Investment returns for mutual funds in 2019 were helped by interest rate cuts. Not only did those provide a lift to fixed-income investments, but they also gave equities investors confidence that, at the time, there was no recession in sight.

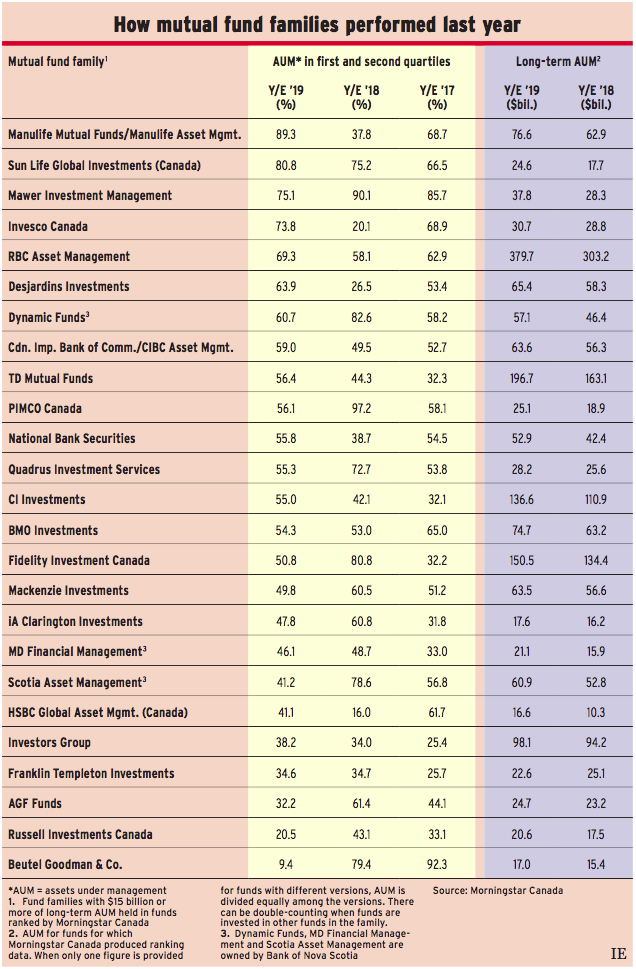

The result was a 30.4% increase in the S&P 500 composite index, despite flat to negative earnings growth. The gains were driven by momentum, says Philip Petursson, chief investment strategist with Manulife Investment Management. That company’s mutual fund family had 89.3% of its long-term assets under management (AUM) held in funds that were ranked in the first or second quartile — i.e., above average — by Morningstar Canada as of Dec. 31, 2019. (All companies are based in Toronto unless otherwise noted.)

Petursson explains that the momentum was partly a recovery from the 20% plunge in stock prices in late 2018, but also from the three interest rate cuts made by the U.S. Federal Reserve Board between August and October as well as the U.S./China Phase 1 trade agreement, announced in December and signed in January.

However, as Petursson points out, the enthusiasm for stocks wasn’t broad-based. The gains were concentrated in the huge technology companies, including Microsoft Corp. and the FAANGs — Facebook Inc., Amazon.com Inc., Apple Inc., Netflix Inc. and Alphabet Inc. (Google’s parent). He notes that Apple alone had an 89.6% increase in its stock price.

Last year was a difficult year for market-timers. The momentum was concentrated in the first four and final three months, with ups and downs in between. Sadiq Adatia, chief investment officer (CIO) with Sun Life Global Investments (Canada) Inc., attributes the strong results for his firm’s mutual fund family — 80.9% of long-term AUM in above-average performing funds — mainly to making the right tactical asset-allocation decisions at the right times. “We read the markets well,” he says, “providing downside protection in certain periods and adding risk at other times.”

Adjusting asset allocation isn’t a strategy used by all firms. For example, Beutel Goodman & Co. Ltd.’s portfolio managers use a bottom-up “value” strategy to provide downside protection by investing only in high-quality companies. That strategy can result in relatively weak performance when momentum is driving markets, as was the case in 2019, when the company had only 9.4% of AUM in funds with first-or second-quartile performance.

“Popular growth or momentum stocks do not fit with our process,” says James Black, Beutel’s director of research, “as we are looking for undervalued companies and have a focus on downside protection.”

Calgary-based Mawer Investment Management Ltd. is a case in point. Paul Moroz, CIO and portfolio co-manager of global equity and global small-cap funds, says stock-picking usually doesn’t do as well in “risk on” or momentum years. Yet Mawer’s mutual fund family had 75.1% of AUM in above-average performing funds.

Invesco Canada Ltd.’s portfolio managers also are stock-pickers — and they did well. Invesco’s fund family came in just below Mawer’s, with 74.2% of AUM in funds ranked in the top two quartiles. On the equities side, Invesco’s fund portfolio managers typically look for about five new investments over a year. That strategy gives the portfolio managers lots of time to put together a list of possibilities and fully explore them, says Rob Mikalachki, CIO for the equities team. “We spend a lot of time travelling the world to understand first-hand the markets and companies we invest in.”

RBC Global Asset Management Inc. (RBCGAM) rounded out the top five. (See table, below.)

Other firms that continued to struggle include Winnipeg-based Investors Group Inc. (38.2%) and Franklin Templeton Investments Corp. (34.6%).

Click image for full size.

Here’s a look in more detail at the strong performers and relative underperformers last year:

MANULIFE INVESTMENT MANAGEMENT. Speaking in early February, Petursson predicted equities markets would be more lacklustre this year, with below-average returns. He notes that U.S. stocks are fully valued and earnings expectations are modest — adding that those modest expectations may be a little high. He also says the market euphoria following the U.S./China Phase 1 trade deal isn’t justified, as the deal doesn’t resolve the underlying issues.

That said, Petursson believes his firm’s approach will continue to deliver good returns because of the quality of the funds’ portfolio managers: “We don’t have one investment philosophy, but are rather a conglomerate of boutique investment teams, each empowered to make its own bottom-up stock selections.”

SUN LIFE GLOBAL INVESTMENTS (CANADA) INC. Adatia attributes 70% of 2019’s equities returns to U.S. interest rate cuts, 20% to more optimism about global trade and just 10% to earnings. Looking ahead, he notes that there are opportunities in emerging markets due to supply-chain changes that came about as a result of the U.S./ China trade war. U.S. companies unable to buy from China have increased purchases of agricultural goods from Brazil and technology inputs from Thailand and Vietnam. He thinks there also could be changes relating to auto manufacturing supply chains.

MAWER INVESTMENT MANAGEMENT LTD. Mawer’s successful picks include a couple of U.K. firms — Aon PLC and Diploma PLC — and New York-based S&P Global Inc.

“In an increasingly risky world, there are more things that have to be insured, including guarding against cyberattacks and environmental liabilities,” says Moroz. Aon is benefiting: its stock price rose by 45.1% last year.

Diploma is a holding company involved in distributing and servicing specialized technical niche products to companies in Europe, North America and Australia. Moroz says Diploma is “really well run, with a high return on capital.” The stock price rose by 64.7% in 2019.

S&P Global, along with Moody’s Investors Service, has a stranglehold on bond rating in the U.S. S&P also provides data, analytics and a large numbers of equities indices. Its stock price rose by 61.3% in 2019.

INVESCO CANADA LTD. Mikalachki says one of the investment team’s most successful stock picks in 2019 was Brookfield Asset Management Inc. The company had an exceptional year, with AUM increasing by 42% and the stock price shooting up by 52.4%. Another winner was Germany-based Scout24 AG, the dominant operator of online automotive and real estate marketplaces in Germany and certain other European countries. Scout24’s stock price rose by 42% in 2019.

Invesco’s stock-picking is complemented by a similar approach on the fixed-income side. The fixed-income team in Canada uses information gathered from the global network of the firm’s Atlanta-based parent to look for high-quality bonds worldwide, explains Avi Hooper, senior portfolio manager, global investment-grade team, fixed-income. Most holdings are investment-grade corporate bonds, but there are some emerging-market sovereigns denominated in U.S. dollars or euros, such as BBB-rated Kazakhstan’s and AA-rated Qatar’s government bonds.

RBC GLOBAL ASSET MANAGEMENT INC. “All in all, 2019 was a great year for balanced funds because almost all asset classes delivered solid gains,” says Dan Chornous, CIO of RBCGAM. He is cautious about 2020, though. Interest rates are unlikely to go lower and earnings expectations are moderate. “Given the aging business cycle and a variety of durable macro risks,” he adds, “we are reluctant to take on significant risk in our portfolios.”

INVESTORS GROUP INC. This fund family has struggled over the past three years, but John Kilfoyle, senior vice president, IG Investments, attributes this mainly to higher-than-average fees. The company is aggressively addressing the issue by moving AUM into low-fee “U” (a.k.a. unbundled) funds. Because the firm has a captive sales force, this transition can be made quickly. Kilfoyle expects 80% of AUM to be held in “U” funds by the end of this year. He says this will significantly increase the fund family’s performance figures.

FRANKLIN TEMPLETON INVESTMENTS CORP. Duane Green, Franklin Templeton Canada’s president and CEO, notes that although the fund family’s performance remains below average, it has been improving — to 34.6% of AUM in the first or second quartiles in 2019 from 34% in 2018 and 25.7% in 2017. Green attributes that improvement to the company’s efforts to diversify by introducing new funds with different strategies.

Although the newer funds are small, many are performing well and Green expects them to push up the overall performance numbers as they attract more assets.

BEUTEL GOODMAN & CO. LTD. Although the company had a relatively weak year in 2019, its longer-term record is stellar, with an average of 75.7% of long-term AUM in above-average performing funds in 2014-18 vs only 9.4% last year.

Beutel’s portfolio managers are long-term investors who don’t worry about short-term swings, says Black: “We look for stable, growing businesses with strong balance sheets [and] trading at discounts to their intrinsic value. If the market goes up, we monitor that everything we own remains well priced, and harvest gains where our process demands.”

Black adds that his firm’s process targets the most appealingly priced businesses, keeping long-term return expectations attractive. “If the market goes down,” he says, “we will seek to take advantage by buying more of the businesses we own and have high conviction in, or [by] taking new positions that were previously too expensive.”