Finding ways to automate basic processes and tasks has become a core business need for advisors, and most firms are responding.

In Investment Executive’s (IE) 2025 Brokerage Report Card, most advisors acknowledged their firms’ efforts to introduce new systems and technologies — this applied to everything from client onboarding tweaks to more basic advisor calendar and notetaking widgets.

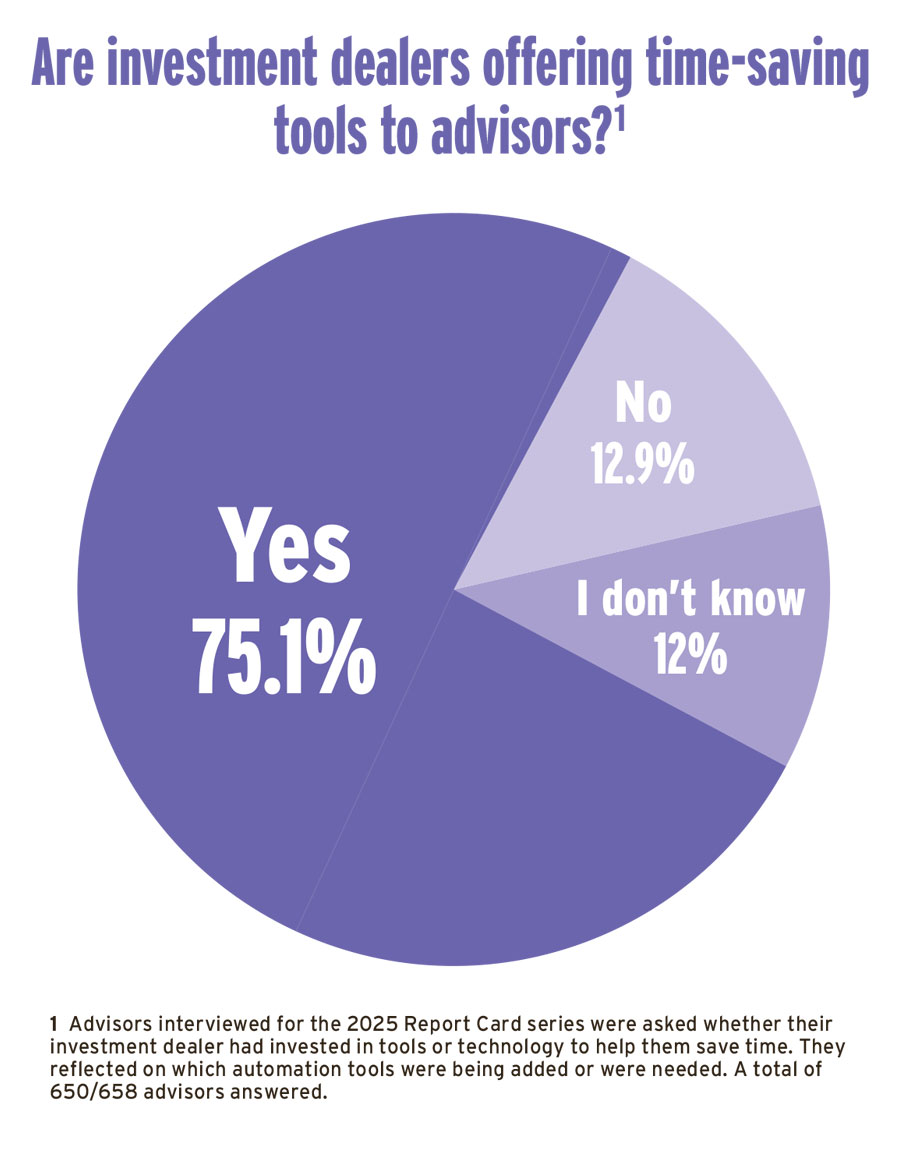

When asked whether their firms had invested in the past year in time-saving tools and technology to help with everyday tasks, three-quarters of advisors (75.1%) said their firms had introduced efficiencies. The remaining 24.9% was split nearly evenly between “no” or “I don’t know” (see pie chart).

There were advisors with each of the 14 firms assessed in the Report Card who gave a yes response, meaning all were engaged in improving advisors’ workflows to some degree. For nine firms, the percentage of advisors who indicated improvement was 78% or above, exceeding the overall average Report Card response.

Two examples were Richardson Wealth Ltd. and National Bank Financial Inc., both of which had 90% of their advisors saying they were providing automation tools. That was the highest result recorded across the 14 firms — though it mainly reflected the confidence those advisors had in understanding and using the tools provided by their firms rather than suggesting the firms were outpacing their industry peers.

“They are constantly setting up more tools,” said a Richardson Wealth advisor in Ontario, who appreciated efforts by their firm to understand advisors’ needs.

It’s easier to open client accounts and fill in know-your-client forms quickly, according to many Richardson Wealth advisors, so they can more efficiently meet compliance requirements. Other enhancements have helped advisors create client reports and better navigate complex discretionary and insurance business systems. More than one advisor with Richardson Wealth cited a business analysis tool for their practice.

Figuring out where to automate is part of Richardson Wealth’s “big tech spend,” said Dave Kelly, president and CEO of the firm, which leans in part on Microsoft functionalities. He referenced Microsoft Power BI, which helps process client data and create reports much faster than in the past. The goal is to bring policy, process and platform together, Kelly said, and he’s asking advisors where they’re trying to do things on their own versus automate.

Advisors with National Bank Financial, who also mentioned Microsoft-based AI software, felt that processing paperwork has been easier. They referred to Microsoft Copilot, for example, which helps with notetaking and summarizing client information.

On top of that, these National Bank advisors highlighted a slew of new capabilities and changes, including streamlined onboarding, updates for their Salesforce Inc. system and improved wealth planning tools. As one of the bank-owned brokerage’s respondents in Ontario said, “They are adding AI into our system,” at the same time as updating the CRM based on advisor feedback and “working to fill all gaps” in the back office.

The firm confirmed in an emailed statement that a new CRM build is coming and that automated account opening plus AI tools for administrative work were launched for advisors, “to give them back their time.”

Curbing advisor confusion

There were cases where advisors and their assistants seemed less satisfied with the efficiency of their firm’s automation-focused updates. If they felt new tools weren’t implemented seamlessly, or that digital training wasn’t offered, their confidence was lower. Also, advisors wanted to understand what was coming, requiring proactive communication about future launches.

Consider the response of advisors with BMO Nesbitt Burns Ltd., where less than half of the advisors polled (41.2%) felt their bank-owned brokerage had actively invested in time-saving tools. Some of these advisors felt their firm was investing but hadn’t yet hit the mark. Just over one-third (35.3%) said they weren’t sure if Nesbitt Burns was providing tools. Nearly one-quarter (23.5%) said they hadn’t been saving any time.

“They could automate all these compliances [tasks] that come through where you give the same responses all the time,” said an advisor in Ontario with Nesbitt Burns. They added, “Even with our email they could start letting us use more AI.”

Another advisor with Nesbitt Burns in Atlantic Canada said investments in automation were a focus for the firm, yet they personally hadn’t seen any effect on their efficiency in the past year.

That’s not surprising to Craig Meeds, head of wealth advice in Canada with BMO Private Wealth, who referenced that business’s decision in autumn 2023 to partner with and transition to global wealth management platform FNZ, starting in 2026. “[It’s] a multi-year journey that we’re on to get from [the] current state to future state with FNZ,” he said. [Advisors] won’t appreciate what that journey means until probably a year and a half or two years from now.”

Meeds said upcoming tools will increase clients’ access to information and allow advisors to get summaries of complex reports, for example.

For Odlum Brown Ltd., more than half of its advisors (51.7%) said the firm had introduced time-saving tools in the past year. Still, the remaining 48.3% gave mixed responses of “no” and “I don’t know,” highlighting some concerns.

For Odlum Brown advisors confident in their firm’s automation efforts, references were made to items like e-signature technology and a new database-linked reporting tool called Buster.

That internal reporting tool helps advisors create dozens of new types of reports, giving them “a ton of information about their clients,” said Trevor Short, president of Odlum Brown. “There’s been huge improvements in terms of efficiency.”

For the advisors who were unsure of that firm’s efforts, many said improvements were still in process for their client relationship tools and client portals. They cited data entry repetition and connection glitches, and asked for more training: “We have Salesforce, [but] we don’t have enough time to adequately learn everything,” said one Odlum Brown advisor.

Warren Beach, chief strategy and business development officer at Odlum Brown, acknowledged the need for ongoing advisor education about technology. He said, “Sometimes there’s a lack of clarity over what’s available and so, this year, we’ve put enhanced focus [on] giving our [advisors] opportunities to learn.”

This article appears in the June issue of Investment Executive. Subscribe to the print edition, read the digital edition or read the articles online.