In 1996, the Canadian Life and Health Insurance Association (CLHIA) published Guideline G6 on illustrations. Board-approved. Distributed to every member company. Incorporated into ongoing compliance programs. Its purpose: “to set out standards for the preparation and distribution of life insurance illustrations, both at point-of-sale and for in-force policies.”

Guideline G6 is still there. Go to the CLHIA website today and you will find it listed as number six on the guidelines page, alongside 17 other standards. Last amended April 2009. A living standard, unchanged for 17 years, while the Canadian life insurance product landscape transformed significantly around it.

The principles in G6 are exactly right. Guaranteed values must be displayed. Non-guaranteed values must be clearly identified as such. Illustrations must not imply in any manner that non-guaranteed values are guaranteed. Where non-guaranteed amounts are included, at least two scenarios must be shown — a primary scenario and one less favourable. Terminology must be consumer friendly. The purpose of an illustration is to inform, not to sell.

Stephen Covey, author of The 7 Habits of Highly Effective People, wrote that, “The main thing is to keep the main thing the main thing.” The main thing in Guideline G6 was always consumer information — clear, honest, complete disclosure of what a life insurance product does, what it costs, what is guaranteed and what is not. That main thing got buried. Not because G6 was wrong. Because the system built around it was designed for something else.

What G6 got right, and what it left open

G6 identified the consumer information problem with precision. It called for clear disclosure of guaranteed versus non-guaranteed values. It required at least two scenarios for any illustration containing non-guaranteed elements. It named the experience factors that should be accounted for — investment rates, mortality rates, lapses, expenses, taxation rates. It insisted on consumer-friendly terminology. These remain the right principles today.

What G6 was not designed to address was the prior question: which product, and why this one rather than the alternatives? The illustration standard assumes the selection decision has already been made. It governs how to present the chosen product. It says nothing about how to document the allocation decision that preceded the recommendation.

G6 also acknowledged, directly, that comparison between products is inevitable and that meaningful comparison enhances rather than conflicts with the need for clear illustration.

The Society of Actuaries had recommended that illustrations never be used to compare one policy with another. G6 explicitly pushed back, since any such comparison is most meaningful if the consumer fully understands the key features and operation of the policies being compared. This potential use enhances rather than conflicts with the need for the illustration to be informative.

The comparison principle was in the guideline from the beginning. What nobody built was the framework to make that comparison systematic, consistent and consumer accessible.

The standard the investment industry built

Every investment advisor in Canada is trained to show the asset class landscape before recommending products. Cash, bonds, equities — here is what each does, here is what it costs, here is how they work together, here is a model portfolio at your age and risk profile. Then specific products are recommended for each component. This is not a recent regulatory invention. It is a professional standard the investment industry internalized decades ago and has never abandoned.

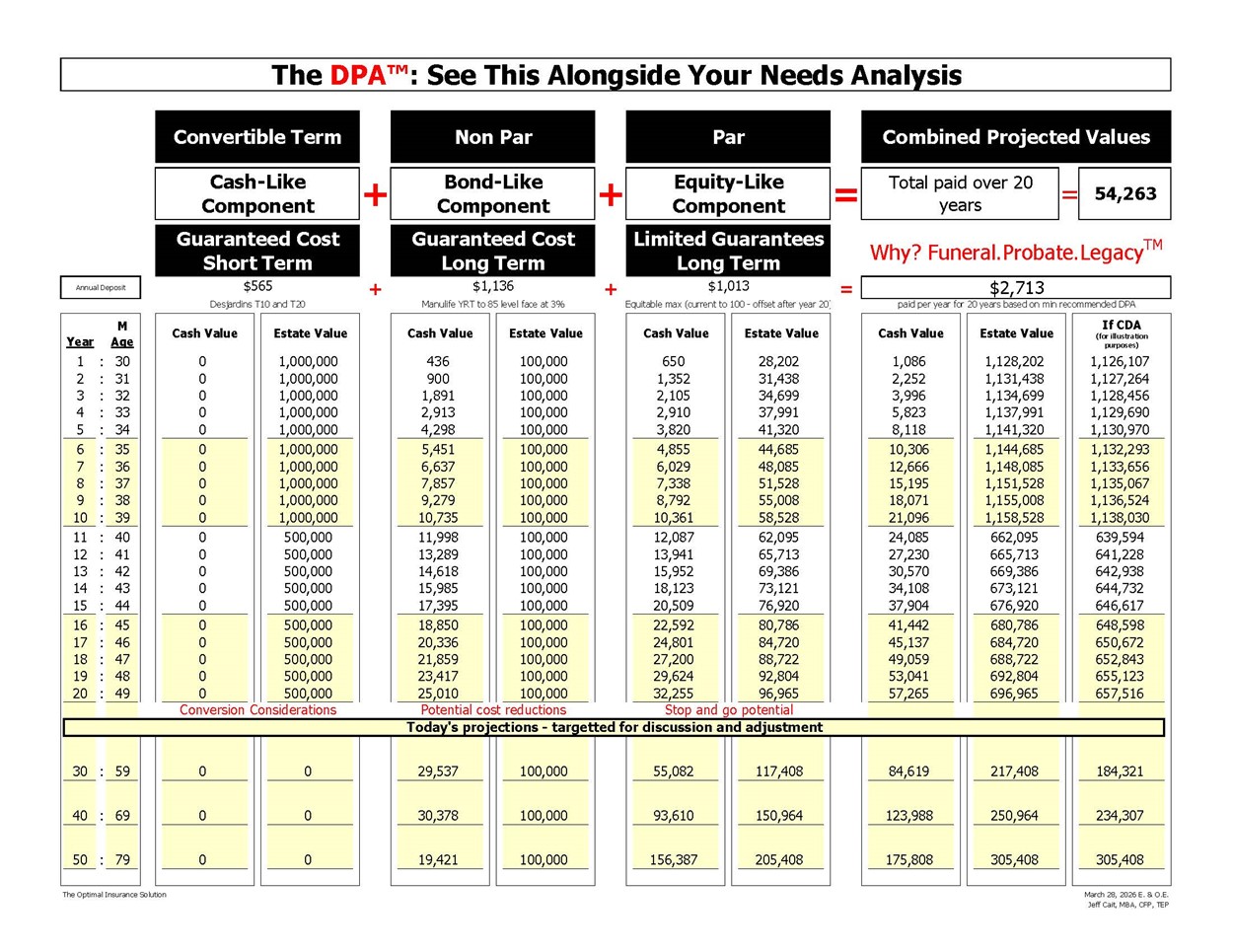

The life insurance industry never applied identical logic to its own asset class. The three permanent products available to Canadian consumers — convertible term, non-participating whole life and participating whole life — have meaningfully different characteristics, costs, guarantees and purposes.

Term is cash-like: temporary, maximum coverage for minimum premium, guaranteed cost for the short term. Non-par is bond-like: guaranteed mortality costs, predictable, designed for long-term certainty. Par is equity-like: limited guarantees on the cost side, long-term growth potential through smoothed dividend crediting. These products are not interchangeable. They are complementary. They belong in a portfolio view.

The investment industry standardized the portfolio view decades ago. The life insurance industry never did. That is a design gap, not a character gap. The advisors operating within the existing system are not behaving badly. They are working within a structure that was built around single-product economics: one-and-done compensation, single-carrier administrative efficiency and illustration software designed for individual product presentation.

The system was not built to make a diversified portfolio recommendation economically viable. It was built to move product.

G6 pointed toward the comparison principle in 1996. The economic structure of the industry pointed away from it. The main thing got lost.

The diversified portfolio approach

The diversified portfolio approach (DPA) provides illustration guidelines for independent Canadian life insurance professionals. That is the precise description of what it is and what it does.

It applies G6’s principles — guaranteed versus projected, scenarios, consumer-friendly disclosure — to all three life insurance asset classes simultaneously, at the same premium outlay, for the same insured. It shows the consumer what term does, what non-par does, what par does, how they work together and what the combined portfolio looks like at their age and life stage. Then the consumer decides how much to allocate to each component, or whether to allocate at all.

The guaranteed-versus-projected distinction that G6 requires is built into the DPA framework from the ground up. The mortality costs in convertible term and non-participating whole life are contractually guaranteed and printed in the policy — they cannot be changed by an insurer’s unilateral action, which is G6’s own definition of guaranteed.

The dividend scale in participating whole life is not guaranteed and is presented in a range: current scale and a less favourable scenario. Assumptions are visible. Variables are named. The consumer sees what is certain and what is not, before they sign anything.

The DPA also delivers G6’s comparison principle in practice. The consumer sees all three products side by side. They see the allocation decision explicitly. They see what term costs versus what non-par costs versus what par costs, and what each one provides in return. That is the comparison G6 endorsed in 1996 and that almost no consumer has ever actually seen presented that way.

The DPA is not company specific. It is a framework any independent advisor can apply using the best available products in each category for their client’s age, health, coverage needs and premium capacity. The illustration guidelines are the structure. The product selection happens within the structure.

In practice, adopting the DPA as an illustration standard means three things.

First: document why this allocation was chosen over the alternatives — not in the compliance forms, but in plain language the consumer can read and question. If the recommendation is term-only at this stage, say why permanent coverage was considered and deferred. If the recommendation includes all three components, say what role each plays and why the allocation is what it is.

Second: show the consumer where to find what is guaranteed versus what is projected in the policy contract itself — not just in the illustration at the point of sale. G6 has required this distinction since 1996. The practice standard is to make sure the consumer can find it after they own the policy.

Third: put the recommendation, the math and the rationale in writing — in a form the consumer can read, question, keep and share with their accountant, their financial planner, their lawyer and their children.

G6 governs the point-of-sale illustration. It does not govern what happens to the consumer’s understanding of their policy after they own it. The guideline acknowledges this directly: in the case of an in-force policy, the policyholder’s retention and understanding of information given at time of sale may have deteriorated since issue.

The life insurance holding statement addresses that gap. It is a plain-language summary of the policies in force: the ownership structure, the coverage amounts by product type, the cash values, the guaranteed costs, the projected values and what each component is intended to accomplish in the overall wealth plan.

It is not a compliance form. It is not a carrier illustration. It is a portfolio summary the consumer can share with anyone whose job it is to help them — in a form they can read, question and keep.

Christine Van Cauwenberghe’s Wealth Planning Strategies for Canadians — required reading in the chartered life underwriter curriculum and the foundational text for comprehensive financial planning in Canada — identifies insurance planning as one of the six components of a complete wealth plan.

She writes that due to its complexities and potential long-term benefits, it often warrants specific attention. The DPA is what specific attention looks like in practice. The holding statement is what it looks like in writing.

Why now

Guideline G6 has been on the CLHIA website since 1996. Last amended in 2009. The industry has had a living illustration standard for nearly 30 years. The principles have not changed because they did not need to change — they were right from the beginning. What has changed is the availability of tools to implement them properly.

The administrative complexity that made a diversified portfolio recommendation difficult for a single advisor working across multiple carriers is solvable in ways it was not solvable in 1996 or 2009. The illustration framework exists. The documentation standard exists. The consumer education language exists.

What is needed is the professional will to adopt the DPA as a practice standard rather than leaving it as a good idea.

The main thing in G6 was always consumer information. Clear, honest, complete disclosure of what a life insurance product does, what it costs, what is guaranteed and what is not. That main thing is available to every independent Canadian life insurance professional today, in a form they can apply to every client conversation, at every life stage. It does not require a regulatory change. It does not require a carrier initiative. It requires an advisor who has decided that the consumer sitting across from them deserves to see the full picture.

The main thing is to keep the main thing the main thing. The DPA is the illustration standard that makes that possible. The decision to use it is available right now.

Jeff Cait, MBA (Finance), CFP, TEP is an independent life insurance consultant and founder of the Trusted Advisors Network. He has more than 40 years in the industry.