Although the new client relationship model reporting and disclosure rules requiring wealth-management firms to share new information about fees and portfolio performance (CRM2) have now been in full effect for more than a year, 79% of investors in Canada are still unaware of the initiative. Furthermore, according to the J.D. Power 2018 Canadian Full Service Investor Satisfaction Study released Thursday, even among those relatively few investors who are aware of CRM2, only 49% have actually noticed the associated changes in the reporting.

“The low awareness and understanding of CRM2 poses an ongoing challenge and opportunity for firms and financial advisors,” says Mike Foy, senior director of the wealth management practice at Costa Mesa, Calif.-based J.D. Power, in a statement.

“While the industry’s concern that the new fee and performance reporting would trigger an exodus of investors hasn’t materialized, the risk of defections still exists. The study suggests that the best way to address that risk is for advisors to be proactively and regularly discussing fees and performance with their clients, rather than leaving them to figure it out on their own,” he adds.

The study shows that investors who are aware of CRM2 and have noticed the changes in the reporting format, as well as had their advisor explain the fees within the past 12 months, are not only much more likely than investors overall to understand their fees (55% vs. 32%, respectively, indicate “complete understanding”), but they are also much more loyal to their firm (58% “definitely will” remain with their firm for the next 1-2 years vs 46%) and are more likely to recommend their firm (53% vs 37%).

“Advisors continue to be critical of CRM2 achieving goals of greater investor understanding of fees and performance,” Foy says, adding, “and the greater risk for both advisors and firms remains with inaction rather than taking action to engage with clients.”

J.D. Power highlights three key findings findings of the 2018 study.

- The role of the financial advisor as well as client expectations are changing, depending in part on the investor’s age. According to the study a greater portion of Baby boomers (15%) cede all decisions to their financial advisor, while only 10% of millennials do the same. Meanwhile, 39% of millennials consider consider their advisor more of a sounding board for their own ideas, vs just 24% of boomers.

- More than three-fourths (77%) of investors have not used or have only tried using their wealth management mobile app once. This is a very low adoption and usage rate, compared with other channels as well as other industries, J.D. Power says. Those who have used the mobile channel rate their experience significantly lower (satisfaction of 716, on a 1,000-point scale) vs other channels such as phone (808) and online/web (792), suggesting that firms have significant work to do to improve the mobile user experience as well as driving engagement.

- While awareness of robo-advisors is comparable among boomers (43%); Gen X (45%); and millennials (48%), it is the latter who are much more likely to adopt the technology, according to the study. Nearly one-fourth (22%) of millennials have used a robo-advice service, compared with only 9% of Gen X investors and 3% of boomers. More than half (52%) of millennials using robo-advisors attributed their usage to a desire for lower fees.

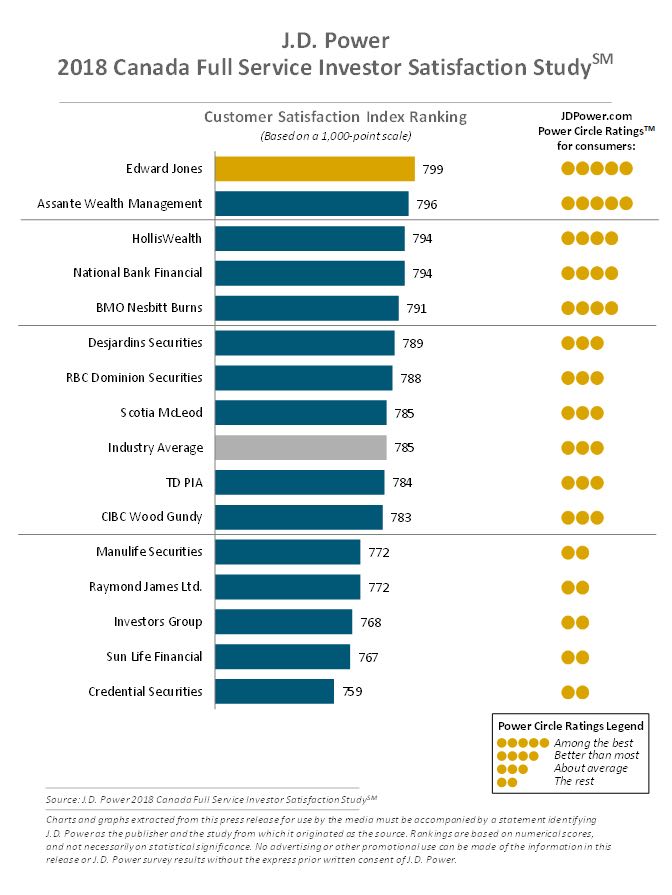

Edward Jones ranks highest in overall satisfaction for a sixth consecutive year, with a score of 799. Assante Wealth Management (796) ranks second, while HollisWealth and National Bank Financial rank third in a tie (794 each). In 2018, overall satisfaction is 785, up from 771 in 2017.

The study measures overall investor satisfaction with full-service investment firms and financial institutions that offer wealth management and private banking services. It was fielded in May-June 2018 and is based on responses from more than 4,400 investors who work with a financial advisor on their primary investment account.