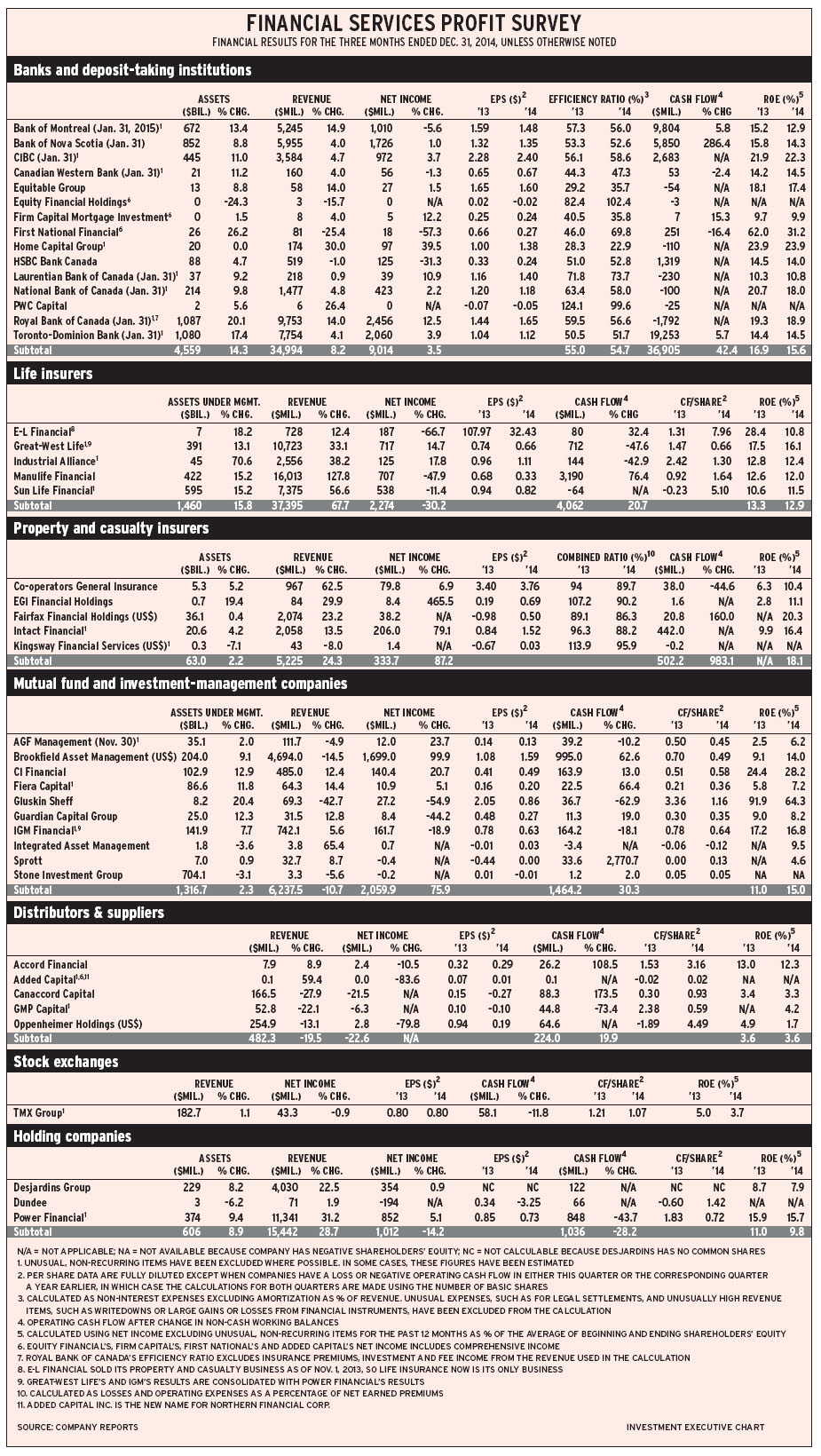

Canada’s economy grew strongly in 2017 and, unsurprisingly, most of Canada’s publicly traded financial services companies had higher earnings in the third quarter (Q3) of calendar 2017 compared with the corresponding quarter a year earlier.

Of the 43 companies in Investment Executive’s (IE) quarterly profit survey, 25 saw an increase in earnings, while Echelon Financial Holdings Inc., Integrated Asset Management Corp. (IAM), Oppenheimer Holdings Inc. and Dundee Corp. reported positive net income vs a loss the year before.

However, the drops in net income at 10 firms and the losses at four others were enough to almost offset those gains. (These figures exclude Great-West Lifeco Inc. [GWL] and IGM Financial Inc., as the results of both are consolidated with those of parent firm Power Financial Corp.)

In fact, the average gain in net income for the sector overall was only 0.1%. A major reason was a 50.9% earnings drop at Brookfield Asset Management Inc., which translated into a drop of almost $1 billion in net income in dollar terms vs Q3 2016 because Brookfield is a very large company.

In fact, Brookfield’s drop is larger than the banks’ combined year-over-year gain of $862 million in net income; 10 of the 12 deposit-taking institutions saw their earnings rise from a year earlier.

Brookfield has been picking up assets during the past few years and that has almost doubled revenue in Q3 2017 vs Q3 2016. However, with that kind of expansion, costs tend to rise more than revenue initially – as happened in this case.

Canada’s economy is expected to slow to around 2.2% in 2018 from 3% in 2017. (See story on page 1.) That’s not alarming as it’s still well above Canada’s current potential growth of around 1.5%. Recent growth rates have been unsustainably high, driven by strong housing markets and buoyant consumer spending.

Economists anticipate housing and retail sales will return to more normal levels this year.

However, the current economic situation should allow financial services companies to continue to grow their earnings, albeit at a modest pace.

Thus, seven firms were sufficiently optimistic to raise their quarterly dividends: Bank of Montreal (BMO), to 93¢ from 90¢.; Equitable Group Inc., to 25¢ from 24¢; Laurentian Bank of Canada, to 63¢ from 62¢; National Bank of Canada, to 60¢ from 58¢; MCAN Mortgage Corp., to 37¢ from 32¢; Industrial Alliance and Financial Services Inc. (IA), to 38¢ from 35¢; and Sun Life Financial Inc., to 45.5¢ from 43.5¢. In addition, First National Financial Corp. announced a special divided of $1.25.

Several firms announced or completed transactions in this quarter, including:

– Bank of Nova Scotia announced plans to buy a majority interest in BBVA Chile, one of Spain-based Banco Bilbao Vizcaya Argentaria SA’s subsidiaries.

– Home Capital Group Inc. is selling its payment-processing and prepaid cards business.

– ECN Capital Corp. has sold or is selling several non-core businesses while acquiring higher-growth and less capital-intensive firms.

– IA completed the acquisition of HollisWealth Inc. from Scotiabank on Aug. 4.

– Sprott Inc. sold its diversified funds business on Aug. 1. Then, in early October, the firm announced the purchase of Central Fund of Canada Ltd. and the formation of a joint venture with Ceres Partners LLC to make investments to acquire and actively lease farmland in North America.

A closer look, by industry:

– Banks. Only BMO and Home Capital had lower earnings year-over-year.

BMO’s decline is not worrisome, as it was a result of increased reinsurance claims arising from an unusually destructive hurricane season.

Home Capital is another matter. Costs have risen following the company’s discovery of income-verification issues for mortgages brought in by some of the brokers in its network. Both customer and investor confidence has been affected. The company’s Q3 2017 financial report states that the firm’s “priorities are to grow residential and commercial lines to take back market share.”

In a similar development, issues emerged in early December concerning the quality of control functions and underwriting procedures for mortgages at Laurentian Bank that were sold to other institutions. The bank is buying back those mortgages and shoring up its processes, but customer and investor confidence has been affected negatively.

A key indicator for banks is loan-loss provisions. For the 12 deposit-taking institutions, total loan-loss provisions have remained at around $1.9 billion through the past year, down from a peak of $2.8 billion in late 2015 and early 2016, but still above the average of $1.6 billion during the previous three years.

– Finance Companies. Five of the seven firms had higher earnings. The loss at Callidus Capital Corp. was mainly because of lower interest revenue. Element Fleet Management Corp.’s net income was down by 30.8%, but it’s still in transition after the former Element Financial Corp. was divided into two companies: Element Fleet and ECN.

– Life Insurers. Results were mixed in this industry. IA’s and Manulife Financial Corp.’s earnings increased, while net income dropped at E-L Financial Corp., GWL and Sun Life.

All the companies reported significantly lower revenue because of losses on the fair value of their assets. Life insurers have large amounts of assets to back up their insurance liabilities, so big swings in revenue are frequent.

– Property & Casualty Insurers. Fairfax Financial Holdings Ltd., Intact Financial Corp. and Genworth MI Canada Inc. had increased earnings, and Echelon Financial Holdings Inc. reported positive net income vs a loss in Q3 2016.

That leaves Co-operators General Insurance Co., which had a loss vs positive earnings in Q3 2016. This firm’s results were dragged down by much lower investment income year-over-year.

Fairfax had a big underwriting loss because of losses from hurricanes, but that was more than offset by gains on investments. This is not unusual for this company, as its major focus is on investing its assets, including using sophisticated techniques such as derivatives.

Case in point: Fairfax’s gains on investments totalled US$1.1 billion in Q3 2017, up notably from a loss of US$200 million in Q3 2016.

– Mutual Fund and Investment-management Companies. Results were mixed in this industry. AGF Management Ltd., CI Financial Corp. and Guardian Capital Group Ltd. had increased earnings, while IAM reported positive income vs a loss in Q3 2016.

On the other hand, Brookfield, Fiera Capital Corp., Gluskin Sheff & Associates Inc. and IGM had lower net income.

Sprott, which is in transition after selling its diversified funds business, had a loss vs positive net income in Q3 2016.

Among the Big Three mutual fund companies, CI and IGM experienced net sales, while AGF suffered small net redemptions.

– Brokerages. Canaccord Genuity Group Inc. and GMP Capital Inc. had losses vs positive net income in Q3 2016, while Oppenheimer Holdings Inc. had positive net income vs a loss in Q3 2016.

All three companies have international clients or divisions, but Canaccord and GMP are much more exposed to Canada and, thus, the resources sector. Oppenheimer’s base is in the U.S.

– Exchanges. TMX Group Ltd. had a small 1.1% increase in net income.

– Holding Companies. Desjardins Group had a solid 10.2% increase in earnings, while Power Financial’s lower results reflected those at GWL and IGM.

Dundee is mainly an investment company that focuses on resources, although it also operates Goodman & Co. Investment Counsel Inc. and Dundee Securities Ltd., both of which had pretax losses year-over-year.

© 2018 Investment Executive. All rights reserved.