With seniors becoming Canada’s fastest-growing demographic, the unique issues affecting these clients are becoming ever more important for regulators. As a result, brokerages and their investment advisors will be facing increased scrutiny and greater compliance challenges when dealing with senior clients in the years ahead.

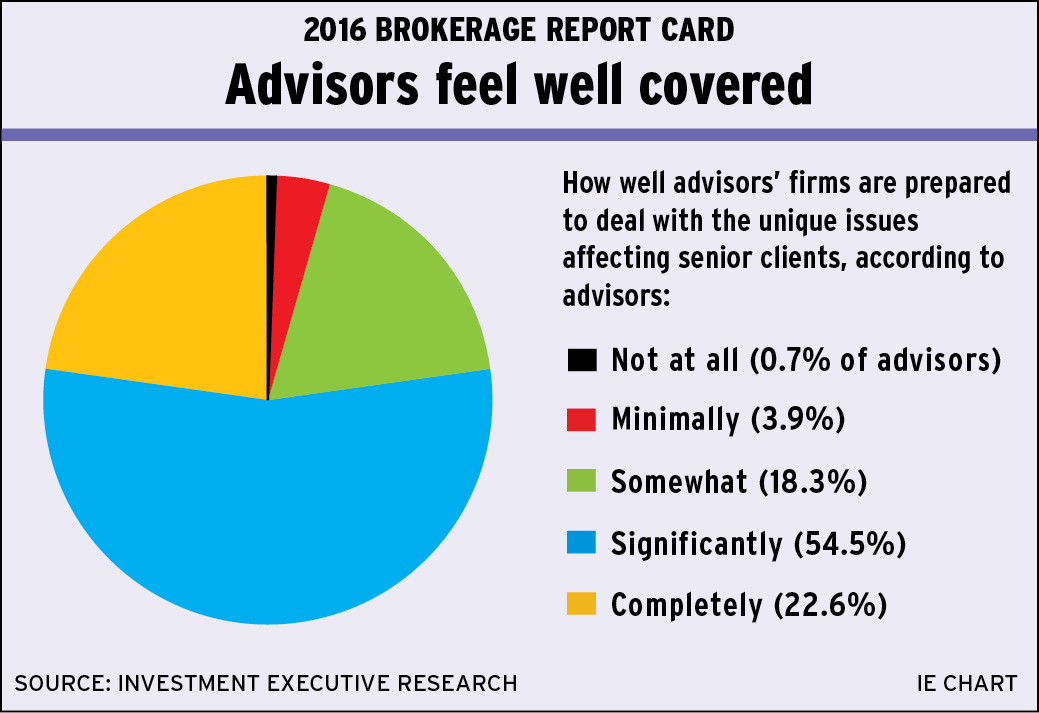

In a supplementary question added to this year’s Brokerage Report Card, Investment Executive asked advisors how well their firms are prepared to deal with unique issues affecting this demographic. These issues include recognizing cognitive decline and having sufficient retirement savings. The responses reveal that 77.1% of advisors believe their firms are very well prepared to deal with the increased regulatory burden related to these particular clients.

“We’re totally prepared for that,” says an advisor in Ontario with Mississauga, Ont.-based Edward Jones. “All our programs are designed for retirement and longevity and showing [clients] how their money will last.”

An advisor in Ontario with Toronto-based Richardson GMP Ltd. points out that many high net-worth clients are more likely to be seniors, so brokerages are prepared for increased regulation: “Wealthy individuals are typically part of the aging population. So, our firm is very well prepared in that regard and promotes discussions among family members and individual clients.”

An advisor in Alberta with Calgary-based Leede Jones Gable Inc. says the firm’s advisors work closely with compliance with regard to senior clients: “[The compliance department] is on the ball. [They] monitor asset allocation to make sure it checks out with what’s written down. [That process] is over and above what we do with our clients. It serves as a backup. It’s a reassuring safety net.”

Despite the fact most advisors felt their firms are very well prepared to deal with seniors’ issues, advisors with Toronto-based Raymond James Ltd. and Vancouver-based Odlum Brown Ltd. were quick to point out that their firms go above and beyond in dealing with issues unique to senior clients.

Specifically, Raymond James’ advisors noted that their firm launched a retirement planning initiative in 2014 based upon the longevity research developed at the Massachusetts Institute of Technology’s AgeLab as a way to improve the services the brokerage’s advisors offer to senior clients.

“That has shifted the conversation we have with senior clients. Now, we recommend to them to use their years rather than just survive them,” says a Raymond James advisor on the Prairies. “We have access to a lot of that research. On the longevity side of it, [the firm’s services] have been top-notch.”

The planning aspect is only one way that Raymond James deals with seniors-related issues. The firm also has a unique risk-tolerance questionnaire that allows advisors to determine appropriate levels of risk for these clients, says Sandy Martin, Raymond James’ senior vice president and chief compliance officer in Vancouver.

“The risk tolerance questionnaire is quite strong,” Martin says. “It measures investor psychology and financial capacity. It helps define the risk tolerance that will be stated on the Know Your Client form.”

In addition, Raymond James’ compliance department electronically supervises all trades involving senior clients’ accounts, he adds: “For any senior with more than 10% [of assets held in high-risk investments], we pull reports and we can have a discussion with the advisor to figure out why the senior is in that position.”

Advisors with Odlum Brown praise their firm’s approach to dealing with the issues relating to senior clients. The firm focuses on education and hands-on experience.

“We are one of the more proactive firms on [seniors’ issues],” says an Odlum Brown advisor in British Columbia. “We’ve had a lot of training in recognizing signs of dementia and parental abuse. We’ve always had an older client base, so this is something we have a lot of experience with.”

Kim Abbott, vice president and director of sales and business development with Odlum Brown, points out that one way the firm educates its advisors on this issue is through the close ties to the community the firm has developed over the years.

“The one thing that is invaluable to us is we have close connections with the local chapter of the Alzheimer’s Society,” she says. “[Chapter members] came in to speak to us on what to look for in [the senior] demographic. We also had a lawyer come in to speak about what things to look for if you have concerns about any client who might [have cognitive issues.]

Even though more than 75% of surveyed advisors felt their firm is very well prepared to deal with seniors’ issues, 4.6% of advisors said their firm is poorly prepared and 18.3% of advisors said their firm is somewhat prepared. Most of the advisors who said their firm is not prepared work at bank-owned dealers and felt their firm is focused on another demographic.

“I don’t think [seniors’ issues] are even on their radar,” says an advisor in Atlantic Canada with Toronto-based ScotiaMcLeod Inc. “They’re just looking at high net-worth clients and aren’t worried about seniors.”

“They don’t seem to be moving in that direction,” adds an advisor in Alberta with Toronto-based RBC Dominion Securities Inc. “They’re looking for assets; they don’t seem to care about the elderly.”

© 2016 Investment Executive. All rights reserved.