The high-calibre performance of Calgary-based Mawer Investment Management Ltd.’s Mawer Global Small Cap Fund has resulted in the selection of its two lead managers — Paul Moroz, Mawer’s chief investment officer, and Christian Deckart, deputy chief investment officer — as joint winners of Investment Executive’s (IE) 2019 Fund Manager of the Year award.

In choosing the winner, IE uses a point-based scoring system to rate Canadian mutual funds that have a minimum record of 10 years. Points are awarded for each year of positive annual returns as well as relative outperformance and quartile rankings. IE also assesses cumulative 10-year returns, management expense ratios and volatility.

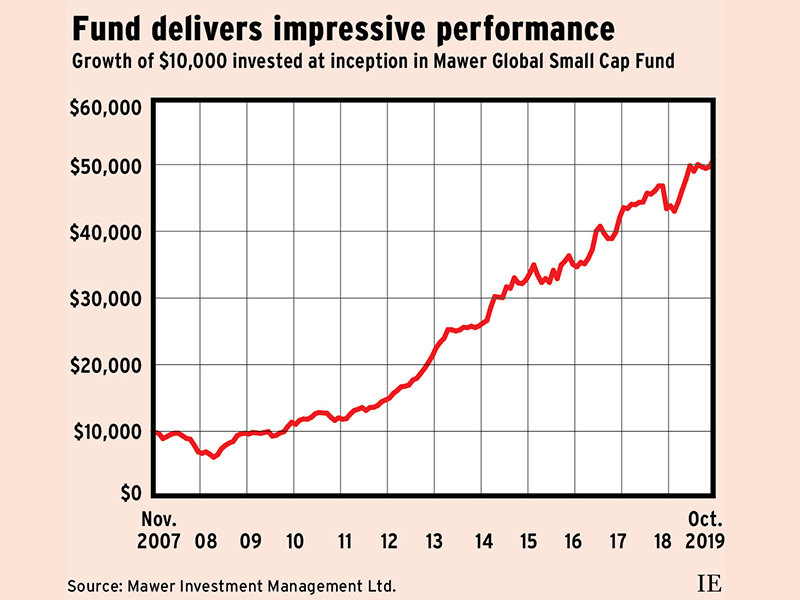

The Mawer fund’s 10-year average annual return as of Oct. 31 was a stellar 16%, far ahead of the 11.3% shown by the benchmark Dow Jones global small cap total return (Canadian dollars) index.

“Our investment philosophy is to seek wealth-creating businesses with strong management teams that are trading at less than their intrinsic value,” Deckart says.

In short, the goal is to buy high-quality companies at a reasonable price. The Mawer team examines cash flow and debt, and seeks a sustainable competitive advantage that will ensure long-term corporate success. The Mawer portfolio managers are not in-and-out traders; their ideal holding period is eight to 10 years, a period they believe is necessary to enjoy the fruits of growing profitability as companies mature.

Ideally, as small companies become larger, not only do their revenue and profits increase, but their stocks trade at higher multiples with greater investor recognition. “We don’t just examine the income statement of a company,” Deckart says. “We look for a healthy return on capital employed. Some companies may be profitable, but if they are not good allocators of capital, they won’t have long-term success.”

The $3-billion Mawer fund, launched in 2007, boasts an impressive average annual compound growth rate since inception of 12.5% as of Oct. 31, according to Toronto-based Fundata Canada Inc. The fund’s annual returns are in the top quartile for eight of the 10 calendar years up to 2018 and year-to-date in 2019.

Shorter-term fund performance also is superior. The Mawer fund posted a five-year average annual gain of 12.6% as of Oct. 31, substantially ahead of the benchmark’s 9.4%. And the fund has a three-year average annual gain of 11.3%, beating the index’s 8.4%.

The Mawer fund’s reasonable management expense ratio of 1.74% contributed to the succulent returns savoured by unitholders.

“Our motto is ‘turn over more stones’ and in the past year we’ve spoken to more than 500 companies,” says Deckart, 42, who was on his way to becoming a lawyer in Germany before he changed direction and entered the investment business in 1997. “The investment business is constantly evolving and changing, and that makes it exciting. Law is something of a fixed universe.”

Click image for full size.

Before Deckart joined Mawer in 2013, he worked as an equities analyst for an investment boutique in Zurich and, before that, as a small- and mid-cap stock analyst with Merrill Lynch Europe Ltd. in London and Commerzbank AG in Frankfurt.

Moroz, 39, joined Mawer in 2004 as an equities analyst and now oversees research in global equities and fixed-income. Prior to joining Mawer, he had jobs at Alberta Investment Management Corp., the investment arm of the Alberta government, and Merrill Lynch Canada Inc. During 2016 and 2017, he served as CEO and director of Mawer Investments Management Singapore Pte. Ltd., exploring Asia and learning about emerging markets from the ground up — whether that included traversing sewage-filled streets in Mumbai slums to investigate local business operations or inspecting huge factories in China.

“You can glean a lot of added information by actually seeing factories and distribution centres,” Moroz says, “as well as meeting management teams face to face and becoming familiar with different cultures.”

The two other team members on the Mawer fund are analysts John Wilson and Karan Phadke. Moroz and Deckart point to Mawer’s “culture of collaboration,” fostered by the independent nature of the employee-owned private investment firm, in which research is catalogued and shared among the 30 other team members on Mawer’s stable of 13 funds.

Both Moroz and Deckart ventured into the investment world at a young age and learned from their early mistakes.

As a teenager, Moroz tried to speculate on currencies by scraping together $1,000 and investing in the Bulgarian lev after its drastic collapse vs the U.S. dollar in 1997. Hoping to profit from a quick rebound of the lev, he raced to banks in Calgary in search of the currency, but came up dry and couldn’t make the trade.

Deckart was inspired at the age of 12 by the book One Up on Wall Street, recommended by his godfather. Deckart was keen to take author Peter Lynch’s advice and buy shares in a company that Deckart knew from his own activities. So, the fledgling investor, inspired by his CD player and his Walkman, eventually saved enough pocket money to buy shares in Japan-based electronics company Sony Corp. in 1989, only to watch his savings melt away when the stock price subsequently dropped.

“Our first ventures weren’t successful,” Deckart says. “But I did learn important lessons about risk management. I realized I knew something about one thing — products — but I didn’t know about management or valuation.”

Neither of the young investors was deterred by failure, and both view mistakes as part of the investment experience. “There are many ways to lose money — and when you get burned, you learn,” says Moroz. “It’s a constant process of learning, and it’s cumulative.”

The Mawer fund invests in small- and mid-cap companies anywhere that have a free-float market capitalization of US$3 billion-US$7 billion at the time of purchase. The fund reduces risk by diversifying among currencies, industry sectors and countries. Currently, its biggest geographical weightings are the U.K. (16%) and Germany (11%), with Sweden and the U.S. next in line. The fund had 69 holdings in 24 countries as of Sept. 30.

“We are truly global,” Moroz says. “We look everywhere, but we don’t necessarily buy everywhere. There are certain pockets where the business cultures and values are more conducive to long-term success.”

Moroz and Deckart also look for what Moroz calls a “compounding runway”: the ability of a company to take advantage of economies of scale in a relatively risk-free manner. Expansion strategies may include introducing successful products or services to new markets — such as a different geographical area — or acquiring complementary businesses.

Moroz says the attributes of the management team are particularly important in small companies, and motivation, talent and ability to allocate capital are key. “We are big believers in the value of corporate culture,” he says. “We realize the importance of a strong team here at Mawer, and that’s what we want to see in the companies we hold in the fund. The team can be a hidden competitive advantage that the stock market doesn’t always capture.”

Moroz’s biggest portfolio successes at Mawer have come from investing in the right people; some of the biggest mistakes involved misjudging people’s motives, intentions or abilities.

“You need to meet the people and recognize patterns of behaviour in how they manage relationships with employees and customers,” Moroz says.