The uncertainty hanging over Richardson Wealth Ltd. in recent years has resulted in stagnant growth and advisor departures, senior leaders at the brokerage admit. But with last fall’s shareholder dispute settled, ownership restructured and a new name on the door, executives say the independent firm formerly known as Richardson GMP Ltd. is setting a clear strategy and is ready to grow.

“This new clarity, this new alignment of [shareholder] interests, is the end of our [advisor] turnover, I would say, and the beginning of a significant growth phase,” said Andrew Marsh, president and CEO of Richardson Wealth in Toronto.

Richardson Wealth is mapping out a strategy to leverage the firm’s scale, capabilities and reputation to recruit top advisors, acquire smaller wealth and asset management firms, and invest in in-house services and products to gain a greater share of the lucrative wealth management market.

“We have this pent-up energy that is going to be unleashed because we’ve been held back for the last year or two,” Marsh said.

Kish Kapoor, president and CEO of Richardson Wealth’s parent firm, Toronto-based RF Capital Group Inc. (formerly GMP Capital Inc.), said there’s a “significant” opportunity to grow the brokerage firm’s business — to even double or triple the business over a period.

The journey to the new Richardson Wealth began in 2017, when the board of GMP Capital decided to focus on growing a strong independent wealth management platform.

To that end, GMP Capital sold off its capital markets business in 2019 and announced it was interested in buying all of Richardson GMP, its subsidiary, from minority and advisor shareholders in exchange for shares of GMP Capital. An initial shareholder proposal in early 2020 was restructured in the summer, after the economic effects of the pandemic hurt Richardson GMP’s valuation. In the fall, a disagreement arose with minority shareholders (including two former CEOs of GMP Capital), which was resolved when GMP Capital returned $40 million to shareholders through a share buyback.

When the dust settled, Richardson Financial Group Ltd. owned 43.8% of GMP Capital, Richardson Wealth advisors owned 30.7% and existing GMP Capital shareholders owned 25.6%. In November, the brokerage changed its name to Richardson Wealth (Patrimoine Richardson in Quebec), while the parent firm changed its name to RF Capital Group.

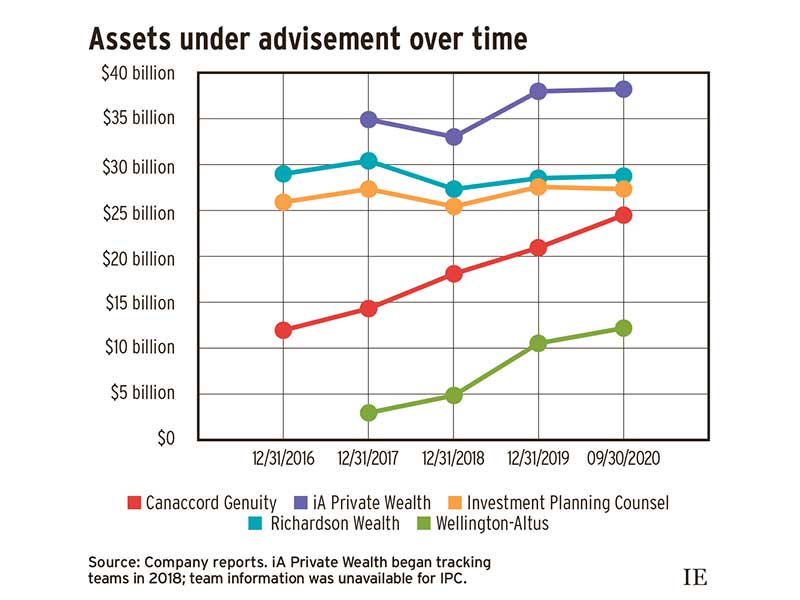

The uncertainty of the past several years is reflected in Richardson Wealth’s growth. As of Dec. 31, 2020, Richardson Wealth reported $30.3 billion in assets, up marginally from $29.3 billion at the end of 2016.

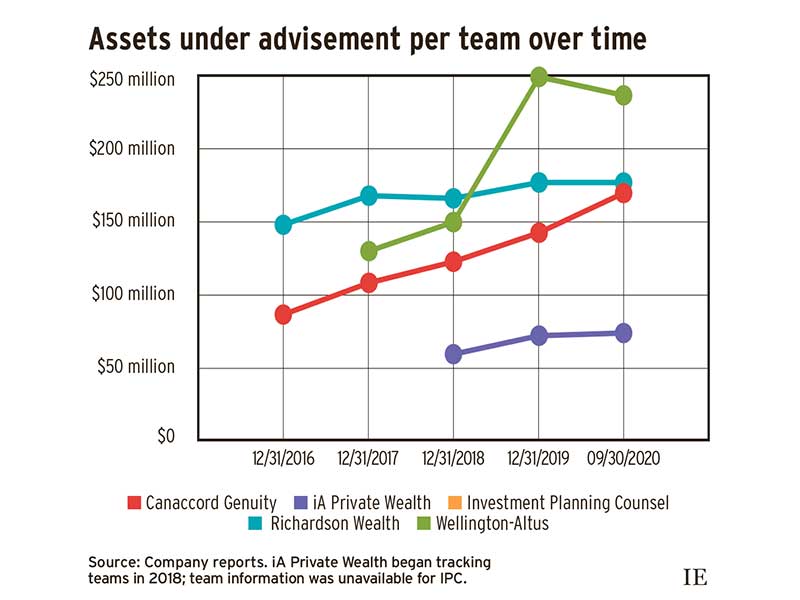

The lack of clear direction also resulted in rival firms luring away advisors from Richardson Wealth. At the end of 2020, Richardson Wealth reported 162 advisory teams, down from 199 four years prior.

Charlie Spiring, co-founder and chairman of independent rival Wellington-Altus Private Wealth Inc. in Winnipeg, said that Richardson Wealth has fallen behind its peers in terms of its investments in products, services and technology, with management distracted by the ownership reorganization and shareholder dispute.

“Because they stalled for five years, they have to restart that engine,” Spiring said, adding that Richardson Wealth has a “talented management” team that is likely “to tighten the gap” in the years ahead.

A stronger Richardson Wealth is good for the Canadian independent wealth management sector, Spiring added.

Marsh said Richardson Wealth plans to enhance what he believes are already “industry-leading” core technology systems.

“While we’ve been waiting for this transaction to happen over the last couple of years, we’ve kind of kept our powder dry on significant investments in our systems,” Marsh said. “We want to make it easier for advisors to work here, and easier for our clients to work with us. I think the resulting investment in our technology platform will make a significant difference in the coming year or two.”

Marsh said the firm will also direct resources to improving discretionary portfolio management systems and tools.

“Over 80% of our revenues are recurring fee-based revenue, driven primarily by the explosive growth we have seen in our [portfolio management] platform,” he said. “We see a great opportunity to leap-frog our competitors in this area.”

Richardson Wealth intends to not only stem the tide of advisor departures but add to its team. In GMP Capital’s third-quarter 2020 report, the firm stated that Richardson Wealth would be proactively recruiting advisors, offering cash incentive bonuses in exchange for long-term commitments to the firm.

Marsh said the brokerage is looking for advisors in “growth mode” who have at least $100 million in assets under administration. Richardson Wealth also will seek veteran advisors who, as part of their business succession planning, “want to make sure that they’re leaving their clients at a firm that will respect [them],” he said, as well as young advisors “we can mentor, help and provide resources for growth.”

Richardson Wealth is also in acquisition mode, Kapoor said, “identifying other [wealth managers] that don’t have the scale to compete” and are looking to join a national platform. “We intend over the next six months or so to start approaching them, having conversations and seeing which [businesses] have the right cultural fit.”

Kapoor added that Richardson Wealth is interested in acquiring an asset management platform “that has sufficient scale, is profitable and [is] looking for access to a network of advisors that could use their services.”

The market for consolidation, particularly among mid-market firms, is “hot right now,” said Kendra Thompson, partner at consulting firm Deloitte LLP in Toronto. Smaller firms looking to keep up with the service capabilities of larger players may see a merger as the best option. “They [may] take a harder look at the economics and realize they need more scale,” Thompson said.

Technological change, new regulations and shifting demographics will drive consolidation, Marsh said: “As the next 12 to 24 months play out, we’ll see the landscape change in the sense of who is building for the long term, like we are, and who is being built to be sold.”

Richardson Wealth also plans to leverage the Richardson family name as part of its strategic plan. The Richardson name on the door evokes the heyday of independent shops that carried their founders’ last names, Marsh said, back when “banks didn’t own everything.”

Said Sandy Riley, president and CEO of Richardson Financial Group Ltd. in Winnipeg: “[The Richardson name] sends an important message as to the nature and culture of the organization. Families that have been in business for multiple generations understand the issues of multi-generational wealth.”

Having the backing of Richardson Financial Group and RF Capital will also mean Richardson Wealth has the resources to fund its growth initiatives, Riley said: “There are all kinds of ways in which we’ll be able to fund this business.”

Kapoor said he believes there is room for strong independent firms to compete effectively.

“We think there’s a large community of Canadians who want to have a choice to go to an independent boutique, whether [that’s] Richardson Wealth, Wellington-Altus, Canaccord [Genuity Wealth Management] or many of the smaller firms,” Kapoor said.

“Canadians like to do business with someone other than a bank, and that segment of the market is what we’re all trying to appeal to.”