Federal and provincial governments have been reluctant to increase most tax rates in recent years — but wealthier taxpayers in the highest marginal tax bracket often are the only group targeted for rate increases.

Whether increasing taxes on the wealthy is good policy has been the subject of intense debate.

“I think it’s positive, in the sense that it can raise much needed revenue for new programs as well as [pay] for some of the pandemic programs,” said David Macdonald, senior economist with the Canadian Centre for Policy Alternatives in Ottawa. “And it’s progressive, in the sense that the people making more money are the ones who owe more [at] higher rates.”

Macdonald said increasing tax rates on the wealthy lets governments raise revenue without having to cut back on services. However, he suggested any increases would “probably [be] a couple of years away.”

Governments have tended to get more involved with program spending in recent years, said John Oakey, national director of tax services with Baker Tilly Canada, an accounting firm based in Halifax. An aging Canadian population, for example, has put a strain on health care, he noted.

However, raising rates on the highest bracket is “ultimately a negative thing because the higher the tax rate goes, the less entrepreneurial people tend to be,” Oakey said. “How high can the tax rate go until people start to revolt? We’re starting to see now where people are leaving Canada and going to lower-tax jurisdictions. They’re moving their capital outside Canada.”

Taxing higher-income groups without a negative impact on the economy can be extremely difficult, said Laurence Booth, a professor of finance with the University of Toronto’s Rotman School of Management. Over the long run, taxing the most productive earners “is not a great method for improving productivity and growth,” he added.

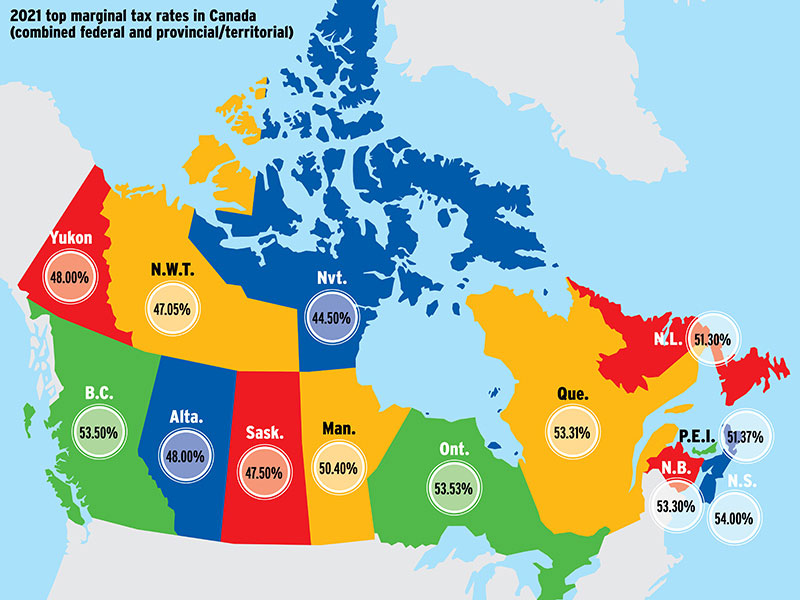

However, eight of the 10 provinces (see map) currently have a combined federal/provincial top marginal tax rate in excess of 50% on regular income.And in 2022, Newfoundland & Labrador will introduce three tax brackets for income above $250,000 and boost the province’s top tax rate by 3.5% — for a combined federal/provincial rate of 54.8% on income above $1 million.

Oakey said he expects governments to continue targeting wealthier Canadians for most tax increases, especially to address the unprecedented deficits that have accumulated during the Covid-19 pandemic.

Therefore, wealthier clients should have tax strategies in place to deal with rates that are already high and expected to increase.

Since different income sources are taxed at different marginal rates, clients in higher tax brackets should diversify their income sources to lower their average taxes payable, said Evelyn Jacks, founder and president of Winnipeg-based Knowledge Bureau Inc.

Clients should know the combined federal/provincial marginal tax rate for eligible dividends is lower than the effective marginal rate for capital gains in lower tax brackets, but higher than capital gains in higher brackets. The crossover bracket varies widely by province.

Jacks also suggested that advisors discuss with their clients the possibility of splitting income with lower-income family members. (Read “Year-end tax tips”, which discusses prescribed-rate loans.)

You also should ensure clients fully utilize tax-exempt savings opportunities within insurance policies. “Even if you’re paying high taxes during your lifetime or at death on that terminal return,” Jacks said, “you can shore up the tax differential by passing a tax-exempt life insurance policy on to the next generation, thereby offsetting the tax erosion on net family wealth.”

To reduce income subject to taxes, affluent clients in their 60s should consider whether postponing their CPP and old age security until age 70 is financially beneficial, and contemplate the opportunity costs of earning other income instead, Jacks said.

Oakey added that business-owner clients could consider taking advantage of the lifetime capital gains exemption by owning shares of their own company. As long as that company qualifies as an active business, these clients can shelter up to $892,218 in gains (in 2021) under the lifetime capital gains exemption when they sell those shares, he said.

Small business owners who invest within their Canadian-controlled private corporations should monitor the amount of passive income their investments generate, as the small business deduction begins to be clawed back after $50,000 in passive income. Passive income also is taxed at a higher rate than active income.

Business owners can also defer taxes by paying themselves a salary and then contributing to an RRSP, which also diversifies the risk of keeping all their funds in the corporation. But they should be aware they will owe payroll taxes on their salary.