Even though there were challenges aplenty in the past year, it proved to be a positive one for most Canadian equity balanced funds. Those funds benefited from a low interest rate environment and continuing global growth.

Looking ahead, fund portfolio managers are upbeat, but also very selective in their equities and fixed-income allocations.

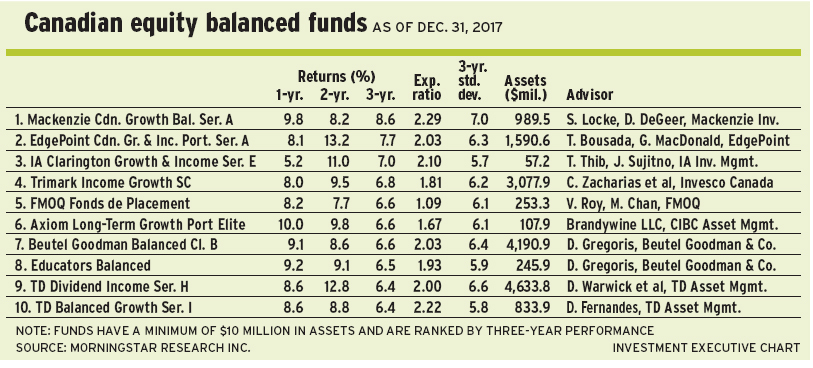

“People are getting worried that [economies] are long in the tooth. But [economic] growth has been subpar and inflation is not a problem,” says Doug Warwick, managing director with Toronto-based TD Asset Management Inc. (TDAM) and lead manager of TD Dividend Income Fund. “Growth has sometimes been disappointingly low. But we are seeing that global growth is gaining some momentum, so we’re at 2.5% to 3%. Back in the 1970s, when there were big inventory adjustments every cycle, you had big swings in [gross domestic product. Volatility] is much more muted now.”

Warwick admits he can’t foresee where economies may be going in three years or more. “But, looking at the next year, it looks pretty good to me,” he says, noting that, for example, U.S. unemployment rates are very low, at 4.1%, which is reminiscent of the 1970s.

“To me, everyone is climbing a wall of worry: issues such as North Korea and its nuclear weapons development and what [U.S.] President Trump might do; what’s happening in the Middle East; and Brexit,” Warwick adds. “As long as the [equities] market is concerned, it’s pricing in these things. When the market begins to ignore them, then you have to worry.”

Warwick shares portfolio- management duties with other TDAM personnel: Michael Lough, vice president; Elaine Lindhorst, vice president; and Geoff Wilson, managing director.

As far as risks are concerned, Warwick notes, interest rate hikes have been muted in the past couple of years, which should continue. “Central banks talk about raising interest rates, but [that process] will be slower than what the market expects,” he says. “Getting back to a ‘normalized’ rate will take several increases. If the [overnight] rate is going to be 2.5%, we have a long way to get there. [Outgoing Federal Reserve Board chairwoman Janet] Yellen was in no hurry to get there. New chairman [Jerome] Powell is in no hurry, either. The Bank of Canada also is a little cautious on rate increases because they impact the value of the dollar and [could] hurt Canadian manufacturing.”

Looking ahead, Warwick is bullish and anticipates that portfolio returns in 2018 will be positive. “Our longer-term expectation is high single digits – if we can pick the stocks that participate well in the economy. This would come in as what, we hope, will be an average year.”

From a strategic viewpoint, Warwick’s fund is fully invested.

Stocks account for 83% of the TD fund’s assets under management (AUM) and are distributed across 65 names.

A favorite holding is Enbridge Inc., a leading pipeline firm. This stock has been under pressure because of several factors, including negative sentiment by socially responsible investors. The share price has fallen in the past year to about $48 from $56. The stock has a 5% dividend yield. There’s no stated target. Says Warwick: “We like [Enbridge] because there are billions of dollars in approved, not yet built projects. Most of that is based on rates [set by energy regulators], so you can see an upward progression in earnings, cash flow and dividends because of those projects.”

Another favorite is Brookfield Asset Management Inc., which has holdings in asset management, real estate, infrastructure, renewable energy and private equity. The stock is trading at $53.40 and pays a 1.35% dividend. There’s no stated target. Says Warwick: “Management is superb. When their buildings get too expensive, they sell them and redeploy the money elsewhere.”

The TD fund holds about 16% of AUM in fixed-income: 57% of that portion is in investment-grade corporate bonds, 37% in government bonds and 6% in high-yield bonds. The average duration is about 6.5 years (about a year less than that of the benchmark FTSE TMX Canada universe bond index).

trying to determine the direction of the market is difficult, agrees Clayton Zacharias, vice president with Toronto-based Invesco Canada Ltd., and portfolio co-manager of Trimark Income Growth Fund SC. He also acknowledges that the market faces both headwinds and tailwinds.

“The current environment is pretty favourable for equities, in terms of low interest rates and low inflation, and solid economic growth in most parts of the world,” Zacharias says. “That’s why equities have done so well recently. But whenever the starting point is at a high level with respect to valuations, both on an absolute and a relative basis, there is a potential headwind from those high valuations. Not that I’m predicting an imminent market correction or the economy will go into recession. But you just have to be cognizant of the chance of a pullback or reversion to the mean.”

Much of the gains from the lengthy bull market has been due to the expansion of valuation multiples, which has been supported by earnings growth.

“Part of the reason [for the expansion] is that interest rates are already very low,” Zacharias says. “But over the next three to five years, rates are more likely to rise than to fall further. That’s a potential headwind to valuation multiples. We certainly would not want to invest on the basis of higher multiples.”

Zacharias shares stock- picking duties with Alan Mannik and Mark Uptigrove, both vice presidents with Invesco.

Although rising interest rates are a concern over the medium term, Zacharias also is worried about massive fund flows into passive ETF strategies: “We have seen indiscriminate buying of equities on the way up, and the shift to passive from active strategies has been quite dramatic. But what happens when that flow reverses? As equities decline, those inflows could turn into outflows. What will that mean for valuations as indiscriminate buying turns into selling? That poses a risk for equities.”

A bottom-up investor, Zacharias is running about 7% of the Trimark fund’s AUM in cash. That’s not a market call, but simply due to the stock-selection process.

“We’re always looking for compelling opportunities. But, to the extent that we can’t find them, we will default to cash,” he says. “So, finding compelling ideas is more difficult. We’re being patient and will not deviate from our investment discipline even though the market has gone up quite a bit and valuations are higher than normal. Risk management and downside protection are more important than swinging for the fences.”

From a sectoral standpoint, financial services is the largest sector on the equities side, at 31.9% (this includes a few non-traditional financials such as Brookfield), followed by 10.9% in technology, 7.3% in health care and 6.9% in industrials.

Running a concentrated portfolio of about 30 equities, Zacharias likes Bank of America Corp., which “enjoys the largest and lowest-cost retail deposit base [in the U.S.]. This is a meaningful advantage. Under the leadership of chairman and CEO Brian Moynihan, the bank has gone through a significant transformation over the past eight years. The balance sheet has been strengthened and operating costs structurally reduced. Despite a substantial appreciation in the stock price over the past year, I believe the valuation remains attractive for a business that will continue to compound its value.”

The stock is trading at US$29.50 (C$36.90) and pays a 1.6% dividend. Although Zacharias does not have a target for the stock, he believes that the discount to intrinsic value is about 20%.

Another favorite is Onex Corp., a Toronto-based private-equity firm that invests its own capital and that of third-party investors in a diversified mix of businesses. The stock is trading at $93 and Zacharias believes that’s at a 15% discount to net asset value.

“Given a very long track record of success and strong investment returns, Onex has the ability to raise a significant amount of capital on a regular basis,” says Zacharias, noting that Onex’s individual investment funds continue to grow larger over time. Onex’s own capital amounts to US$6.7 billion (C$8.4 billion) and about US$23 billion (C$28.75 billion) is held by outside parties. “Onex has a reputation for being a very good investor – not only within Canada, but also globally.”

On the fixed-income side, about 24% of the Trimark fund’s AUM is held in bonds, managed by Invesco vice president Alexander Schwiersch’s team and spread among 56% corporate bonds, 37% government bonds, 6% asset-backed securities and 1% cash. The average duration is 3.7 years.

“Given that in the coming years, interest rates are likely to be higher than they are today, we’re focused on downside risk management,” Zacharias says. “We’re not being compensated appropriately to buy long-dated bonds. The risk/reward [balance] is unattractive today.”