Two-thirds of canadians who work with financial advisors feel strongly that they’re taking advantage of tax-optimized registered accounts, according to the results of a recent survey.

This suggests that advisors are “bringing value to the table” by ensuring that most of their clients possess registered accounts such as tax-free savings accounts (TFSAs) and RRSPs, says Hugh Murphy, managing director of Credo Consulting Inc. of Mississauga, Ont.

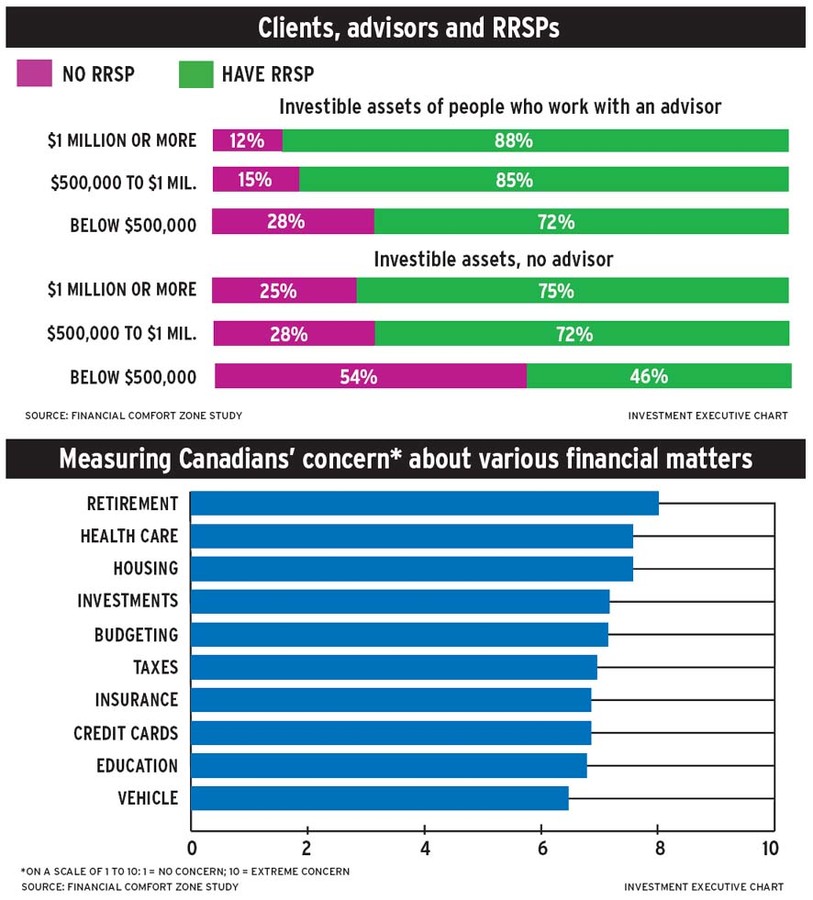

These findings are from the most recent edition of the Financial Comfort Zone Study, a national consumer survey conducted by Credo in partnership with Montreal-based TC Media’s investment group, which publishes Investment Executive. This edition of the survey examines Canadians’ thoughts on tax- optimized investing.

Competing financial priorities, such as paying off debt and purchasing a home, may be one reason that one-third of financially advised Canadians feel they are not maximizing the potential of registered accounts, says Curtis Davis, director of tax and estate planning with Toronto-based Mackenzie Financial Corp.

“Higher debt levels and debt payments [are] taking up a large portion of people’s income, which makes funds less available to maximize contributions to these other products,” says Davis. “If money is going [toward paying off debt, those people] are not putting as much money away as they could – and they’re worried about that.”

The survey found that Canadians who work with an advisor are substantially more likely to take advantage of tax-advantaged opportunities such TFSAs and RRSPs than people who don’t work with an advisor, says Murphy.

In fact, advisors have the largest impact on lower net-worth Canadians regarding RRSP ownership. Fewer than half (46%) of Canadians who don’t work with an advisor and who have less than $500,000 in investible assets have RRSPs. However, that figure leaps to 72% for people within that asset level group but who work with an advisor.

These lower net-worth individuals tend to be younger and have had relatively less time to build their assets. Thus, advisors have a critical role to play in coaching and educating this demographic on how registered accounts work and the importance of saving early in life, says Debbie Wong, vice president, longevity planning, with Toronto-based Raymond James Ltd. in Vancouver.

Competing financial priorities also may have a hand in the overall level of importance that Canadians give to the subject of taxes. The topic lands just outside of the top five priorities, which are retirement, health care, housing, investments and budgeting.

However, Canadians with higher levels of wealth are more likely to place more importance on tax matters. For example, 21% of Quebeckers with investible assets of $500,000 or more said that taxes are in their top two financial priorities, compared with 14% who have less than $250,000 in investible assets. This pattern is consistent throughout Canada.

One issue that worries wealthier clients is how taxation will affect the assets they can pass onto younger generations, says Davis.

Canadians with $500,000 or more in investible assets are commonly in their 40s, Wong says, and have begun to think about how to distribute their wealth to family members. “Once [these clients] get to $500,000, they start to feel more comfortable that they have a nice nest egg, and then they think about: ‘What should I be doing with it?'” Wong says.

You should pay attention to how your clients’ assets are growing, Wong says, and take the initiative to bring up the topic of tax planning. Clients may not think to ask about this, Wong notes.

The research also suggests there’s an opportunity for advisors to be more proactive with women clients. Slightly more than one-quarter (27%) of women are confident that they are maximizing their tax-optimized investment opportunities. However, this figure is trumped by the 34% of men who feel the same.

That difference may be attributable to divergent personality traits. Although men feel confident they are being proactive by simply making the investment, women tend to have more questions and want more time to explore the opportunities within the investment, suggests Davis.

The research makes clear there’s a great opportunity for you to bring that additional value to your women clients – as long as you answer those clients’ questions in a way that is straightforward and avoids financial jargon, says Murphy.

A report from Credo released in November 2015 stated that women are more likely than men to find jargon confusing or intimidating, and women who work with an advisor are even more intimidated by that factor than women without an advisor.

The online Financial Comfort Zone Study polled more than 13,000 Canadians. The survey is meant to gain insight into the relationships among financial advice, financial well-being and overall life satisfaction in Canadian society. Canadians are polled monthly, and the number of survey participants will grow each month.

© 2016 Investment Executive. All rights reserved.