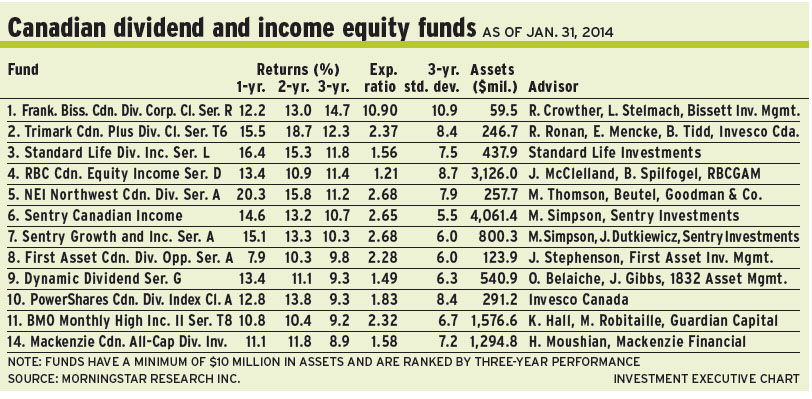

Canadian equities markets proved resilient last year in spite of below-par domestic economic growth. Going into 2014, portfolio managers of Canadian dividend and income equity funds are relatively upbeat while acknowledging the slowness of the economic recovery.

“I’m relatively optimistic about the Canadian stock market, although not all parts of it,” says Jennifer McClelland, senior vice president with Toronto-based RBC Global Asset Management Inc. (RBCGAM) and lead portfolio manager of RBC Canadian Equity Income Fund. “There are a lot of sectors that are very reasonably valued and have strong opportunities for earnings growth. It looks pretty choppy now; but if we see a pickup in the U.S. economy and in manufacturing activity, there are a lot of Canadian sectors that are well positioned to benefit.”

In particular, McClelland (who shares portfolio-management duties with Brahm Spilfogel, RBCGAM vice president) points to some industrials, materials and energy firms that might do well – even though commodities prices have been volatile.

“Within energy services and pipelines,” says McClelland, “there’s a lot of activity going on. But in a lot of cases, that positive earnings momentum isn’t necessarily priced into our stocks.”

She adds that Canadian banks, which represent about 20% of the benchmark S&P/TSX composite index, also are reasonably valued despite potential challenges in the form of indebted consumers.

The wild card is the outlook for the materials sector, which has been hit by weak commodities prices. “If we don’t see another negative year, non-Canadian investors will look at our market again. There’s a lot of foreign capital that might come back in,” says McClelland, adding that worries about emerging markets are casting a pall over Canadian stocks.

“I’m not a big investor in that [emerging markets] sector,” she says. “But the stocks have reflected a negative scenario over the past couple of years. The end to the bleeding will be pretty positive for our market.”

Bottom-up stock-pickers, McClelland and Spilfogel are building a portfolio that can both benefit from an improving economic outlook or, conversely, withstand a deteriorating one.

“We try to create a balance in the portfolio,” says McClelland, “so that it can hold its own in either a positive or negative scenario and [be] protected from downside risk, whether it is rising interest rates or a recession.”

From an asset-allocation viewpoint, about 32% of the RBC fund’s assets under management (AUM) is in financials (banks, insurance firms, real estate investment trusts and non-banks), followed by 31% in energy (producers, pipelines and service firms), 11% in industrials and smaller weightings in sectors such as utilities and consumer staples.

One favourite name in the portfolio, which holds about 120 positions, is Newalta Corp., which specializes in industrial and oilfield waste-management services. “[Newalta has] been quite innovative in devising new technologies to help either recycle waste oil or treat wastewater,” says McClelland, noting that the firm is active in the oilsands and expanding into the U.S. “It’s benefiting from a pickup in activity, but not as exposed to the commodity price.”

Newalta shares, which pay a 2% dividend, are trading at about $16.50 each, or roughly 7 times enterprise value to earnings before interest, taxes, depreciation and amortization. There is no stated target.

Equally optimistic is Kevin Hall, managing director with Toronto-based Guardian Capital LP and portfolio co-manager of BMO Monthly High Income II. “Overall, we are constructive for 2014,” says Hall, who shares portfolio-management duties with Michele Robitaille, managing director with Guardian.

“A year ago,” says Hall, “equities markets benefited from a material multiple expansion. You could see some modest multiple expansion this year, but not to the same degree as in 2013. We are now around the long-term average.”

Hall notes that stocks have risen to a price/earnings multiple of 15 on a forward earnings basis from around 13: “There’s some room for multiples to go up, driven partly by continued recovery in the U.S. economy. The U.S. housing market continues to improve nicely and the job market, while not stellar, is still decent. A recovering U.S. economy will provide a decent tailwind for our economy.”

Combined with a soft landing in China, whose gross domestic product growth is around 7%, this leads to a generally positive outlook.

As for Europe, Hall argues that many risks remain in the region: “We view it as going through a long, painful recovery that is susceptible to further downside.

“The worst appears to be behind them,” Hall adds, “but equities markets can do well with the U.S. and China moving in the right direction, even if Europe continues to stumble along.”

Although the BMO fund’s returns were in the mid-teens last year, Hall is expecting them to be less robust in 2014: “But even with a little multiple expansion, combined with a 3% dividend yield, based on the S&P/TSX composite, that would get a total return of 8%-12%.”

Running a portfolio of about 40 names, Hall and Robitaille have about 39% of the BMO fund’s AUM in financials (15% banks, 15% real estate investment trusts and 9% diversified financials), 31% in energy (19% oil and gas producers and 12% in infrastructure and pipelines) and smaller holdings in sectors such as industrials.

A favourite is Intact Financial Inc., the largest property and casualty insurer in Canada. “We think [it has] a very sustainable competitive [advantage], given its size and scale,” says Hall, noting that the firm is likely to benefit from rising premiums following a series of natural disasters.

Although Hall admits that Intact’s 2.6% dividend yield is middle of the road, the real objective is total return potential. “On a total return basis,” he says, “it’s a very attractive stock.”

Intact stock is trading at about $66.50 a share. There is no stated target.

As a value-oriented investor, Hovig Moushian, senior vice president with Toronto-based Mackenzie Financial Corp. and portfolio manager of Mackenzie Canadian All-Cap Dividend Fund, is cautiously optimistic.

“Valuations are in and around the historical average,” says Moushian. “The market is not inexpensive or overly expensive. In the U.S., we have seen a substantial amount of multiple expansion. Our view is that it’s not reasonable to expect further expansion. When you combine that with earnings growth in the 5%-6% range, you’re looking at 5%-6% market appreciation and 3% in dividends. It’s reasonable to expect 7%-9% total return over the course of 2014. That’s not our forecast but a reasonable view to have in the context of what we’ve seen in the marketplace.”

The recovery of the U.S. economy, whose growth is a key factor in Canada’s economy, says Moushian, is much slower than in past economic recoveries.

“That’s connected to the continued large debt burden and how it has suppressed the ability to grow,” he says. “You see it every day in areas such as job creation, which is not anything to write home about. But it is positive. Our view is that trend is likely to continue.”

As a consequence, Moushian believes a slow growth environment will drive 7%-9% total investment returns in 2014.

Moushian has allocated about 31% of the Mackenzie fund’s AUM to financial services (dominated by a 19% weighting in banks), plus 25% to energy (a mix of producers, pipelines and services), 9% to industrials, 9% to materials and smaller holdings in sectors such as consumer discretionary.

Running a portfolio with 62 holdings, Moushian continues to favour SNC-Lavalin Group Inc., the global engineering firm that was mired in corruption scandals in 2011-12. “The bulk of the issues are behind them,” says Moushian, who bought the stock after the scandals emerged. “There is a new management team in place and they’ve taken many steps to clean up the structure of the business, such that the fraudulent activity that occurred in the past is not likely to happen in the future.”

The chief attraction, though, is SNC-Lavalin’s stakes in infrastructure projects, such as Ontario’s toll Highway 407, which generate stable income.

SNC-Lavalin stock is trading at $46 a share, or 17.6 times earnings. The dividend yield is 2%. Moushian believes that fair value is around $50 a share.

© 2014 Investment Executive. All rights reserved.