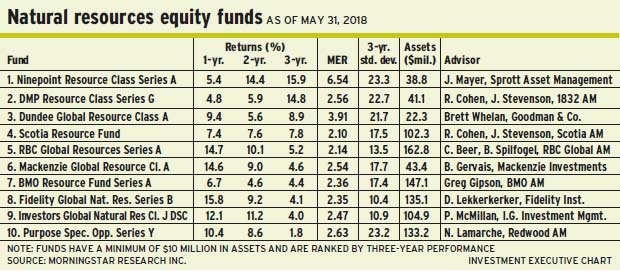

Fund portfolio managers in Morningstar Canada‘s natural resources category face the challenge of finding investments in industries that are linked to commodity prices. Although these funds’ mandates are relatively narrow, the portfolio managers are able to diversify across a handful of industries, including precious metals, energy, forest products and base metals, as well as related businesses, such as chemicals, packaging and resources equipment.

Mutual funds in the natural resources category have been helped recently by a surge in the price of crude oil, which rose into the US$71 a barrel range in May from US$60 in early March before falling back slightly, as measured by the benchmark price for West Texas intermediate crude (WTI).

That rise helped the Morningstar natural resources equity fund index achieve a 6% gain in April alone, thanks to the funds’ stakes in energy stocks. The price of oil has been as high as above US$100 a barrel in 2014 and as low as $42 in June 2017, indicating how volatile commodity prices can be.

Few portfolio managers of resources funds attempt to predict commodity prices in selecting stocks for their portfolios. Although the recent gain in oil has been a boost, higher prices ultimately lead to rising global output and lower demand, which dampens prices.

Saudi Arabia and Russia have signalled that they’ll increase output, and the OPEC countries also have suggested they may increase production in the second half of this year. U.S. crude production climbed to 10.47 million barrels a day in March – a monthly record, according to data from the U.S. Energy Information Administration. On the other hand, reductions in supply from Venezuela and Iran, due to recent U.S. sanctions, are anticipated.

Canadian oil producers have been constrained by a lack of pipeline capacity to the west coast and the U.S., as well as a shortage of railway tanker cars. These shortfalls have created a negative price differential that has hurt Canadian companies. The discount on heavy oil received for Canadian crude relative to the WTI price has been as great as US$30 this year, which has been painful for producers with properties in Canada.

How quickly these bottlenecks will be eased by the federal government’s recent $4.5-billion purchase of the TransMountain Pipeline from Kinder Morgan Canada Ltd. remains to be seen. Canada’s proven oil reserves are the third-largest in the world, and could be a huge source of wealth if their production isn’t landlocked anymore.

Canada’s inability to get a pipeline built to the coast because of political squabbles, court challenges, environmental protests and other delays has tarnished the perception of Canadian energy companies among international investors, and depressed stock prices. New obstacles may arise during the construction phase with the nationalization of the pipeline. Although the federal government has stated it doesn’t intend to be a long-term owner, any deal to resell the pipeline has yet to be negotiated.

Meanwhile, in another important resources category, sagging prices for gold bullion in recent years have curtailed exploration projects, and there have been few new discoveries. According to the World Gold Council, production of 3,298 tonnes of gold in 2017 was barely higher than the 3,277 tonnes produced in 2016. Rather than waiting for higher bullion prices, portfolio managers of resources funds are focusing on companies with promising deposits and efficient mines that keep these firms’ costs down.

“The resources sector does well at the mid- to end of the economic cycle,” says Benoît Gervais, senior vice president, investment management, leader of Mackenzie’s resources portfolio team and portfolio manager with Mackenzie Financial Corp. “When we have synchronized economic growth around the globe, that creates the kind of sustained demand needed to deplete inventories and boost prices.”

The opportunities to beat benchmark indices in the resources sector lie in unearthing opportunities in mid-cap stocks, Gervais says, as the more stable, large-capitalization giants tend to dominate indices. Currently, Mackenzie Global Resource Fund’s weighting is 55% in energy, including pipelines, distributors and refiners; and 45% in materials, including metals and mining.

“We look for mid-cap companies that can generate sustainable growth and free cash flow over time,” Gervais says.

The Mackenzie fund’s global mandate allows Gervais to look beyond Canada for investment opportunities. Although 30% of the fund’s assets are held in Canada, 42% is held in the U.S. and there are holdings in Europe and Africa.

“There are transportation bottlenecks in Canada,” Gervais says, “and although the problems are fixable, that may take several years.”

In the U.S., the cycle still is on the upswing in the housing sector, which augurs well for building materials such as lumber, Gervais says. As economic growth continues at a healthy pace, he adds, improving employment and wages will lead to more demand for housing.

One of the Mackenzie fund’s top holdings is copper producer First Quantum Minerals Ltd., which has a massive mine project coming into production in Panama later this year. Few other companies are building mines because of low copper prices, but Gervais foresees growing copper demand, particularly as electric cars become more popular. There can be as much as 100 pounds of copper in an electric car, he says.

“I’m a believer in the electrification of society, and that means more batteries, wires and charging stations,” Gervais says. “We’re moving toward clean energy sources with lower carbon emissions, such as natural gas and electricity.”

In line with the clean energy theme, another top holding in the Mackenzie fund is Williams Cos. Inc., a natural gas gathering, processing and transmission firm. One of the firm’s key projects is a natural gas pipeline in the U.S. that connects the northeast to the Gulf coast, where coal plants are being replaced. The fund also holds Tourmaline Oil Corp., which has extensive land position and control of natural gas processing and transportation infrastructure in promising regions in British Columbia and Alberta.

Another top holding in the fund is Noble Energy Inc., a Texas-based oil and gas producer with a large gas find in the eastern Mediterranean Sea close to markets in Israel, Jordan and Egypt.

“There are many years of growing natural gas consumption ahead,” Gervais says.

Jason Mayer, senior portfolio manager with Sprott Asset Management LP in Toronto and subadvisor to the Ninepoint Resource Class fund, says he uses a bottom-up style. That approach, he says, leads him to small-cap to mid-cap companies and offers a better chance of finding attractive valuations.

“We look for world-class assets,” Mayer says. “We can find more hidden gems in the small-to mid-cap space, as the companies are not as well covered by analysts.”

For example, the Ninepoint fund invests in NexGen Energy Ltd., which has uranium properties in the Athabasca Basin in Saskatchewan, near the producing deposits of giant Cameco Corp.

The Ninepoint fund’s biggest weighting is in gold companies, which accounts for 45% of the fund’s assets. Energy is next, at 26%, followed by base metals, at 12%. Although there has been a lacklustre market for gold bullion in the past several years, Mayer says, some companies have managed to control costs and increase free cash flow.

“A lot of gold companies have been financial disasters with capital overruns – burning through cash,” he says. “But there also are those that have battened down the hatches, righted the ship and gotten in line, and free cash-flow yields are impressive.”

Patience is called for, Mayer notes, as there is “complete disinterest” in gold stocks in the stock market and speculators are finding more excitement in marijuana or cryptocurrency plays.

Looking longer term, Mayer remains optimistic. He regards gold as the world’s oldest currency, with a history of maintaining its purchasing power.

Mayer expects widespread currency devaluation will be “a supportive tailwind” for gold someday. In the meantime, he looks for companies with strong operating mines, low costs and high cash flow. Among the Ninepoint fund’s top gold-mining holdings are Continental Gold Inc., Roxgold Inc. and Kirkland Lake Gold Ltd.

On the energy side, a key holding of the Ninepoint fund is Yangarra Resources Ltd., a junior oil producer in Alberta with high rates of growth and a high rate of success in its drilling program. The fund also holds Parex Resources Inc., a Calgary-based company with Colombian oil properties that are unaffected by the transportation constraints of Canada.

In base metals, Mayer favours Arizona Mining Inc., which is developing a promising zinc asset. Zinc is used primarily for galvanizing steel.