Emerging markets have performed well this year, driven by improving currencies, economic fundamentals and less dependence on commodities. These markets have surpassed the gains of the MSCI world index by a margin of about 10 percentage points.

Fund portfolio managers, such as Alpha Ba, vice president with Toronto-based AGF Investments Inc., and Philippe Langham, head of emerging-markets equities with London, U.K.-based RBC Global Asset Management (U.K.) Ltd., are upbeat about the prospects for emerging markets based on the narrowing of the discount on emerging markets stocks as compared with developed markets stocks.

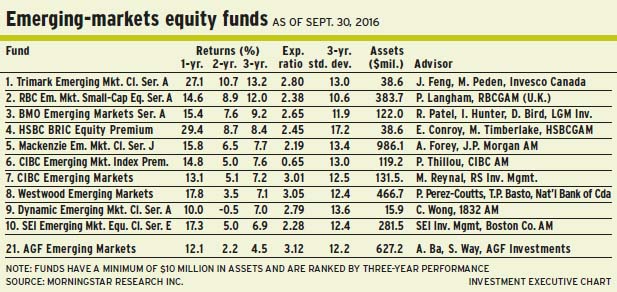

“There are seven reasons that explain the outperformance of emerging markets,” says Ba, portfolio co-manager of AGF Emerging Markets Fund. He shares portfolio-management duties with Stephen Way, senior vice president with AGF. Ba’s reasons:

– Emerging markets were trading at attractive valuations relative to developed markets at the beginning of 2016.

– Earnings estimates were more realistic than in 2015 and there were fewer negative revisions this year.

– Emerging markets interest rates began to drop in 2016 and supported equities valuations.

– There was declining political risk in a number of emerging markets relative to developed markets.

– More reforms have been introduced in countries such as India, Indonesia and Mexico.

– Competitive currency devaluations that occurred last year are over and several currencies have begun to appreciate.

– Commodities prices have formed a bottom. “Energy and materials have rebounded slightly this year after the bloodbath of 2015,” says Ba.

However, there are some risks on the horizon. One risk is China’s heated property market.

“It’s not yet a bubble, but points to an unsustainable rise in certain areas,” says Ba. He notes that housing prices in cities such as Shanghai are at risk of a correction with widespread ramifications.

The second risk centres on lower commodities prices. “Although other sectors have taken over, commodities still are an important part of the macroeconomic story,” says Ba, noting that commodities account for about 14% of the benchmark MSCI world index, down from 30% in 2010.

Finally, a strong U.S. dollar (US$) would hurt emerging-markets corporations especially and make servicing US$- denominated debt difficult.

Still, Ba is upbeat because returns on equity are on the rise in emerging markets. “That is driven by margin expansion,” he says.

“The big development in 2016 was that real wage growth in emerging markets now is lower than productivity growth for the first time since 2010,” Ba says. “This is the reverse of [the situation in] developed markets, where wage growth has been higher than productivity growth since 2015.”

When real wage growth is slower than productivity growth, that results in margin expansion, says Ba, who adds that margins were at a historically low level for several years.

“With this development, margins can start to expand in emerging markets, whereas in developed markets, margins are peaking if not falling,” says Ba.

About 22% of the AGF fund’s assets under management (AUM) is in China/Hong Kong, 13% is in India, 8% is in Taiwan and 8% is in Mexico, with smaller weightings in countries such as South Africa. Ba, a bottom-up investor, looks for companies with return on invested capital (ROIC) that exceeds the cost of capital.

A top holding in the 70-name AGF fund is India-based UPL Ltd., a mid-cap firm that is a global player in the crop protection industry. UPL generates 18.5% ROIC.

“We believe that margin upside has been underappreciated by the market and will be driven by a shift toward branded products and operating leverage.”

UPL stock is trading at about 675 Indian rupees (INR) or $12.30 a share. The target is INR1,000 a share within two years or so.

Valuations were very attractive at the beginning of the year and currencies were cheap in emerging markets, Langham agrees. He is portfolio manager of RBC Emerging Markets Equity Fund.

“We began to see economic momentum improve [in emerging markets], while momentum has been somewhat slowing in developing markets. Also, there have been signs of improving profitability [in emerging markets,” says Langham. “There is a strong link between those two factors and relative performance of emerging markets. These have been the key reasons for strong performance.”

Return on equity had been falling for some years, largely because of overcapacity and rising wages, says Langham.

“We have begun to see cap-ex [capital expenditures] moderate, and wages also have moderated along with improvements in productivity and economic growth. These factors support improvements in earnings.”

As for risk factors, Langham says that one of the major worries at the beginning of the year was a devaluation of China’s renminbi.

“But that is looking increasingly unlikely,” says Langham, noting that authorities in China are not in favour of a large devaluation. “Having a much weaker currency would not make sense.”

Second, a strong US$ would hurt emerging-market firms that borrow in US$ and would also make US$-denominated commodities more expensive. However, Langham argues, US$ strength appears to be coming to an end, and certainly against emerging-market currencies.

More important, global gross domestic product (GDP) growth could turn out to be worse than expected. “The big risk is that global growth will disappoint – and that will be negative for all equities markets,” says Langham, adding that downward revisions to estimated growth figures have become the norm.

“My central scenario is that [GDP] growth does not disappoint. But it is a risk,” says Langham, who anticipates that policy-makers will turn their attention toward fiscal measures and away from monetary easing.

Langham, like Ba, points to reforms that will drive improvements in emerging markets’ GDP growth: “I am seeing lots of signs of reform in many countries: India, Indonesia, Malaysia, Mexico, Peru, and even China. [The last], for all the bad press it gets, is trying to reform its economy,” he says. He notes that, invariably, periods of sluggish GDP growth are reversed as countries introduce reforms.

Langham says that stocks hit valuation levels at the beginning of the year that were the lowest seen in many years: “Valuations now have become a little more expensive. But, compared with long-term averages, they still are quite attractive.”

Emerging markets stocks trade at a 30% discount to developed markets on a price/book basis. “Long term, a 10% discount would be more reasonable,” he says.

Langham is a bottom-up investor. About 14.9% of the RBC fund’s AUM is in India, 13.2% is in China, 10.7% is in South Korea, 9.8% is in Taiwan and 9.6% is in South Africa, with smaller holdings in countries such as Brazil. Langham says country weightings are a byproduct of the stock-picking process.

A favourite name in the 60- stock RBC fund is SM Investments Corp., a Philippines-based conglomerate that operates a leading bank and mall operator.

“[SM’s] penetration in many areas, such as credit and consumer discretionary, is relatively low,” says Langham. “SM is dominant in each of the areas in which it operates and has benefits of scale.”

SM generates an ROIC of about 20%. SM stock is trading at PHP671.50 ($17.25) a share, or about 2.8 times book value. There is no stated target.

A variety of factors have been driving emerging markets, making the crafting of general statements about these markets difficult, says Rishikesh Patel, portfolio manager, India and global emerging markets, with London, U.K.-based LGM Investments Ltd. (a unit of Toronto-based BMO Global Asset Management Corp.) and portfolio co-manager of BMO Emerging Markets Fund. He shares portfolio-management duties with LGM portfolio managers Irina Hunter and Damian Bird.

“Brazil has been the best- performing market, but performance seems to have decoupled with what has been happening on the ground. The economy continues to contract, there’s been political change and accusations of corruption,” says Patel. “And yet, the market is up by 60%.”

Conversely, India has pushed through key reforms, he says, yet its market is up by only single digits year-to-date.

“It’s difficult to make broad-brush statements about what is driving the rally [in emerging markets]. At LGM, we don’t allow short-term ‘noise’ to affect our decisions,” says Patel. “We look at the specific drivers of growth. Whether last year or this year, the strategic case for investing in emerging markets remains unchanged.

“You will have periods of stocks running up – as they are now – or running down,” Patel adds. “Fundamentally, the case for emerging markets is unchanged, and they remain an attractive category to be invested in.”

Patel and his team are bottom-up investors and study structural growth trends. In particular, Patel notes, countries with low GDP per capita, such as Indonesia and Thailand, are experiencing rising disposable income, thus bringing changes to spending habits.

“People who were having a basic existence are getting their first credit card or opening a bank account. This is the kind of structural growth trend that we focus on,” Patel says.

“Some of these markets tend to be very underdeveloped and unorganized in terms of retail or banking penetration,” he adds. “Companies that are well entrenched tend to have a wider moat around them and can grow and sustain their cash flows, thus benefiting from emerging trends.”

As an outcome of the bottom-up stock-picking process, about 28% of the BMO fund’s AUM is in India, 18% is in Indonesia, 10% is in Philippines and 10% is in Mexico, with smaller holdings in countries such as Brazil.

A favourite holding in the 46-name BMO fund is India-based Yes Bank Ltd., which opened in 2003 with one branch and now has 850.

Although Yes Bank has a 1% market share on the corporate side, says Patel, the bank is just beginning to grow on the retail side: “In terms of room to grow, [the bank] has tremendous potential.” Yes Bank stock trades at INR1275 ($23.30) a share, or at about three times book value. There is no stated target.

Another favourite is Mead Johnson Nutrition Co., a U.S.-based producer of infant formula that derives about 80% of revenue and profits from emerging markets.

“[Mead Johnson] is a good-quality company and has very good governance. [The stock] was available at a bargain,” says Patel, who notes that Mead Johnson stock was punished because the firm was slow in adapting to changes in the market.

Mead Johnson stock, acquired early this year, is trading at about US$80.50 ($103) a share and pays a 1.65% dividend. “[The stock] is trading at an attractive 3.8% free cash-flow yield,” Patel notes.

© 2016 Investment Executive. All rights reserved.