Precious metals and the mutual funds that invest in related equities have lost some of their shine recently, as investors have been distracted by more enticing opportunities to grow their wealth using other assets.

Portfolio managers of precious metals funds are familiar with the category’s propensity to fall in and out of favour, and are anticipating that gold and other precious metals, such as silver and platinum, will shine again and prove their value as both portfolio diversifiers and stabilizers in times of financial market turmoil.

Although global stock markets have had a terrific run for the most part since they bottomed in March 2009 after the global financial crisis of 2008-09, the price of gold bullion topped at around US$1,900 an ounce in September 2011 and has been on an uneven downward slide since. Bullion was hovering around US$1,200 in mid-September, with gold stocks sagging as well.

The most important elements in the behaviour of gold, the king of precious metals, are the level of real interest rates, the U.S. dollar and investors’ sense of risk or need for a safe haven.

With the U.S. Federal Reserve Board in the process of implementing an anticipated total of four interest rate hikes in 2018, the opportunity cost of holding gold has been rising. Gold pays neither interest nor dividends and tends to perform best when real interest rates are negative relative to inflation.

Inflation has been relatively benign, running just above 2% in Canada and the U.S., but there are signs that it could pick up – and that might inject some life into precious metals. For example, massive tax cuts in the U.S. have succeeded in stimulating economic growth and creating jobs, and these trends are potentially inflationary.

In addition, tax cuts and rising expenditures in the U.S. also have contributed to a surge in government borrowing under President Donald Trump as that country’s federal deficit edges toward US$1 trillion. History has shown that skyrocketing debt and fiscal irresponsibility, over time, can erode the value of currencies as money supply rises.

Gold bullion often does well when major currencies are losing purchasing power. The historical association of gold as the ultimate store of value goes back thousands of years and is rooted deeply, as more gold cannot be printed. Gold also has value as a safe-haven asset and its price typically rises when there’s turbulence in financial markets.

The past decade has seen a shift in the behaviour of central banks around the world with respect to gold, triggered by the global financial crisis. Central banks in emerging markets have increased gold bullion purchases, and European banks have ceased selling. Although the period between 1987 and 2009 saw central banks sell 7,853 tonnes of gold, the trend reversed between 2010 and 2016, when 3,297 tonnes were bought, according to the U.K.-based World Gold Council.

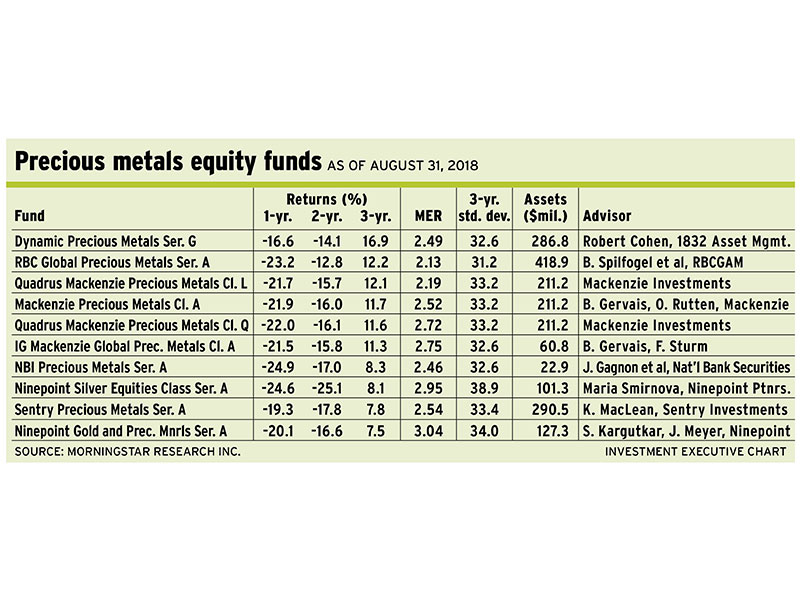

Robert Cohen, vice president and portfolio manager with Toronto-based 1832 Asset Management LP and lead manager of Dynamic Precious Metals Fund, fo-cuses on picking superior companies for that fund rather than trying to forecast precious metals prices.

“It’s hard to predict the bullion price with clarity, and I’m not sure that would help us make money,” Cohen says. “We look for best-in-class companies.”

As a mining engineer who formerly worked in that field, Cohen likes to model mining company scenarios “from the ground up” and doesn’t rely on analysts’ research from the Street.

“We look for ounces in the ground surrounding existing mines, well-rounded management teams and technology expertise,” Cohen says. “We want companies that are finding a lot of gold surrounding the drill bit and doing it efficiently.”

The Dynamic fund is permitted to invest globally, and the top holding is Northern Star Resources Ltd., an Australia-based company that, Cohen says, is producing 600,000 ounces of gold a year – and growing.

Several of the Dynamic fund’s holdings have properties in Australia. Cohen says land title and permit issues tend to be resolved quickly in that country. In addition, there is a lot of flat terrain accessible for drilling and good weather most of the year.

“There are people with a lot of technical expertise running the companies,” Cohen says, “whereas, in Canada, there are a lot of companies run by accountants.”

The Dynamic fund has a handful of holdings with key assets in West Africa, he adds, although those companies may be headquartered in Canada or Australia. For example, Roxgold Inc., B2Gold Corp. and Semafo Inc. are listed in Canada, but have properties in Africa and other locations. Australia-based companies with West African holdings include Cardinal Resources Inc. and Oklo Resources Ltd.

The U.S. is fairly well “combed over,” Cohen says, and there haven’t been any new discoveries there for a while. After Australia, Canada is the Dynamic fund’s largest geographical weighting, with Agnico Eagle Mines Ltd. and Kirkland Lake Gold Ltd. also among the portfolio holdings.

Aside from major producers, the Dynamic fund holds about 5% its assets under management (AUM) in smaller companies with a market capitalization of less than $100 million. Currently, there are about seven companies in this group. There also is about 2.5% of AUM held in private companies expected to provide a “lift” when they go public.

“We like to have a toehold in smaller [companies] with good geology,” he says, “without betting the farm.”

Although most of the Dynamic fund’s AUM is invested in gold companies, there’s some diversification. The fund holds shares in silver-mining company MAG Silver Corp., as well as in Largo Resources Ltd., which produces vanadium. (A key use of of vanadium’s is to strengthen rebar. After several years of poor quality rebar being used in China’s construction, authorities there are cracking down on quality control, Cohen says.)

Largo owns a large vanadium mine in Brazil that entered “harvesting mode,” beginning production earlier this year, Cohen says. The Dynamic fund invested in a secondary stock issue by Largo in July.

“Largo has been under the radar with no broker coverage,” Cohen says, “and it was a good opportunity.”

Brahm Spilfogel, vice president and senior portfolio manager, Canadian equities, with Toronto-based RBC Global Asset Management Inc. and portfolio co-manager of RBC Global Precious Metals Fund (along with Chris Beer and Jeffrey Schock), says the price of gold bullion has been in a bottoming process since 2011. He expects a turnaround, but says the timing is difficult to call.

“We are focusing on companies that can grow their resources and cash flow in a flat commodity-price environment,” Spilfogel says.

Although the RBC fund invests in all sizes of companies, Spilfogel says, the best opportunities are being found in intermediate producers, which account for about half of the fund’s assets: “Our top 10 are mostly intermediate producers, [for which] we anticipate 20%-30% annual production growth over the next two to four years.”

Valuations relative to earnings are about half of what they were when gold was flying high seven or eight years ago, Spilfogel adds. With less analyst coverage of the intermediates relative to the senior companies, there’s an opportunity to uncover promising companies before they’re recognized widely and thus priced higher.

The top holding in the RBC fund is Kirkland Lake Gold, which accounts for 10% of the fund’s AUM after enjoying strong price appreciation this year and in 2017. Spilfogel says the firm has two of the best underground mines in the world, one in Canada and one in Australia, and also has lots of cash on the balance sheet.

Other top holdings include Agnico Eagle Mines, which has a strong management team and two attractive projects in Canada, and Endeavor Mining Corp., which is ramping up two mines in Africa.

“There’s a bit of political unrest in Africa, but the assets are low-cost, high-rate-of-return projects that we expect to be revalued higher,” Spilfogel says.

The RBC fund holds up to 25% of AUM in junior companies, which Spilfogel calls an “acorn strategy”: “A few of these small companies will turn into oak trees. We’ll take a small position, carefully watch how plans are unfolding or how the ore grades are coming in as exploration proceeds, and throw out what’s not working.”

A couple of the smaller names in the RBC fund include Continental Gold Inc., an exploration and development firm that has a promising property in Colombia, and Wesdome Gold Mines Ltd., which is enjoying healthy production growth from a couple of operating mines in Canada and is seeing good drilling results from its Kiena deposit in Quebec.