Stocks of firms based in Europe have taken a bruising, thanks to the Brexit referendum’s result, which will see the U.K. leave the European Union in 2019 or later; that result was not expected by the financial markets. Meanwhile, concerns have emerged about the European Central Bank’s (ECB) quantitative easing (QE) policy, which has resulted in negative bond yields that hurt the region’s banks.

Some fund portfolio managers are cautious on prospects, especially those subject to the impact of Brexit. Other portfolio managers are more bullish and argue that the fears are exaggerated.

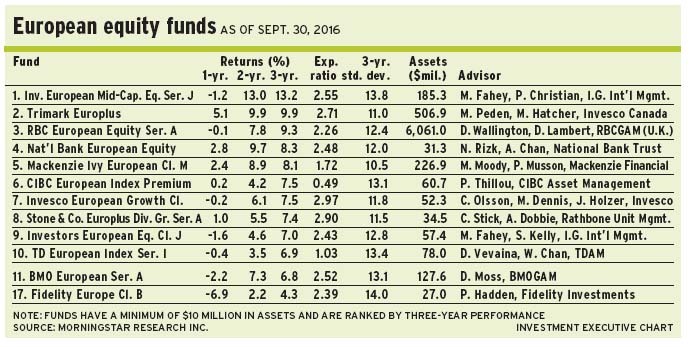

One of those in the latter camp is Matt Peden, vice president with Toronto-based Invesco Canada Ltd., and lead portfolio manager of Trimark Europlus Fund. He notes that the immediate expectation that the Brexit vote will spell disaster has been laid to rest.

“Mark Carney, head of the Bank of England, was quite negative in his predictions, as was the former chancellor of the exchequer, George Osborne,” says Peden. “Part of that was scare tactics to get voters to vote in the direction they felt best. But people have come to the realization that [the aftermath of the vote] is not going to be an immediate severe crisis. There may not be a severe recession or much of a downturn – just slower growth going forward.” He adds the formal exit process may not begin before next spring.

Meanwhile, Europe’s economy remains sluggish and countries such as Germany, which are heavily dependent on export markets – China, for example – are feeling the pinch. “China had a sizable fiscal expansion in the first half [of this year]. There are some signs [that economy] is pulling back in the second half.”

What’s more, there are rumblings that the ECB’s QE policy is not working and economic growth will come only through tax measures, says Peden: “[The ECB is] reaching the limits of how much further [it] can use QE. [Progress] comes down to fiscal policy. But governments are highly reluctant to do this, especially in northern Europe, which is more disciplined in the budgeting process.”

From a valuation standpoint, stocks are expensive and trading at elevated levels, Peden notes. The benchmark MSCI Europe index is trading at 20.9 times earnings on a trailing basis and at 14.9 times on a forward basis. However, the MSCI world index is trading at 21.3 times on a trailing basis and at 16.2 times on a forward basis.

“The differential is smaller between trailing and forward multiples for world stocks,” he says. “That indicates to me that analysts are being most optimistic on European stocks.”

Peden is cautious. About 20% of the Trimark fund’s assets under management (AUM) is held in cash. The U.K. is the largest country exposure, at 28.2% of AUM, followed by Ireland (10.6%), France (9.9%) and the Netherlands (6.5%), with smaller holdings in markets such as Germany.

A bottom-up investor, Peden likes small-cap names such as Electrocomponents PLC, a U.K.-based distributor of supplies and services to engineers in leading global markets. Electrocomponents stock is trading at about 347.15 pence ($5.77) a share. There is no stated target.

THE U.K.’S EXIT FROM THE EU is certain and unavoidable, says David Moss, head of European equities with London, U.K.-based F&C Management Ltd., a subsidiary of Toronto-based BMO Global Asset Management Inc., and portfolio manager of BMO European Fund.

“Theresa May, the [U.K.’s]prime minister, has been pretty clear and said, ‘Out means out.’ [The withdrawal] will happen,” Moss says. “But the time scale has been dragged out.”

May declared in October that the U.K. will invoke Article 50 of the Treaty of the European Union, which will trigger the exit process, before the end of next March.

Meanwhile, the U.K. has scrambled to assemble a negotiation team and develop policy positions. “The U.K. knows what it wants to achieve and where the trade-offs will come. And there will be some trade-offs,” says Moss.

Ironically, little appears to have changed regarding the U.K. economy, even though some economists expressed concerns.

“Most companies that have reported results have said not much has changed. Sales in June, July and August have carried on in the same trend,” says Moss. “[Gross domestic product (GDP)] forecasts have been downgraded for this year and next. But they are still positive. And compared with most of Europe, they are at OK levels.”

Still, Moss acknowledges, there are numerous risks on the horizon. These include the failure of QE to stimulate GDP growth and a referendum in Italy this autumn in which the government is seeking support for reform of the upper house. More important, lack of confidence could have adverse spillover effects on Italy and its place within the EU.

Moss admits stocks are not cheap from a valuation standpoint: “What we can say within the overall market level is that there is a huge range of valuations out there. For example, the staples area – especially non-pharmaceutical health care – looks expensive. But some of the cyclicals, including the banks, look attractive.”

Moss is a bottom-up investor. About 21% the BMO fund’s AUM is held in the U.K., 17% is in Germany, 16% is in Switzerland and 13% is in France, with smaller holdings in markets such as Ireland. Moss, who does not identify with either the value or growth style, looks for quality businesses that have management that is shareholder-friendly and are trading at attractive valuations.

One of the top holdings in the 48-name BMO fund’s portfolio is Amer Sports Oy, a Finland-based sporting-goods maker that produces well-known brands such as Salomon, Atomic, Wilson and Arc’teryx. Amer Sports, now under new management, has spent money on new product development and expansion of product lines. “We think [this firm] has many years of growth ahead of it,” says Moss.

Amer Sports stock is trading at about 27.40 euros ($38.85) a share (24.6 times trailing earnings). Moss believes that fair value is 30 euros a share.

The brexit talks may develop into a long, drawn-out process, and the tone of the talks will depend on how nuanced the politicians may be, says Peter Hadden, portfolio manager with Fidelity Institutional Asset Management (a unit of Boston-based FMR LLC) in Smithfield, R.I., who oversees Fidelity Europe Fund.

“Understand that the EU holds all the cards in the discussions. And the EU can extend the two-year window if [time] runs out, but the U.K. cannot,” says Hadden. “If both sides don’t agree after two years and the EU decides not to extend, the U.K. loses all the advantages of being an EU member.

“This will create uncertainty on the part of corporations and their ability to invest, which should have a dampening effect on growth going forward – on all sides,” he adds. “For example, if you run a Germany-owned auto plant, you may not expand in the U.K. because you don’t know what the trade regulations will be. What will you do with your plants? Will you move outside the U.K. because it can’t take parts from Germany, for example, without some taxes and tariffs? If you are a CEO, how do you plan, when you don’t know the rules for at least two years? You will slow down future investments.”

As for stock valuations, Hadden concurs that the market was a mixed bag before Brexit: “On a historical basis, U.K. homebuilders, for example, were a bit expensive, but banks were way undervalued. The gap between banks and large pharmaceuticals was wide. Today, the market is a tad expensive, but not overly so. There’s more selling out of staples and buying into financial services and some consumer discretionary firms.”

Hadden admits he is not a bull: “I’m a cautious optimist.” He notes that compared with the global financial crisis in 2008-09, when authorities rescued many banks, there’s far more confusion about the fallout from Brexit.

“We are hearing rhetoric in the EU: ‘We’re not going to give them a sweetheart deal because it will encourage others to do their own thing’,” he says. “I think [the negotiators] will reach a good deal for both sides, without much enticement for others. It will be a difficult tightrope to walk.”

Hadden is a growth-oriented, bottom-up investor. About 24.8% of the Fidelity fund’s AUM is held in the U.K., 20.2% is in France, 14.2% is in Germany and 8.5% is in Switzerland, with smaller holdings to markets such as Spain and Sweden. The fund holds 51 stocks.

Hadden likes names such as Lundin Petroleum AB, a Sweden-based mid-cap oil firm with operations in Norway and Southeast Asia. Lundin stock is trading at about SEK147.50 ($21.50) a share. There is no stated target.

© 2016 Investment Executive. All rights reserved.