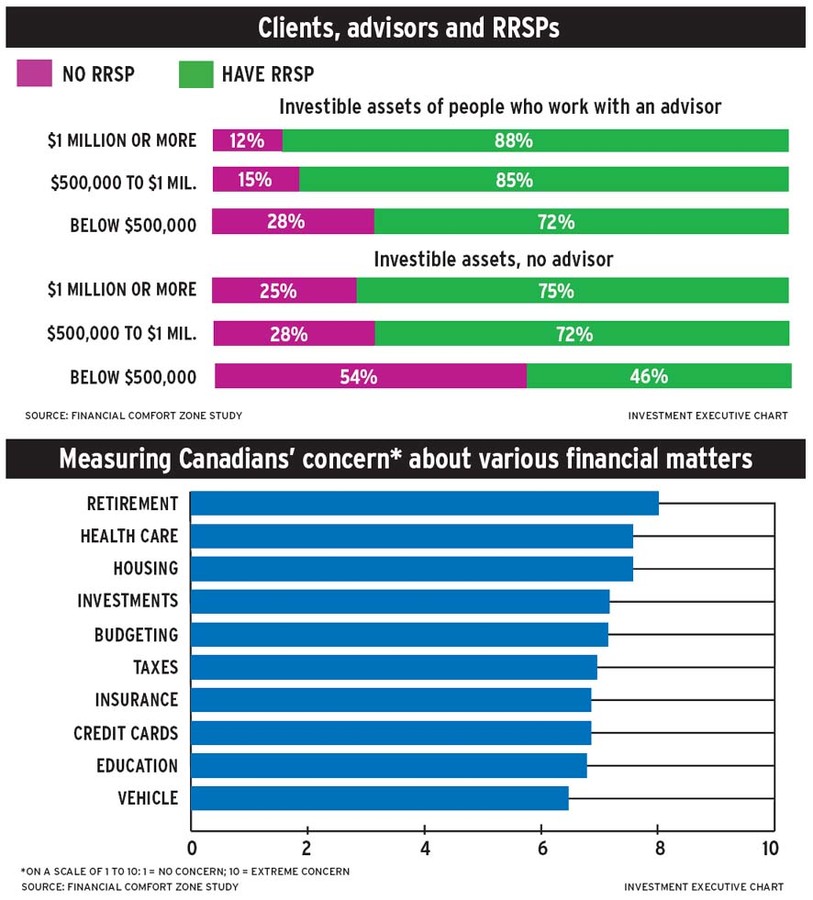

The average contribution to registered retirement savings plans (RRSP) in the 2013 tax year held steady from the previous year, according to a new poll released Tuesday by Bank of Montreal (BMO). However, many Canadians regret not being able to save more.

According to BMO’s fifth annual Post-RRSP Deadline Study, Canadians contributed an average of $3,518 by the 2013 deadline, which is virtually unchanged from last year’s $3,544. Of those respondents who made a contribution, 54% said they had contributed as much as they could. However, over one-third (35%) of respondents felt that they perhaps could have put a little more away in their RRSPs this past year.

“Their dollar is being pulled or stretched in various directions in terms of meeting their month-to-month expenses,” says Chris Buttigieg, senior manager, wealth planning strategy, BMO. “Advisors can certainly be of assistance to their clients in helping them contribute more or make the most out of their contributions.”

There are several ways advisors can help clients contribute to RRSPs without regret in 2014, according to Buttigieg. The first is by setting up a meeting in the next few months to review the clients’ retirement or financial plans. As well, advisors can help their clients set up a budget or spending plan to make sure they are contributing as much as they can – or wish – to their RRSPs. Finally, if the meeting happens after the April tax deadline, advisors should ask clients to bring in their notice of assessments.

“There’s a lot of important information [in the assessment] in terms of how much RRSP contribution room has been used or left unused over the years,” says Buttigieg, “and that could certainly be the launch point for setting that client on the right course [for their contributions].”

The report also found that most Canadians stick to what they know when it comes to investing in their RRSPs. Forty-nine per cent of respondents said they purchased mutual funds in their RRSPs. Guaranteed investment certificates were the second most popular choice for investors with 35% of respondents saying they purchased that product in their RRSPs in 2013.

These GICs are the “plain-Jane, vanilla” type, says Buttigieg, and while clients may find the guaranteed aspect of the product some may perhaps want or need a higher return. As such, Buttigieg suggest educating clients about other products, such as market-linked GICs.

Bonds and stocks were the next choice for investors at 18% and 17% respectively, while only 12% of respondents said they had purchased exchange-traded funds.