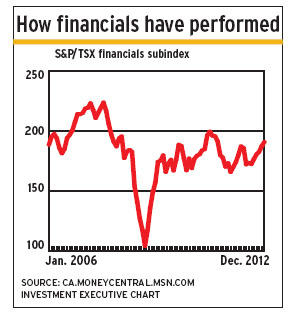

Canadian financial services firms are likely to have only modest growth in 2013, with the country’s big banks experiencing a slowdown in consumer lending and life insurers struggling with continued low interest rates and sluggish equities markets.

“It might be time for investors to take some money off the table,” says Shane Jones, chief investment officer with Toronto-based ScotiaMcLeod Inc. Although Canadian financials remain sound long-term investments, he adds, they are not likely to outperform other sectors in 2013.

Canada’s banks, insurers and other financial services firms will be trying to boost revenue in an economy that is expected to grow modestly Canada’s gross domestic product (GDP) should expand by 1.5%-2% in 2013 with the risk that the sovereign-debt crisis in Europe, the U.S.’s fiscal problems or economic sluggishness in China could pull growth down further.

“Canada has a bit more exposure to the pace of a Chinese recovery than the U.S. does in comparison,” says Stuart Kedwell, senior vice president and senior portfolio manager, Canadian equities, with RBC Global Asset Management Inc. in Toronto. Although China’s economy has been showing signs of recovery, any fallback is likely to dampen commodities prices and, therefore, the Canadian economy overall.

Meanwhile, Canada’s housing market will continue to soften in 2013, although most fund portfolio managers believe that there will be a gradual decline in home prices rather than the steep drop that characterized the collapse of the U.S. housing market during the financial crisis. Still, any decline in Canadian home prices, when coupled with the slowdown in consumer borrowing that appears to have already begun, will dampen bank earnings.

With GDP growth still slow, interest rates in Canada are likely to remain low in 2013, with most portfolio managers assuming that an increase is more likely to come in 2014 or even 2015. That means continued pressure on both the banks’ net interest margins, which are already relatively compressed, and life insurers, whose liabilities for long-term products are high when rates are low.

In general, portfolio managers are market-weighted in bank stocks and underweighted in life insurers and other financials.

Here’s a look at what’s expected in Canadian financial services, by subsector:

– BANKS. Fund portfolio managers believe that the banks may be hard pressed to achieve anything above modest growth in 2013 due to Canadian households de-leveraging, the housing market softening and the overall domestic economy facing several key risks, including the possibility of weaker commodities prices.

The banks hope that the slowing growth in their domestic personal and commercial business units will be offset, to some degree, by earnings generated by other business lines including wealth management, capital markets, international and ancillary businesses and by curtailing growth in expenses.

“Best-case scenarios for the banks could be hijacked,” says Richard Nield, portfolio manager with Invesco Canada Ltd. in Austin, Tex., “if there’s a big pullback in commodities prices, the housing market takes a bigger than expected turn south or the fixed-income and equities markets negatively affect the banks’ capital markets business.”

Nevertheless, portfolio managers expect banks to continue raising their dividends in 2013, although perhaps not by quite the same rate that they did in 2012.

“I don’t think the banks are going to go much higher on their payout ratios,” Kedwell says. “I think we’re going to get dividend growth in line with earnings growth.”

That’s why portfolio managers are, in general, market-weighted in the sector.

“From a longer-term perspective,” says Dom Grestoni, senior vice president and portfolio manager with I.G. Investment Management Ltd. in Winnipeg, “taking a four-plus percentage point yield from a bank stock is a decision for which you will be well rewarded. These are high-quality, dividend-oriented companies that will do well and benefit as long as the domestic economy is growing at even a modest level.”

Bank stocks can provide your clients with an attractive yield ranging roughly from 4%-4.5%, portfolio managers say, which compares favourably with returns that can be generated from bonds and other fixed-income products as long as your clients are willing to accept some short-term volatility in share prices.

Nor are Canadian banks in danger of becoming undercapitalized, a possible risk that haunts many U.S. and European banks. Indeed, portfolio managers agree that the Canadian banks appear to be well positioned to meet any new global or domestic banking regulatory requirements.

Among Canada’s big banks, portfolio managers prefer Toronto-Dominion Bank, which has built its strong U.S. retail franchise; Bank of Nova Scotia, which has positioned itself for growth through its international platform; and Royal Bank of Canada because of its wealth-management, capital markets and domestic retail banking businesses.

– INSURANCE. Even though share prices of the major Canadian life insurers rose in 2012, portfolio managers believe that this subsector will continue to struggle in 2013 because of stubbornly low interest rates and volatile and sluggish equities markets.

“[Insurers] need modest economic growth, they need stable to increasing interest rates and they need stable to increasing stock markets,” Grestoni says. “That will drive the recovery in the [sub]sector.”

Over the past several years, the major insurers have shifted out of certain businesses that have been underperforming, such as some variable-annuity product lines, and into businesses that provide the opportunity to produce more reliable earnings, such as wealth management.

“Overall, I think [insurers] are making better decisions,” Nield says. “If you’re losing money in a product line, you probably shouldn’t [under]write any more business.”

Portfolio managers feel that the insurers may be starting to phase out the process of taking reserves against future liabilities and adjusting their businesses, which may provide your clients with an opportunity to step in if they believe that economic conditions will start to move in the insurers’ favour. Says Kedwell: “There’s a lot of positive leverage in these stocks.”

Among the major life insurers, portfolio managers favour Great-West Lifeco Inc. (GWL), which has been shielded somewhat from the subsector’s overall difficulties by virtue of having a stronger book of underlying business; and Sun Life Financial Inc., which has made some key changes to its business mix.

Among the property and casualty insurers, portfolio managers consider Intact Financial Corp. a well-managed firm with a dominant position in its business and the proven ability to make sound acquisitions and integrate them.

– ASSET MANAGERS. Although portfolio managers believe there are some good names within the asset-management group, they remain concerned about this subsector’s long-term prospects in the context of strong competition from the big banks.

“Canadian banks have done a great job of dominating the asset flows of late,” Kedwell says. “It certainly has become more difficult for Canadian independents to do as well as they have in the past.”

On the other hand, portfolio managers acknowledge that there may be opportunities for your clients to achieve above-average returns if they believe economic conditions will be stronger than expected.

“If you think the market goes up [this] year,” Nield says, “you’ll get quite a bit more torque following some of these investments.”

One pick is Brookfield Asset Management Inc., an alternative global asset manager focusing on property, renewable power, infrastructure and private equity.

– STOCK EXCHANGES. Portfolio managers are sitting on the sidelines regarding TMX Group Ltd., which faces challenges in producing earnings, partly due to lower trading volumes.

– HOLDING COMPANIES. Power Financial Corp. is considered a well-managed firm and a good way to gain exposure to GWL.

© 2013 Investment Executive. All rights reserved.