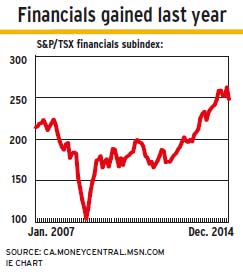

Canadian financial services firms are likely to see modest growth in net income in 2015, somewhat below the levels they enjoyed last year.

“Mid-single digit [earnings growth] is where the consensus is on the banks; slightly better for the life insurers,” says Stephen Carlin, vice president and senior portfolio manager of Canadian equities with CIBC Asset Management Inc. in Toronto.

Economic growth in Canada for this year is forecast to be 2%-2.5%: the lower end of that range is the more likely scenario if oil prices remain below US$70 a barrel over the year. One positive factor for growth will be higher exports to the growing U.S. economy.

Low prices for oil and other commodities, and the negative effect they might have on the domestic economy overall, remains the chief concern for 2015. Another risk would be any significant uptick in the unemployment rate, which was a relatively benign 6.6% in November. A spike in joblessness could lead to a rise in consumer-loan losses.

The Bank of Canada is expected to hold its line on interest rates this year, with the U.S. Federal Reserve Board possibly inching its rates higher in the second half of 2015.

“In Canada, it’s tough to envision rates actually going up,”says Richard Nield, portfolio manager with Invesco Canada Ltd., in Austin, Tex. “In the U.S., if growth rates continue, you might get a small rate hike.”

In general, investment funds are moderately underweighted in banks, moderately overweighted in the insurers and generally underweighted in other financial services. Here’s a look at the sector in more detail:

– Banks. Despite a few key possible headwinds, Canadian banks should continue to perform relatively well in 2015.

“The Canadian banks have diversified businesses that have found ways to grind out mid- to high single-digit earnings growth in a variety of conditions,” says Stuart Kedwell, senior vice president and senior portfolio manager, Canadian equities, with RBC Global Asset Management Inc. in Toronto.

Last year, the big banks all raised their dividends, and that dividend payout trend is likely to continue in 2015, if at a slower pace. “There’s scope for [stock] buybacks and modest dividend increases, but I think ‘modest’ is the word,” Nield says.

Some of the banks already may be at the high end of their dividend payout ratios, and therefore have no room for increases; other banks will want to make sure their capital levels are maintained.

“Bank of Nova Scotia has the highest [Common Equity Tier I] capital ratio, and might have the flexibility to do more [on dividends],” Nield says. “But the other big banks that are in the 9%-10% range probably still want to build up their capital a little bit.”

Lower energy prices probably will have a negative effect on Canada’s economy overall, and thus be a drag on bank earnings.

“It’s not so much where oil prices go, but how long they stay at a low level,” says Jennifer Radman, vice president and portfolio manager with Caldwell Investment Management Ltd. in Toronto. “Over the next quarter or two, you’ll get a better sense of the effect of low oil prices on the banks.”

Loans to the oil and gas sector comprise only about 2% of the banks’ loan books. However, the oil and gas sector also comprises almost 10% of the banks’ capital-markets business.

“That’s where low [energy] prices probably hurts [the banks] the most,” Nield says.

Commercial and industrial loan growth, apart from loans to the energy sector, is expected to remain buoyant. But consumer loan growth is likely to be sluggish this year.

With loan growth overall slowing, and net interest margins likely to remain flat, banks will be looking to focus strongly on keeping expenses in line in order to eke out mid-single-digit earnings growth in their domestic banking businesses. “It’s going to be a grind next year,” Kedwell says.

Ongoing compliance costs associated with the focus everywhere on banking regulations also may be an issue, Radman says. This is particularly true for banks with significant businesses in the U.S. (such as Royal Bank of Canada and Bank of Montreal) or internationally (such as Bank of Nova Scotia). “The whole regulatory environment has shifted,” she adds.

Among the big banks, portfolio managers continue to favour Royal Bank of Canada for its dominant position across a variety of businesses. “It still is best in class for the wholesale business versus the rest of the Canadian banks, and it has a very sound Canadian retail operation,” Nield says.

– Life insurers. Canadian lifecos appear to be better positioned for growth relative to the banks, both this year and beyond.

“[Canadian lifecos] have less exposure to a domestic slowdown, and they have strong businesses in wealth management,” Kedwell says. “The potential for earnings growth over the next two to five years looks pretty good relative to what’s available in the financial [services] sector.”

Long-term rates are not expected to rise significantly, which will not necessarily harm the lifecos.

“They’re all used to living in a low interest [rate] environment,” Nield says. “They’ve adapted and changed their product mix to lower their sensitivity to interest rates.”

The lifecos also have been increasing their capital levels, which will give these firms the flexibility to increase dividends this year.

The key risk in the coming year for the lifecos and their asset-management operations is a significant correction in equities markets. Among the lifecos, Manulife Financial Corp., which has set an ambitious growth target of $4 billion in earnings by 2016, is the most favoured. The firm’s business in Asia is seen as a growth area, and Manulife’s efforts to wring out efficiencies across its lines of business are beginning to bear fruit.

– Property and casualty insurers. Although investment fund portfolios generally are underweighted in the property and casualty insurance segment, Intact Financial Corp. is favoured. “It’s very well run,” Kedwell says.

Fairfax Financial Holdings Ltd. also is a favourite for its strong investment portfolio, which is hedged. “Fairfax is protected from any big equity hit,” explains Nield.

– Asset managers. This subsector raises concerns about how these firms will deal with new regulations affecting the investment industry. Among the names in this subsector, Brookfield Asset Management Inc. is preferred.

“It’s becoming more apparent that its pure asset-management business is adding a lot of value,” Nield says. “There’s good long-term upside there.”

CI Investments Inc. also is favoured. Says Kedwell: “[CI is] the best run of the independents.”

– Brokerages. Among the distributors, the short-term outlook for Canaccord Genuity Corp. and GMP Capital Inc. is not attractive, as the capital market business is expected to face turbulence this year.

However, those two companies may represent a good play for clients with a longer time horizon, as the firms’ respective valuations are low.

“In an account that can handle more volatility,” Kedwell says, “we think there’s an interesting setup in these stocks.”

© 2015 Investment Executive. All rights reserved.