Asia’s economies continue to grow at a world-beating pace, while also developing more stability and balance as their economies evolve from a focus on commodities production and basic manufacturing to more value-added industries to serve a wealthier base of consumers at home.

Economic growth rates have slowed from their peaks, but the region (excluding China) is forecast by the World Bank to grow at a pace of 5.3% in 2014. Domestic activity, particularly private consumption and investment, is becoming an increasingly important driver in most Asian countries. However, although the importance of exports is declining in some countries, trade still is a key driver in Taiwan and South Korea. These exporting countries, as well as China, remain vulnerable to the pace of global growth, particularly in Europe and the U.S.

Commodity prices have softened in the past year or so, especially for iron ore, palm oil, rubber and non-oil energy such as coal and gas. However, trade among Asian countries is increasing as the Association of Southeast Asian Nations moves toward a common market, creating a free flow of services, goods and labour.

“Infrastructure spending has come down in the region, and with that there has been some softening of commodity prices,” says Eileen Dibb, portfolio manager with Smithfield, R.I.-based Pyramis Global Advisors, a division of Boston-based FMR LLC (a.k.a. Fidelity Investments), who manages portfolios for Fidelity Far East Fund and Fidelity AsiaStar Fund. “Some countries, including Indonesia, Malaysia and Australia, are commodity producers and sensitive to price drops.”

A key factor affecting Asian countries in 2014 will be the degree to which the U.S. Federal Reserve Board decides to taper its quantitative easing (QE) program. Starting in January, it will buy $75 billion in government bonds per month, down from $85 billion a month since October 2012. Fed policy-makers say they are likely to continue to trim these purchases “in further measured steps at future meetings.”

The original talk of QE tapering last spring pushed up U.S. bond rates and thereby set off a massive outflow of capital from emerging markets as investors headed for the more attractive yields in those U.S. bonds. Since then, there has been some recovery in emerging-markets stocks, bonds and currencies, and reaction to the recent tapering announcement was muted in emerging markets.

“There has been some currency depreciation as a result of capital outflows since the tapering talk began,” says Chuk Wong, vice president of Bank of Nova Scotia-owned 1832 Asset Management LP in Toronto and portfolio manager of Dynamic Far East Value Fund. “But I think it has been overdone. Fundamentally, the region is healthy.”

Any impact on capital flows in Asia by tapering U.S. QE may be offset by Japan’s new stimulus measures to spur its economy. That could lead to more Japanese investment in the rest of the region and increased trade.

However, Norman Ho, investment director in Hong Kong of Asia Pacific Fund Ltd., a closed-end fund trading on the New York Stock Exchange, says he is wary of high-growth companies with external funding needs. He is focusing on companies that are able to generate sufficient cash flow for capital expenditures and dividend payments without resorting to leverage or new financings.

Here’s a look at a handful of Asia’s markets (with the exception of China, which is covered in a separate article on page B7):

– Indonesia. As a producer of palm oil, coal and gas, Indonesia benefits from trade with China and enjoys being in closer proximity to that giant market than fellow resources producer Australia. Indonesia has been hurt by lower commodity prices but is benefiting from rising consumer spending.

Mark Lin, vice president of international equities for CIBC Asset Management Inc. in Montreal and portfolio manager of CIBC Asia-Pacific Fund, favours Bank Rakyat Indonesia, which specializes in micro-financing and retail banking, and retail-oriented Bank Negara Indonesia. Lin is avoiding banks with exposure to capital markets.

Next: The Phillippines

@page_break@

– The Philippines. While this country has been devastated by typhoon Haiyan, the Philippines remains an attractive emerging market with an expected annual economic growth rate of about 7%. The country is a major recipient of remittances from a large group of people who work overseas but financially support their families at home. The country has a young population and English is widely spoken, spurring growth in the call-centre business.

“The natural disaster in the Philippines is tragic,” Wong says. “But these disasters can often be drivers of growth when reconstruction gets underway.”

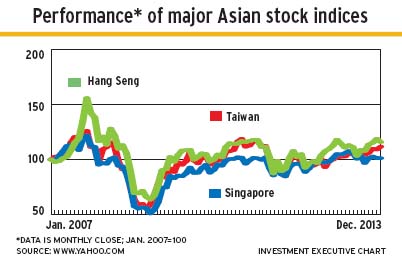

– South Korea. One of the more developed Asian markets, South Korea is a leader in electronics and automobile production. Many investment funds hold positions in this country’s recognized global brands, Samsung Electronics Co. Ltd. and Hyundai Mobis Co. Ltd.

– Taiwan. Taiwan is a big exporter of components for the technology sector, producing parts for smartphones, tablets and computers made by global leaders.

Dibb likes Taiwan Semiconductor Manufacturing Co. Ltd. Wong prefers Chailease Holding Co. Ltd., which leases industrial equipment to businesses.

– Hong Kong. Hong Kong continues to boom due to its proximity to China but most portfolio managers are focusing on companies that are doing business throughout Asia.

For example, Dibb and Tim Leung, vice president and head of Asian equities in Hong Kong with Winnipeg-based Investors Group Inc. and portfolio manager of Investors Pacific International Fund and Investors Greater China Fund, both favour insurance company AIA Group Ltd. Both portfolio managers also like Hutchison Whampoa Ltd., a multi-pronged retail, container-port and real estate empire.

Laurence Bensafi, deputy head of global emerging markets with RBC Global Asset Management Inc. in London, and portfolio manager of RBC Emerging Markets Dividend Fund, invests in Luk Fook Holdings International Ltd., a giant, prosperous jewelry-store chain based in Hong Kong with sales throughout the world.

– India. After struggling through a difficult year in 2013, some of the economic clouds are expected to lift for India in 2014 with anticipated growth at a comfortable level of around 5% this year.

Inflation of 7% per year remains a key concern. India’s government has been trying to control inflation by keeping interest rates high and controlling spending, but this policy has slowed previously hot economic growth. India also faces political uncertainty with a national election expected in the spring. The rupee has been one of the worst-performing currencies in Asia in the past year, dropping by almost 25% between January and September 2013 before regaining about half of those losses.

In December, India’s ruling Congress Party suffered a major blow in elections in four key states comprising 15% of the population. The party is losing votes to the Bharatiya Janata Party, and a fierce battle is shaping up between a fired-up Opposition and the Congress Party, which has governed India for almost a decade.

Mihir Vora, chief investment officer with Birla Sun Life Asset Management Co. Ltd. in Mumbai and portfolio manager of Excel India Fund, sponsored by Excel Funds Management Inc. of Mississauga, Ont., expects an easing of inflation and interest rates in 2014. He prefers banks, which tend to do well when interest rates are easing, and the Excel fund invests in ICICI Bank Ltd. and HDFC Bank Ltd.

Other major holdings in the Excel fund include pharmaceuticals (Sun Pharmaceutical Industries Ltd., Lupin Pharmaceuticals Inc. and Dr. Reddy’s Laboratories Ltd.). As well, the relatively weak rupee attracts business in information technology services from outsourcers in other countries, benefiting holdings such as Infosys Technologies Ltd. and Tata Consultancy Services Ltd.

Like Vora, Bensafi is positive on the consumer discretionary sector and favours the automobile and motorcycle industry, including Bajaj Auto Ltd., a major producer of motorbikes.

© 2014 Investment Executive. All rights reserved.