Canada’s financial services sector is in the midst of adapting to significant changes, including the rise of robo-advisors and the growing regulatory complexities of working with an aging clientele, according to the results of Investment Executive‘s 2016 Report Card series. Advisors are thinking carefully about the support they need from their firms to meet these new realities.

“It’s a matter of keeping up. In our industry, people leapfrog. You could be the worst at online access, then you leapfrog everyone and become the best,” says an advisor in Ontario with Montreal-based National Bank Financial Ltd. “It’s just a matter of keeping up and not falling behind.”

Yet, leapfrogging to meet the challenges of the future could be difficult for many advisors, given the fact they’re not getting any younger. Case in point: the average age of advisors remains stable, at just shy of 50 years of age, compared with years past. Similarly, the average tenure of an advisor with a firm and in the industry remains in step with 2015 results, suggesting that the sector needs to inject a little “young blood” into the advisors’ rank and file.

Recruiting younger advisors is easier said than done, however, particularly through succession plans. Advisors noted that some firms are trying to bring younger advisors on board through formal succession planning programs, but those advisors still are concerned about the difficult challenge of finding the right successor. (See Facing a need for fresh blood.)

“The biggest issue is finding the right advisor fit. Having the right guy who will do what you need for your clients – that’s a whole different question,” says an advisor in Ontario with Mississauga, Ont.-based Investment Planning Counsel Inc.

The difficulties that rookie advisors face in getting started in this business is well known, and adding to that challenge is the fact that future advisors will be working in a very different environment than the one advisors work in today.

For example, technology is quickly disrupting the financial services sector, particularly with the launch of digital asset-allocation services, known as robo-advisors.

To that end, advisors were asked in a supplementary question in this year’s surveys whether they consider these financial technology startups a threat to their business. Although some advisors noted that these online services could be a concern for future generations, the overwhelming majority of advisors said they don’t view robo-advisors that way.

Indeed, 81.5% of all advisors surveyed said they don’t consider these startups to be a threat because those advisors believe clients value face-to-face relationships. Some advisors even went so far as to say that robo-advisors could prove to be a boon for the advisor’s business. (See Are robo-advisors a threat?)

“I think it’s great for our industry; they may enhance and elevate what we do. I would even use [a robo-advisor service] in my own practice,” says an advisor in Ontario with Toronto-based Raymond James Ltd. “If we can get more of the day-to-day allocation standardized, that would free up my time to spend more of it with clients.”

Advisors also are looking to modernize their practices through other innovations in technology. More specifically, the ability to take their business on the road or communicate with clients and prospects via social media are both becoming increasingly important to advisors.

Although most financial services firms have a way to go to support all the needs of the “mobile advisor,” they’re certainly moving in that direction. (See Newer technology’s increasing importance.)

“Previously, unless you had a BlackBerry, you couldn’t use mobile tech at all,” says an advisor in Ontario with Toronto-based TD Wealth Private Investment Advice. “Now, we have a new app coming out that’s even better. [The tech department] has focused on that and we’re appreciative.”

As advisors adapt to new ways of doing business, the services they provide also are evolving. For example, the results of this year’s Report Card series show that advisors and their firms are placing more emphasis on financial planning: the percentage of advisors who create financial plans for clients increased to 86.2% this year from 81.8% in 2015. (See Attention turns to financial planning.)

“This is the direction the industry is going,” says an advisor in British Columbia with Toronto-based RBC Dominion Securities Inc. “If we’re going to charge fees, people need some service around that.”

Part of that emphasis on fees is a result of the implementation of the second phase of the client relationship model (CRM2), which mandates enhanced cost disclosure and portfolio performance reporting. CRM2 is a major reason advisors are looking to show the value they provide to their clients.

This years-long endeavour is just one of several compliance changes that have taken place since the 2008-09 global financial crisis. As the number of regulatory requirements has grown, advisors have developed a growing appreciation for their compliance officers and consider them as a help rather than a hindrance to conducting business. (See The challenge of compliance.)

“[Compliance staff] give presentations on compliance and dealing with seniors,” says an advisor in Alberta with Toronto-based Richardson GMP Ltd. “They’re keen and helping us protect our firm and our business by pointing out the landmines.”

Navigating through the regulatory issues that surround working with the elderly is something that will increase in importance. This demographic is growing in Canada and regulators are increasing their focus on seniors’ issues, which means firms must develop new procedures that allow advisors to serve these clients without running afoul of the regulators.

To that end, advisors were asked in another supplementary question how prepared they believe their firm is to deal with the unique issues related to senior clients. The overwhelming response was that advisors and their firms are ready. Whether offering products geared toward retired clients or providing training to recognize the signs of elder abuse, advisors said they’re well prepared to deal with their aging client base. (See Seniors’ issues take centre stage.)

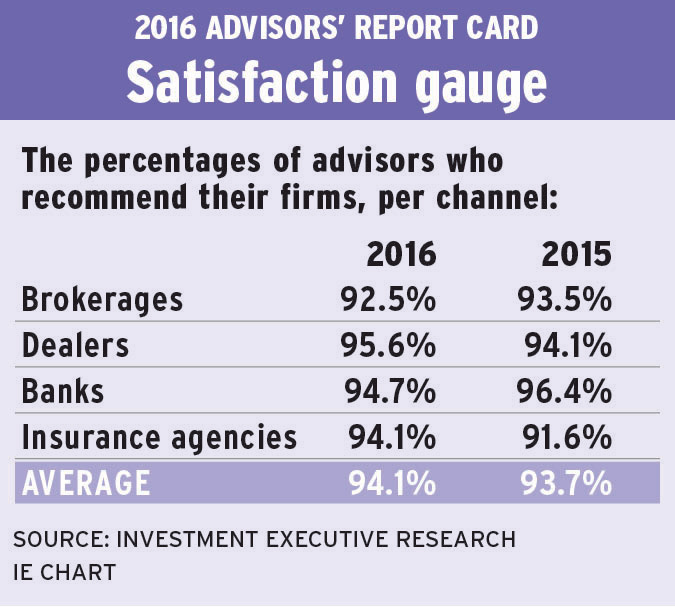

Although clients and the financial services sector find themselves in a period of rapid change, advisors’ opinions on what matters most to them remains steadfast. As in previous years, the top three categories in importance to advisors remain “firm’s ethics,” “firm’s stability” and “freedom to make objective product choices.”

In fact, how well a firm meets advisors’ expectations regarding their ability to make independent product choices can affect the company’s overall ratings in a Report Card. There’s a strong correlation between a firm garnering a high rating in that category and in “firm’s strategic focus” with the firm’s ” rating” and its “overall rating by advisors.”

This correlation suggests that advisors’ satisfaction with their firm typically is highest when they’re clear about their firms’ priorities and feel free to recommend products that they feel are best suited to their clients.

“[My firm] gives you the freedom, space and tools to succeed,” says an advisor in British Columbia with Kitchener, Ont.-based Financial Horizons Inc.

© 2016 Investment Executive. All rights reserved.