Buoyed by an improving economy, U.S. equities markets have been climbing steadily since the Great Recession of 2009, although the momentum has slowed year to date – the benchmark S&P 500 composite index is up by a mere 2%. Still, fund portfolio managers are bullish on prospects for U.S. equities and favour stocks that have more predictable earnings and are less sensitive to economic cycles.

“I’m not surprised to see U.S. equities treading water, given the very strong results that we’ve seen over the past few years,” says Jason Hornett, vice president with Calgary-based Franklin Bissett Investment Management Ltd. and co-manager of Franklin Bissett U.S. Focus Corporate Class Fund. Hornett shares portfolio-management duties with Garey Aitken, chief investment officer with Franklin Bissett.

“If you look back on a six-year time period,” says Hornett, “you’ve been receiving close to 20% returns annually from the S&P 500. In this environment, over the past six months, U.S. equities were the beneficiaries of a strengthening U.S. dollar and that effect has stopped for now.

“And there are some concerns,” he adds. “Will the recovery continue? Or are things going to start slowing down? In that case, earnings estimates could be too high, and we’d have to see them come down. That’s probably why we’re in a holding pattern.”

However, if earnings remain strong and no major problems emerge, then Hornett would not be surprised if equities go higher: “The first-quarter results looked a bit softer than expected, and some economists blamed it on the poor weather. But I’m optimistic and pretty enthusiastic about the employment market continuing to improve. We haven’t had a lot of growth in wages, but it’s starting to get a little bit better.”

Among various positive developments, Hornett notes that Wal-Mart Stores Inc. announced it would raise its minimum wage, providing impetus to wage growth. Also, lower gasoline prices act like a tax cut.

“I’m probably more optimistic than the doomsayers, who have concerns that economic growth will start to stall,” Hornett says.

As for price/earnings multiples, U.S. stocks are trading, on average, at about 17 times earnings, which has changed little in the past six months.

“But equities are trading at the high end of their historical range, which is not too surprising, given the extremely low interest rate environment we’re in,” Hornett says. “And dividend yields are very attractive compared with bonds. Investors looking for income continue to be attracted to equities.”

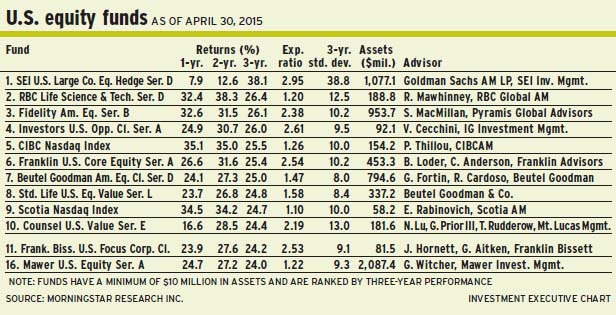

Running a portfolio with about 40 names, Hornett has allocated about 27.4% of Franklin Bissett fund’s assets under management (AUM) to health care, 16.9% to financials, 14.7% to consumer staples, 11.7% to information technology (IT) and smaller amounts to sectors such as energy.

A quantitative-based investor who seeks stocks with reasonable multiples and good profitability, Hornett likes firms such as Union Pacific Corp., a leading railway.

“It has a market-like valuation and looks very attractive from a risk level,” says Hornett, noting that the stock trades at about 19 times earnings. “[Union Pacific] has better earnings growth than the index and a much lower beta.”

Union Pacific stock is trading at about US$111.50 ($130.20) a share and pays a 2.2% dividend. There is no stated target.

Equally bullish is Steve MacMillan, a portfolio manager with Pyramis Global Advisors, a division of Boston-based FMR LLC (a.k.a. Fidelity Investments), who oversees Fidelity American Equity Fund.

“I meet [with the managements of] about 500 companies a year. And when I listen to CEOs and CFOs, I’m not hearing anything about a slowing U.S. economy,” MacMillan says. “Generally, there continues to be talk of recovery and a modest expansion. Lower energy and commodities prices are a net positive for the U.S. consumer. The U.S. economy remains on solid footing.”

MacMillan concurs with Hornett that stocks are trading slightly above their long-term historical averages. “But you also have to take into consideration,” he says, “that interest rates are well below the historical average. Any investor has a choice to allocate capital. If you are a German investor and your choices are 0% yield on government bonds or 17 times on the S&P 500, you’ll probably take the latter. Put in context with interest rates, I don’t think valuations are excessive. Low interest rates provide support.”

Although a hike in interest rates by the U.S. Federal Reserve Board is likely later this year, that move is already priced into the market, MacMillan says: “No one will be surprised if the Fed raises rates by 25 basis points in the fall. It will be more about the Fed’s ‘tone’ -how high and how aggressively rates will rise down the road.”

Besides, MacMillan adds, a rate increase signals that the U.S. economy is gaining traction: “If we are still here, four years from now, and rates were still zero, I’d be a lot more concerned. If rates are normalizing, that means we’re in a stronger place.”

A bottom-up investor who looks at stocks with a three- to five-year horizon, MacMillan favours companies that he describes as “capital-light” – firms that don’t require heavy capital investment and that benefit from strong, recurring earnings regardless of the state of the economy.

As a result, there is emphasis on health-care firms in the Fidelity fund – 24% of the fund’s AUM is in health care, 17.7% is in financials (but no banks), 16.2% is in consumer discretionary and 14.6% is in IT, with smaller holdings in sectors such as consumer staples and utilities.

“I’ll never find a capital-light, non-cyclical energy business with a competitive advantage,” says MacMillan. “They don’t exist.”

The 40-name Fidelity fund is fully invested. MacMillan likes Kroger Co., the largest supermarket chain in the U.S.

Like other companies in the food retailing industry, Kroger has experienced falling margins since Wal-Mart began selling groceries about 20 years ago. Yet, Kroger has adapted and reduced its costs.

“[Kroger has] the economies of scale that few competitors have to compete with Wal-Mart. [Kroger offers] better service, locations and a better shopping experience than Wal-Mart,” MacMillan says.

Kroger stock is trading at US$71.65 ($89.25) a share, or at 20.5 times earnings, and pays a 1% dividend. There is no stated target.

Another favourite is Cigna Corp., a leading health-care insurance administrator. “[Cigna is] unique because [it doesn’t] take the insurance risk for running health-care plans. The employers do,” says MacMillan.

Cigna stock is trading at about US$130.30 ($153.75) a share, or about 17 times earnings.

The slowdown is part of a classic market cycle, says Grayson Witcher, vice president with Calgary-based Mawer Investment Management Ltd. and portfolio manager of Mawer U.S. Equity Fund.

“The market is up around 200% from the bottom, which is pretty significant. People are reflecting on the strong performance and wondering, ‘Can it continue?’,” says Witcher, adding that some investors are scouring other markets in which valuations are lower.

The U.S. economy is doing well, argues Witcher: “If you listen to what the Fed has to say, there’s talk of less monetary easing and increasing the Fed funds rate. To me, that’s a sign that the economy is getting better. They would not be talking of raising rates if they thought the economy was getting worse or stagnating. There are signs that things are moving in the right direction.”

From a valuation perspective, Witcher notes, stocks are trading slightly above the long-term average. “But we have to keep in mind that we are still within one standard deviation of the historical mean,” says Witcher. “When it’s fairly close [to the historical mean], we are in the realm of reasonability.

“And things can stay expensive for a fairly long time,” he adds. “It doesn’t mean the market will correct tomorrow. You just have to be aware of the fact that just because the price/earnings ratio is a little above the historical average, it won’t revert to the mean tomorrow, or in the next quarter. But it could happen 10 years from now.”

A bottom-up stock-picker, Witcher has allocated about 22% of the Mawer fund’s AUM to IT, 19% to financials, 13% to consumer discretionary, 11% to health care and 10% to industrials, with smaller amounts to sectors such as energy.

“We’re not making a top-down bet on technology,” Witcher says. “But think of Silicon Valley and its critical mass. When you compare the U.S. to other regions, [Silicon Valley] has a competitive advantage – and it’s probably sustainable.”

One favourite in a 53-name portfolio is Fair Isaac Corp., a leading provider of credit scores to banks and mortgage firms. Although Fair Isaac stock has had a solid run since Witcher acquired shares in the firm for the Mawer fund in mid-2014, he sees more upside: “It’s a steady, boring business and very profitable. Others have tried to break into the credit-scoring market and have outright failed because Fair Isaac is so entrenched with the banks.”

Fair Isaac stock is trading at about US$92.30 ($108.90) a share, or 34 times trailing earnings. “[The share price] is at a premium to the market, but we believe it’s warranted, given the quality of its business.” There is no stated target.

© 2015 Investment Executive. All rights reserved.