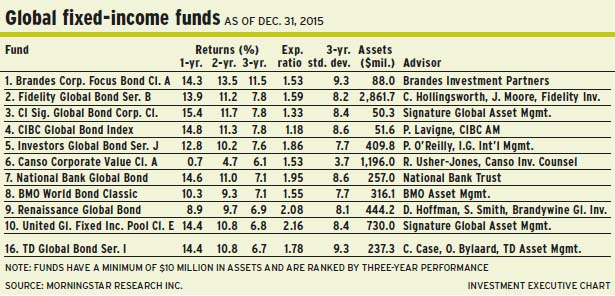

Global fixed-income markets proved highly challenging in 2015. Bond yields remained very low and volatile currency movements either boosted or hurt Canadian investment returns. Fund portfolio managers are cautious about the outlook, given that the U.S. Federal Reserve Board recently increased its overnight rate and currencies could continue on their rocky ride.

“We’re bottom-up managers who focus on individual security selection. But it’s safe to say that the Fed’s move is priced into the market,” says Richard Usher-Jones, partner and vice president at Richmond Hill, Ont.-based Canso Investment Counsel Ltd., and portfolio manager of Canso Corporate Value Fund. “Will other central banks follow suit? Time will tell. As far as Canada is concerned, raising rates in the U.S. will put a lot of pressure on different parts of our market. The question is: ‘How can you justify Canadian bond yields being lower than in the U.S.?’ That’s where we are today.”

Canada’s weak economy is in marked contrast to the U.S. economy, which is on a sounder footing and less reliant on commodities, the values of which have fallen substantially.

“Rates could stay low for an extended period,” says Usher-Jones, who tends to focus on North American bond markets, vs other regions. “But if we adjust to a more normal relationship between Canada and the U.S., we could see a rude awakening, as the Bank of Canada controls only the short end of the yield curve.”

He notes that Canadian bond yields now are negative once inflation is accounted for: “You’re supposed to make a real return on a risk-free asset over and above inflation. But real yields are negative. Something has to give.”

Usher-Jones is being defensive from an interest-rate perspective and maintains an average duration of 2.3 years in the Canso fund, vs six years for the benchmark FTSE TMX Canada all corporate bond index and 7.3 years for the FTSE TMX Canada universe bond index. About 50% of Canso fund’s assets under management (AUM) is in high-yield bonds; the remainder is in investment-grade bonds. The remaining 65% of AUM is in Canadian corporate bonds.

“We’ve assembled a portfolio with some good opportunities that give us some yield,” says Usher-Jones. “The other half of the portfolio is in very high-quality, shorter-duration positions that will give us the flexibility to sell them down and take advantage of opportunities should there be a dislocation in the market.”

About 35% of the Canso fund’s AUM is in foreign bonds denominated in either U.S. dollars (US$) or Canadian dollars (C$), including 20% of AUM in so-called “Maple” bonds (issued by foreign corporations in C$). “There’s good value in some Maples and foreign issuers,” he says. “But we’re able to find some better value at home.”

From a currency viewpoint, 70% of AUM is in C$ and 30% in US$ (half hedged back to the C$).

The Fed’s decision to raise its overnight rate could be a mistake and spell trouble for the global economy, argues Kamyar Hazaveh, vice president, fixed income, at Toronto-based Signature Global Asset Management (a unit of CI Investments Inc.) and portfolio co-manager of CI Signature Global Bond Class Fund. Hazaveh shares portfolio-management duties with John Shaw and Matthew Strauss, both vice presidents with Signature.

This will be a year of slowing U.S. and global economies, says Hazaveh: “Recession is not in our forecast. But, relative to the prior four to five years, when the U.S. economy was running at 4% nominal growth, 2016 will see much slower real and nominal growth.”

In Hazaveh’s view, the Fed has clearly mistimed its move to raise rates and should have taken action when the U.S. economy topped out in late 2014. “[The Fed] has raised rates at the worst possible time – the U.S. is slowing and forecast to slow, and the global economy is very weak,” he says. In fact, he notes, every central bank outside the U.S. is easing monetary policy. “The Fed’s action,” he adds, “raises the risk of an accident in the global economy as the U.S. dollar appreciates further and front-end interest rates are going higher.”

In short, the rate hike came about because the Fed was at risk of losing its credibility, Hazaveh believes. “But that was not reason enough to change monetary policy in an economy as large as the U.S.,” he says. “It’s possible that [the Fed] will get away with its decision. But the risks to the [global] economy have increased substantially as a result of the rate hike,” says Hazaveh, adding that deflation also is a risk.

Tactically, Hazaveh is being defensive, especially at the short end of the yield curve: “[The CI fund holds] nothing below five years – because it’s at risk of losing money. But we do own seven-year, 10-year and 30-year U.S. treasuries. Those bonds will perform really well as the Fed continues on this misguided tightening cycle and brings the U.S. and global economy to its knees.”

The CI fund holds about 95 securities from about 20 issuers. About 40% of AUM is in U.S. treasuries, followed by 22% in European sovereign bonds (mainly from Germany, France, Spain and Italy) and 20% in Japan. There also is about 8% in global investment-grade corporate bonds.

From a currency perspective, 43% of the CI fund’s AUM is in US$, 25% is in euros, 20% is in yen and the remaining 12% is in a mix of Swedish kroner, C$, Australian dollars, and pound sterling.

The CI fund’s average duration is about one-third of a year longer than the 7.3 years for the benchmark JPMorgan global government bond total return index (unhedged). “This duration comes from our macro view,” Hazaveh explains. “This is not an environment in which global rates will rise substantially. If we are right in our prognosis of a Fed policy mistake, then duration is cheap, actually. It’s not costing us much to go a bit longer.”

It’s not the start date of the Fed’s interest rate hike that matters, but the path of future interest rate increases, says Chris Case, vice president at Toronto-based TD Asset Management Inc. (TDAM), and portfolio co-manager of TD Global Bond Fund. He shares portfolio-management duties with Olga Bylaard, managing director of TDAM.

“We believe the Fed will follow a ‘low and slow’ path. This will be the loosest Fed tightening on record,” says Case. “Interest rates will remain low and growth will be relatively slow for a prolonged period. This situation is due to the massive debt that’s been piled onto government, corporate and household balance sheets.”

The Fed understands that the global economy cannot withstand monetary shocks and, although the central bank may boost rates again in 2016, Case says, “We do not foresee this leading to a dramatic rise in bond yields. Monetary policy will be well communicated by the Fed, and further rate movements will be modest and measured.”

Investing outside Canada offers opportunities to pick up extra yield, says Case, pointing to countries such as New Zealand and Australia. For example, 10-year Australian government bonds yield 2.85%, vs 1.45% for comparable Government of Canada bonds. “Australia and New Zealand are not in a position to raise rates any time soon,” he says. “At the very worst, they will be on hold, and may have another rate cut in them.”

Conversely, Case has a dim view of Japan because of its high debt/gross domestic product ratio. The TD fund has no exposure to Japan. As for the eurozone, Case is cautious, as the region is plagued by large structural issues that are very difficult to resolve.

The fund has about 200 holdings from 120 issuers. Based on fundamental analysis, Case and Bylaard have allocated the portion that might have gone into Japan – which accounts for almost 25% of the benchmark Citigroup world government bond index (C$) – to North American investment-grade corporate bonds, which comprise about 25% of the TD fund’s AUM. Similarly, because the two managers have a dim view of the eurozone, that region accounts for only 10% of AUM (in contrast to the index’s 30%).

About 15% of the TD fund’s AUM is in North American high-yield bonds, 25% in U.S. sovereign bonds and 25% in a mix of sovereigns from Australia, New Zealand and Canada.

The average duration for the TD fund is 6.8 years, vs 7.1 years for the benchmark, and the fund holds 40% in US$, 27% in euros, 10% in pounds sterling, with the rest in a mix of developed markets’ currencies.

Although 2015 offered double-digit returns, Case expects 3%-4% in 2016.

© 2016 Investment Executive. All rights reserved.