Mutual fund companies are the most visible part of the asset-management sector. However, they also are facing the greatest challenges. This is particularly so for the independents, which face stiff competition from the banks and higher redemptions as a result of the fee disclosure requirements coming into effect under the second phase of the client relationship model (CRM2).

The earnings outlook is better for the institutional and high net-worth (HNW) businesses. These clients focus on medium- and longer-term performance rather than on quarterly statements, as is more often the case for retail investors. As a result, HNW and institutional businesses’ assets are “stickier” and these firms tend to suffer fewer redemptions.

However, the two segments have very different business models. Institutional money management is a low fee/high volume business. The key is economies of scale. Once a firm reaches a large enough quantity of assets under management (AUM), revenue from additional AUM pretty much drops straight to the bottom line.

In contrast, the HNW business not only charges high management fees, but also performance fees when returns reach or exceed a specified level. What’s critical here is a high level of service and having strong relationships with clients. Much time and energy are spent on attracting prospects and retaining them.

Two of these asset managers worth considering are Fiera Capital Corp. of Montreal and Gluskin Sheff + Associates Inc. of Toronto.

Fiera aims to become a major institutional investment player and has been growing fast, mainly through acquisitions. Fiera’s AUM reached $90 billion as of June 30, up from $23 billion in 2010. The firm is aiming for $220 billion in AUM by 2020.

Fiera also has both retail and HNW businesses, giving the firm nice diversity in revenue streams.

Gluskin Sheff is an “ultra” HNW business: the minimum for client assets is $3 million. The firm focuses on providing strong, risk-adjusted returns. Fees are high and there are very lucrative performance fees when returns exceed specified levels. Gluskin Sheff has some institutional business, but that isn’t a focus. Rather, these assets are mainly endowments whose assets Gluskin Sheff has been asked to manage.

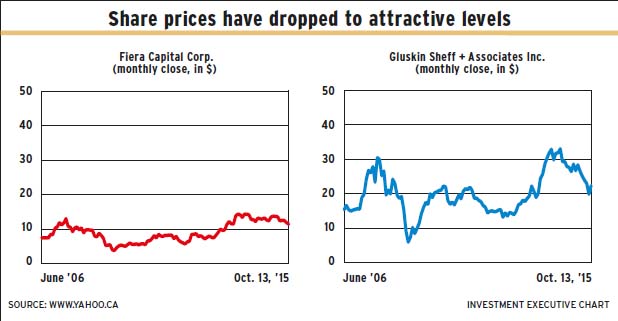

The share prices for the stocks of these two companies have dropped to attractive levels; some analysts – specifically, Scott Chan at Canaccord Genuity Corp. and Shubba Khan at National Bank Financial Ltd. (both analysts are located in Toronto) – think the shares are hitting bottom and are likely to move upward in the next year. Both Chan, and Khan have “buy” ratings on both firms’ stocks.

Here’s a look at the two companies in more detail:

– FIERA CAPITAL CORP. is the brainchild of Jean-Guy Desjardins, a highly respected portfolio manager and strategist. Fiera is his second major business venture. The first was TAL Global Asset Management Inc., established in 1972 and sold to Canadian Imperial Bank of Commerce in 2001, when TAL had $55 million in AUM.

Desjardins started Fiera in 2003 and acquisitions came quickly. Senegal Investment Counsel Inc. was bought in 2005; YMG Capital Management Inc., in 2006; and Sceptre Investment Counsel Ltd., in 2010. (All were Toronto-based companies.) Then came the big one in 2012 – Montreal-based NatCan Investment Management Inc., National Bank of Canada’s asset-management arm, with $25 billion in AUM. Fixed-income specialist Samson Capital Advisors LLC of New York was a smaller purchase made last February.

Although institutional money management is Fiera’s main business, the firm also has HNW operations to which it has been adding, including the 2013 purchase of Bel Air Investment Advisors LLC of Los Angeles and Wilkinson O’Grady & Co. Inc. of New York in 2013.

Integration of all these purchases have gone smoothly. This is probably partly because Fiera allows acquired investment-management teams to operate fairly independently, says Khan.

Fiera expects to make another $30 billion worth of acquisitions in the coming years, most likely U.S.-based HNW firms or investment managers. The latter strategy would extend Fiera’s expertise into areas such as emerging markets and alternative investments. The rest of the increase in the firm’s AUM will be a result of organic growth.

Fiera has about 55% of its AUM in institutional business, 15% in high net worth and 30% in retail. Chan doesn’t think those proportions are likely to change much.

On the retail side, Fiera is a mutual fund subadvisor for Desjardins Group. As part of the NatCan purchase, National Bank not only distributes Fiera products, but is committed to retaining Fiera as the manager of at least 40% of National Bank’s AUM for at least seven years.

The trick for Fiera is to increase its penetration of the financial advisor network, Chan says.

Khan agrees and sees potential for more retail sales through National Bank, given the bank’s 2011 acquisition of Vancouver-based HSBC Securities (Canada) Inc.’s retail brokerage arm and Winnipeg-based Wellington West Holdings Inc. National Bank owns about 22% of Fiera and can nominate two individuals to Fiera’s board of directors.

Khan’s thesis is that Fiera “remains well positioned to drive superior growth, given its access to bank-owned distribution, its U.S. platform, solid fund performance and additional acquisitions. Moreover, we expect comparatively robust investment returns, as [Fiera] has a significantly higher mix of fixed-income funds, which have benefited from the ‘flight to safety’ trade.”

Fiera has been trading at a 20% discount to its historical average share price, Chan notes. He thinks the 14% increase in earnings per share that he anticipates in 2016 could narrow the discount.

Chan has a one-year price target of $16.50 a share, while Khan’s is $15. The 70.2 million outstanding shares closed at $11.50 on Oct. 13.

Fiera has raised its quarterly dividend four times in the past year and a half – to 14¢ from 10¢ in total. The dividend yield was 4.9% on Oct. 9. Chan expects the company to continue raising its dividend every other quarter.

Excluding restructuring charges, Fiera’s net income for the year ended June 30 was $28.4 million on revenue of $240.7 million. Those figures were up from net income of $24.4 million on revenue of $196 million for the corresponding period a year earlier.

– GLUSKIN SHEFF + ASSOCIATES INC. was very successful in 2011-14, but sales have been flat in the past year, says Chan. He thinks this may be because of extreme market volatility, which may have caused a lot of people to pull their assets out of the market. Chan is confident, though, that the firm will do better in the next year.

Gluskin Sheff’s clients are mainly Canadian, although the firm has clients in the U.S. and could get more when Canadian equities, currently out of favour because of the drop in oil prices, become more attractive.

Khan notes that Gluskin Sheff’s chief economist is David Rosenberg, formerly chief North American economist with Bank of America Merrill Lynch in New York, who has a U.S. following.

Gluskin Sheff doesn’t have mass distribution for its investment funds. The firm gets most of its new clients through referrals and word of mouth, and spends a lot of time talking to prospects.

The firm is not an acquisitor, but will buy if a company that broadens Gluskin Sheff’s investment-management expertise is found – such as Toronto-based fixed-income specialist Blair Franklin Asset Management Holdings Inc., purchased in August 2014.

Gluskin Sheff was established in 1984 by investment gurus Ira Gluskin and Gerald Sheff. Gluskin was the firm’s chief investment officer (CIO) until the end of 2009; Sheff was CEO and chairman until Dec. 31, 2013.

The transition to new management was relatively easy on the CEO side, with Jeremy Freedman, who had been at the firm since 2000, now president and CEO.

The question mark is on the investment side. The reputation and investment performance Gluskin delivered was critical to the firm’s success. However, clients accepted the transition to Bill Webb, who worked with Gluskin since 1995, as CIO.

But there have been more exits this year. Strategist Tony Solomon left in the first quarter and Webb announced in mid-July that he will retire at the end of this year. So, now there will be more transitions – this time, to newcomers.

As of Jan. 1, 2016, Gluskin Sheff will have co-CIOs: Peter Mann, specializing in equities; and Peter Zaltz, a fixed-income expert. Mann came aboard in 2011; Zaltz joined in August 2014, when Gluskin Sheff acquired Blair Franklin, for which Zaltz had been CIO.

Chan and Khan both expect the new duo to deliver good performance and anticipate positive net sales in 2016. “Both [Mann and Zaltz] have good track records and can complement each other,” says Chan.

The new team will be aided by an important recent arrival in Jeffrey Burchell, former co-CIO at Aston Hill Asset Management Inc. in Toronto. Chan says Burchell adds strength to Gluskin Sheff’s alternative-investments expertise.

Chan has a one-year price target of $31 a share, while Khan’s is $27. The 31.6 million outstanding shares closed at $22.40 on Oct. 13.

The quarterly dividend rose to 22.5¢ from 22¢ last year.

Gluskin Sheff’s net income for the year ended June 30 was $52.3 million on revenue of $164.5 million. That was down from net income of $106.8 million on revenue of $247.5 million in the corresponding period a year earlier.

The sharp declines were due to lower performance fees in the most recent fiscal year – $55 million vs $156.5 million.

© 2015 Investment Executive. All rights reserved.