Uncertainty about the consequences of the U.K.’s withdrawal from the European Union (EU) in 2019, combined with rising populist governments in a handful of countries and immigration issues, has increased tension in Europe. But, overall, the region is moving in a positive direction, with modest economic growth.

The eurozone’s economy is growing at a steady rate of about 2% annually. The European Central Bank (ECB) has held back on interest rate increases, unlike the U.S. Federal Reserve Board, which has raised leading interest rates three times this year. In fact, the ECB is not expected to hike interest rates until mid-2019 – although it’s set to end its quantitative easing bond-buying program by this December.

Meanwhile, the euro has weakened against the U.S. dollar this year, providing a bit of a tailwind for Europe-based exporting companies that benefit from a favourable exchange rate. Overall, key European stock indices have been more or less flat in 2018.

European stock valuations remain more attractive than in the U.S. stock market. Although the pace of economic growth is slower in the eurozone than in the U.S., the former’s economy has seen positive growth for 20 consecutive quarters – and wages are rising. The unemployment rate as of Aug. 31 was 8.1%, the lowest level since November 2008.

The uncertainty surrounding how Brexit will unfold continues, but the drop in U.K. stock valuations in the wake of the 2016 Brexit referendum presented opportunities for investment fund portfolio managers to pick up bargains in shares of companies with positive long-term prospects and stock prices that have come off their lows.

A handful of other countries in Europe are undergoing political shifts that may trigger market volatility – including Italy, which has a populist coalition government since an election this past March. The new government began with strong rhetoric, including raising government spending, cutting taxes, reducing the retirement age and reversing some pro-growth reforms.

The fear is that these measures will worsen Italy’s fiscal deficit, resulting in a debt crisis that could spill over into the rest of Europe and become a wider problem. Italy’s banking system is viewed as shaky and there are some connections to other EU banks.

Germany’s chancellor, Angela Merkel, has a strong grip that may be slipping as that country’s political far right gathers momentum, while the government in France appears relatively stable under the centrist leadership of Emmanuel Macron, who was elected in 2017.

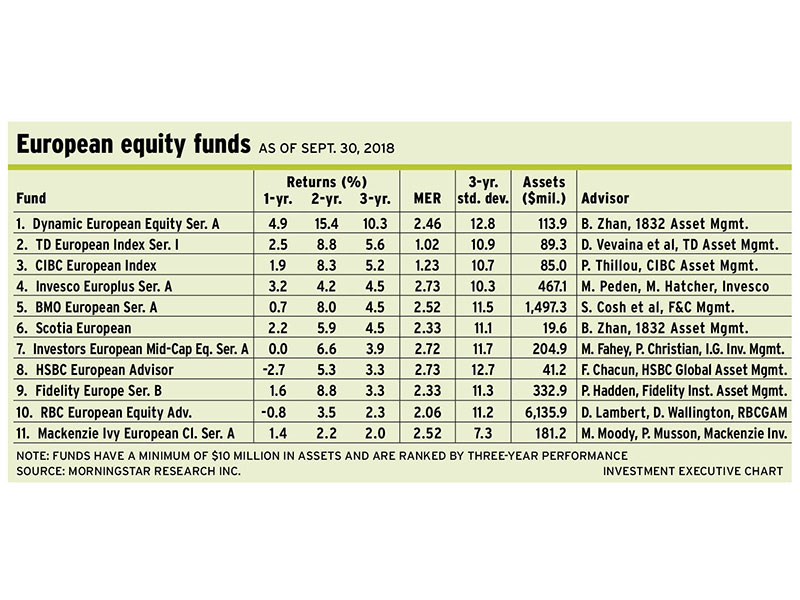

“Europe is stable and growing steadily, although not as fast as the U.S.,” says Matt Peden, vice president and portfolio manager with Atlanta-based Invesco Advisers Inc. and co-manager of Invesco Europlus Fund (along with Michael Hatcher, head of global equities for Invesco Canada).

The eurozone is in a less advanced stage of economic recovery than the U.S., Peden says, as the ECB was later in implementing stimulative policies such as quantitative easing than other central banks were. And Europe now is acting later than other global regions in unwinding these policies.

The Invesco fund has a highly concentrated portfolio of 15 to 20 stocks, and top holdings can account for as much as 7%-8% of assets under management (AUM). Currently, the highest geographical weighting is in the U.K., at 28% of AUM, followed by France at 14% and Germany at 8%.

U.K. holdings are a mix of domestically focused companies and multinationals, including Unilever PLC, the world’s largest consumer goods company, and Reckitt Benckiser Group PLC.

Unilever produces food, cleaning and personal-care products under famous brand names such as Dove, Lipton and Hellmann’s. Reckitt is known for a variety of health and household items, including Lysol cleaning products, Strepsils cough remedies and Dr. Scholl’s footwear.

On the domestic side, another U.K. name, and a strong contributor to recent fund performance, is Howden Joinery Group PLC, a leading supplier of kitchen components to the building trade in the U.K. housing market and which has a strong share of the renovation business. The firm supplies everything for a kitchen, including appliances, cabinets and countertops, Peden says.

Earlier this year, the Invesco team sold off the fund’s only resources-related holding: U.K.-based Rotork PLC, which produces flow-control equipment such as valves and “intelligent” electric actuators for the oil business. The actuators adjust machinery valves automatically and reduce the need for more expensive manpower. Although growth remains healthy, valuations rose to a level that indicated taking profits was advisable, Peden says.

The Invesco portfolio managers also liquidated a position in Diageo PLC due to elevated valuations. London-based Diageo is one of the world’s largest producers of beer and spirits, selling such popular brands as Smirnoff, Johnnie Walker, Baileys and Guinness in 180 countries.

Although Europe doesn’t have global goliaths in the infotech sector similar to U.S.-based Apple Inc., Peden says, he has found value in “local champions.”

For example, the Invesco fund holds shares in Scout24 AG, a Germany-based company specializing in online listings for real estate and automobiles in Europe.

Another top holding in the Invesco fund is Edenred SA of France, a digital payments company and a leader in developing prepaid payment cards and service vouchers for corporations’ employees. Edenred’s products help companies manage items such as fleet fuelling costs and employee travel expenses.

matt moody, vice pres-ident and portfolio manager with Mackenzie Investments and co-manager of Mackenzie Ivy European Class fund (along with Paul Musson, senior vice president, investment management), says that although European stock valuations may appear more attractive than U.S. stocks in general, much of the differential is due to Europe’s smaller exposure to tech giants.

The FAANG (Facebook Inc., Apple, Amazon.com Inc., Netflix Inc. and Alphabet Inc. [a.k.a. Google]) stocks have contributed to much of the U.S.’s market strength, but tech stocks account for only about 5% of the MSCI Europe index vs 18% of the MSCI world index, Moody says.

“Tech stocks are expensive in Europe, but they don’t account for as big a weighting in the [Europe] index,” Moody says. “Overall, European stock valuations may appear more attractive than other regions, but if you drill down to the sector level, that’s not really the case for most sectors.”

The exception, Moody says, is financial services – a sector that has been affected by low valuations for European banks, many of which are regarded as risky.

“We haven’t held [shares of] a European bank in the fund for 12 years,” Moody says. “Banks are generally less attractive in Europe than elsewhere. There are various financial strains in the eurozone, and many of the banks are opaque black boxes, [for which] it’s hard to understand the nature of the risks. Many are not robustly financed.”

The Mackenzie fund does have some financial services sector exposure, but it’s not in banks. The fund invests in Admiral Group PLC, a Wales-based car insurance company, and Burford Capital Ltd., a London-based investment-management company with offices in New York and Chicago. Burford provides capital on a worldwide basis to corporations and law firms engaged in litigation, arbitration and other legal finance and advisory activities.

“We look for companies that are exposed to global customers and have global operations,” Moody says. “We are less interested in companies that are entirely inward-looking and domestically focused. [We look] for great businesses we can understand, that are conservatively run and financed, and that we are confident can succeed over the next 10 years.”

As with the Invesco fund, the Mackenzie fund’s largest geographical exposure is in the U.K., which accounts for 26% of AUM. Another similarity is that Reckitt also is a top holding in the Mackenzie fund.

Moody avoids Italian stocks due to concerns about the country’s high debt levels and business environment.

He recently took advantage of price weakness to add to the Mackenzie fund’s holdings in both Reckitt and another key holding – Henkel AG & Co. KGaA, a Germany-based multinational chemical and consumer goods company. Henkel derives about half of its revenue from consumer products such as Dial soap; the other half from industrial adhesives.

The Mackenzie fund sold its shares in two firms earlier this year because their stock prices increased along with rising oil prices and provided a profit- taking opportunity: Rotork (also sold by the Invesco fund) and TGS NOPEC Geophysical Co. ASA, a Norway-based provider of geophysical and geological data to resources exploration firms.