Real estate equities have proved to be highly resilient in the past year. That is in contrast to global equities markets, which have gyrated over fears of an economic slowdown in the U.S. and China, and the U.K. decision to leave the European Union.

Although real fixed-income yields have trended downward and, in many cases, into negative territory, real estate-based securities are expected to hold their own and generate comparatively better returns.

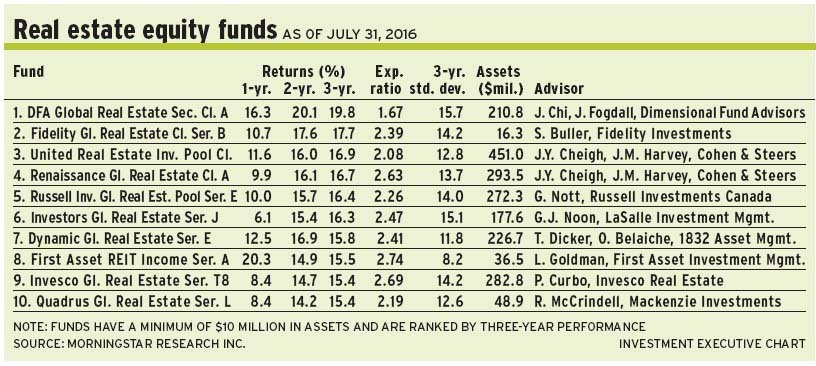

“The biggest reason why real estate investment trusts [REITs] have done well is the global search for yield,” says Tom Dicker, portfolio manager with Toronto-based 1832 Asset Management LP, and portfolio co-manager of Dynamic Global Real Estate Fund. He works with Oscar Belaiche, senior vice president of 1832.

“The biggest factors behind that are central bank actions in Europe and Japan that have been highly accommodative and offer very loose monetary policies,” says Dicker. “In both regions, there are negative central bank interest rates. That has pushed [investments’] yields all the way up the risk curve.”

Sovereign and corporate bonds have rallied in recent months, as have so-called “junk” bonds and infrastructure-related assets. “All of these yielding assets, which are a bit further up the risk curve, have seen their yields compress and valuations increase. That’s largely due to what’s happening in the bond market,” says Dicker.

“There is a real scarcity of defensive, safe assets that have visible growth,” he adds, “especially bricks-and-mortar assets. Publicly listed real estate is one of the ways to get visible growth and a solid dividend. That combination has performed extremely well and is the driver of what’s happening.”

Dicker argues that the bond markets, which determine the cost of borrowing, are in good shape: “We had a scare at the beginning of the year when spreads widened and REITs sold off a bit, but credit seems to be fairly healthy. We’re in the later innings of the credit cycle. It looks like this lower-for-longer interest rate scenario has legs.”

From a valuation perspective, Dicker admits that real estate securities are somewhat expensive; U.S. REITs are trading at around 23 times adjusted funds from operations vs 15.5 times for the long-term average. Moreover, during the 2008-09 global financial crisis, REITs traded at 20 to 24 times. “But you are not comparing apples to apples, because the quality of real estate in U.S. REITs is much higher today. They are better businesses.”

About 30% of the Dynamic fund’s assets under management (AUM) is in the retail real estate sector, 17% is in diversified real estate firms, 12% is in residential, 9% is in office and 6% is in smaller holdings such as self-storage.

AUM is divided equally among securities from Canada, the U.S. and the rest of the world.

One leading name in the 53-name Dynamic fund is Weyerhauser Co., the largest timber REIT and largest private land owner in the U.S. Weyerhauser has recently restructured, Dicker notes: “[The company] now is closer to a pure-play timber-land company. There is a big opportunity for the multiple to be re-rated upward.”

Weyerhauser stock is trading at about US$32.50 ($41.50) a unit, and pays a 3.78% dividend. Dicker believes the net asset value is greater than US$36 a unit.

the real estate sector has weathered volatile markets mainly because “the fundamentals are OK, on average, to slightly above average,” says Steve Buller, vice president at Boston-based FMR LLC (a.k.a. Fidelity Investments) and portfolio manager of Fidelity Global Real Estate Fund.

“For commercial real estate, demand slightly exceeds supply on balance, and occupancy rates continue to be maintained and, in some cases, are going up,” Buller says. “This creates the ability for rents to go up. The fundamentals are good, even within this tepid global economy.”

Buller, like DIcker, notes that investors are seeking bricks-and-mortar assets that offer tangible yields: “We live in a world in which two-thirds of government bonds are paying 0% or negative yields. In a yield-hungry world, property is an excellent [alternative]. Those assets with tenants that have contractual leases are, obviously, fairly desired.”

Is real estate sensitive to interest rate movements? Buller argues that is not the case: “The correlation between global real estate and global bonds, going back to 1996, is 0.28%.”

Still, he acknowledges that in some shorter periods, such as 2011-14, the two asset classes were closely correlated and, in 2005-08, there was negative correlation.

But the main reason for the modest long-term correlation is a tug-of-war between the fundamentals and the cost of capital, Buller says: “If you live in an economy that is doing well, it’s perceived to have rising interest rates.” On the flip side, though, a world of rising interest rates means the cost of capital is rising, which can affect real estate adversely. However, today’s low cost of capital suggests that “the tug of war is somewhat balanced,” says Buller, adding that REITs and real estate securities are generally fairly valued.

About 35% of the Fidelity fund’s AUM is in diversified real estate firms, 21% is in residential, 18% is in retail and 16% is in offices. There are smaller weightings in sectors such as health care.

About 54% of AUM is in the U.S., 10.5% is in Japan, 8% is in the U.K., 5.8% is in Hong Kong and there are smaller weightings in markets such as France.

One top holding in the 78-name Fidelity portfolio is Host Hotels & Resorts Inc., a leading REIT that owns properties carrying hotel brands such as Marriott and Westin.

“Host Hotels has an underleveraged balance sheet and is using that capacity and free cash flow to buy back shares,” says Buller, adding that the firm benefits from strength in its so-called “group” business, which typically picks up late in the economic cycle.

Host Hotels stock is trading at about US$17.30 ($22.50) a share and pays a 4.7% dividend. .

property markets around the world generally are healthy, agrees Paul Curbo, managing director at Dallas-based Invesco Real Estate, a division of Invesco Ltd., and portfolio manager of Invesco Global Real Estate Fund. “Demand is outpacing supply, resulting in improving occupancy rates, rental rates and cash flows,” he says. “That’s the healthy backdrop.”

But the picture is murkier on the capital markets side; rates have been trending downward. In the U.S., the benchmark 10-year treasury rate has fallen to about 1.5% from 2.4% at the start of the year.

Yet, Curbo is concerned about the impact of negative yields in countries such as Germany and Japan: “Longer term, the risk is that capital markets are tied to central bank policies. Correlations among REITs and stocks are higher today than historically is the case. That indicates to us that the performance of the asset class is increasingly tied to macro and central bank policies and less tied to individual real estate fundamentals.”

With much of the world mired in negative interest rates, “the risk is that the capital markets can change,” says Curbo. “If interest rates do move higher and there is a ‘normalization’ of rates, that would be a negative for the [real estate] market.”

And Curbo is reluctant to predict when, or how, that might occur: “That’s not a question for me to answer. It’s a broader question. I would just suggest that if [rates] do change, it would have negative consequences for the [real estate] asset class.”

From a valuation perspective, Curbo believes that, globally, the asset class trades at a 3% premium to the underlying value. “The sector has performed well and asset values have been stable,” Curbo says, adding that there is a 7% premium in the U.S. and 13% premium in continental Europe. However, some markets have suffered, as in the case of Hong Kong, which trades at a 37% discount to underlying values.

About 30.5% of the Invesco fund’s AUM is in diversified firms, 20% is in retail, 13% is in residential, 10.7% is in office and there are smaller holdings in sectors such as health care.

The U.S. is the largest weighting at 55% of AUM, followed by Europe (13%), Japan (11%), and Hong Kong (7%). There are smaller positions in markets such as Australia.

One top holding in the 120-name Invesco fund is Hudson Pacific Properties Inc., a U.S.-based REIT that is active mainly in the office sector on the U.S. West Coast.

“[Hudson Pacific] will have double-digit cash-flow growth over the next several years. And [the units] trade at a 20% discount to {the REIT’s] underlying real estate value,” says Curbo, adding that the market has been concerned about the West Coast’s technology sector. “But we think that the San Francisco Bay area has the best long-term fundamentals in the U.S. That’s where job creation is occurring.”

Hudson Pacific REIT trades at US$32.75 ($42.60) a unit and pays a 2.8% dividend. There is no stated target.

Another favourite is Retail Opportunity Investments Corp. (ROIC), which owns and manages shopping centres on the U.S. West Coast.

“There is very little new construction because of the tremendous barriers to new malls,” says Curbo. “[ROIC] still is able to acquire shopping centres that add to its growth. Management is very hands-on in terms of redeveloping and improving their malls.”

ROIC trades at US$22.30 ($29) a unit and pays a 3.3% dividend.

© 2016 Investment Executive. All rights reserved.