The price of gold bullion has done a 180° turn in the past year and rallied by 20% to about US$1,325 an ounce, thus lifting precious metals stocks to much higher levels. Fund portfolio managers are convinced that the rally is sustainable, thanks largely to monetary easing policies of several central banks, which has resulted in negative bond yields in some countries.

“Quite a number of countries around the world have very easy monetary policies, especially Japan and the U.K., which are in outright stimulus mode,” says Robert Cohen, vice president and portfolio manager with Toronto-based 1832 Asset Management LP and portfolio manager of Dynamic Precious Metals Fund.

“There’s a strong correlation, long term, between global liquidity and the gold price,” says Cohen. “Everyone is looking at the [U.S.] Federal Reserve [Board]’s forward path on interest rates. Rates probably will stay ‘lower for longer’ because there is an election coming up and [the Fed] is unlikely to will make noise before or immediately following an election.”

In Cohen’s view, the earliest date for a U.S. interest rate hike will be in March 2017 – and it is likely to be modest.

“We’ve seen some better than expected housing starts. But the U.S. still has a huge trade deficit, which increased in June. Trade with China is becoming a big election issue with [presidential candidate] Donald Trump,” says Cohen. “The U.S. dollar [US$] is overvalued amid a bunch of other countries. So, the U.S. doesn’t want its interest rates too high compared with everyone else because that will only exacerbate the trade deficit.”

Another factor pushing up the price of gold is the growth of gold exchange-traded funds (ETFs), which buy bullion directly and have increased their holdings by about 570 tonnes year-to-date.

“ETFs are now the size of a large central bank,” says Cohen. “To us, that causes more volatility. I’d rather not have them around and have more stability in the gold price.”

In 2013, Cohen notes, investors dumped gold ETFs en masse and sent the gold price crashing.

“ETFs tend to push the gold price up higher in a strong market, but also push the price lower in a weak market,” he says.

Cohen is reluctant to forecast the future gold price. “That’s not my job. But the trend is upward,” he says. “I’m betting on monetary easing and a low real interest rate environment prevailing. [The trading environment] doesn’t have to be negative bond yields, [but] just below 2%. We’re a long way before interest rates surpass inflation.”

From a valuation standpoint, Cohen says gold stocks are trading at “fair” valuations, although there is a wide range within the asset class.

“The [global] financial crisis did see a compression of valuations. Now, they are slowly creeping back up to pre-crisis levels,” he says. “But we’re not there yet; we’re about 30% off.”

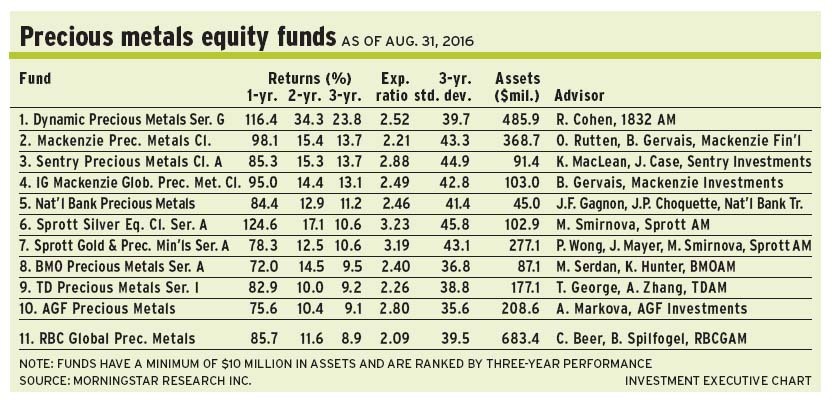

Cohen is a bottom-up investor. About 42% of the Dynamic fund’s assets under management (AUM) is in junior companies, 42% is in intermediates, 13.5% is in senior gold-mining firms and the balance is in cash.

A favourite name in the Dynamic portfolio, which holds about 35 names, is Semafo Inc. That firm produces about 225,000 ounces of gold from a mine in Burkina Faso. Production is expected to climb to 400,000 ounces by 2019 as new mines come onstream.

Semafo stock is trading at about $6.25 a share. There is no stated target.

The key driver behind the price of gold is the fact that global central banks and governments are struggling to maintain economic growth momentum, says Onno Rutten, vice president, investment management, global resources team, with Toronto-based Mackenzie Financial Corp. and portfolio co-manager of Mackenzie Precious Metals Class Fund. He works with Benoît Gervais, senior vice president, investments, resources portfolio team, at Mackenzie.

“In order to do that, [central banks] continue to deploy very accommodative policies,” Rutten says. “In the past year, we’ve seen this response [reflected] in gold because [central banks] have moved more and more down the yield curve and into real negative interest rates.”

Rutten believes that central banks will remain accommodative for some time.

“The European Central Bank, for example, is exploring further easing measures. There’s a growing realization that long-term growth rates for mature economies continue to be very low,” says Rutten, noting that structural underpinnings include aging populations and weak productivity gains.

More important, Rutten expects authorities to turn to fiscal stimuli, in the form of spending on infrastructure projects.

“The last taboo would be if central banks funded governments. This is actively being studied in Japan. The European Union also is talking about this because they have to show something to the people, more than just the bare necessities, ahead of elections in 2017,” says Rutten, noting that elections will be held next year in France, Germany, the Netherlands and, possibly, Italy.

The risk on the downside, says Rutten, is if economies slip into a so-called “Goldilocks” environment of steady growth momentum and low inflation.

This situation would cause central banks to raise interest rates and, assuming inflation was low, result in rising real rates – effectively undercutting the price of gold bullion because it doesn’t pay any dividends or interest.

“Right now, the base case is for moderate to low growth, and somewhat rising inflation. There’s a low probability to a downside scenario,” says Rutten.

The gold bullion price may increase gradually to about US$1,500 an ounce, says Rutten. He suggests that investors keep a modest portion of their assets in gold now as insurance, while gold prices are low.

“Central banks have moved into policies that have never been deployed before,” says Rutten. “In Denmark, for example, banks would pay you earlier this year to take a mortgage on your house. We are moving into uncharted territory.”

Rutten is a bottom-up investor. The Mackenzie fund’s AUM is spread in roughly equal measure among large-, medium- and small-cap stocks.

A longtime favourite holding in the 60-name Mackenzie fund is Detour Gold Inc., which is developing a mine in northern Ontario that has the potential to produce 600,000 ounces of gold a year.

“Detour benefits from a uniquely long reserve life of 22 years, which reduces the need to invest in capital expenditures or acquisitions,” says Rutten, adding that the firm is benefiting from the low Canadian dollar (C$) and diesel prices.

Detour stock is trading at about $30.85 a share. There is no stated target.

Another favourite is Richmont Mines Inc., a junior firm that operates mines in Quebec and Ontario. Richmont stock is trading at about $13.65 a share, or more than double the price at the start of the year. There is no stated target.

“Its share price has benefitted from exploration successes, the ramp-up of mine production – thanks to higher-grade ore – strengthening of management and the weaker C$,” says Rutten.

The gold bullion price could sink to US$1,200 an ounce, but there are too many factors that argue in favour of gold pushing higher than it is currently, says Chris Beer, vice president at Toronto-based RBC Global Asset Management Inc. (RBCGAM), and lead portfolio manager of RBC Global Precious Metals Fund. He works with Brahm Spilfogel, vice president and senior portfolio manager with RBCGAM.

“The negative real interest rates, mounting level of global debt and growing trend to populism in the U.S. and Europe are key drivers,” says Beer. He notes that populist movements, which are fed by anti-immigration sentiments, are prompting some investors to seek shelter in gold bullion.

“And today we see that the European Central Bank has hit US$1 trillion in quantitative easing. [That strategy] hasn’t done a lot for the real economy, although it’s done a lot for risk assets such as equities. The next shoe to drop is additional quantitative easing and fiscal stimulus.”

Like Rutten, Beer observes that governments are considering fiscal policies aimed at increasing infrastructure spending in order to pump growth into their flagging economies.

“You will, at least, have something to show for the money – such as roads and bridges. But that [strategy] is potentially inflationary as well,” says Beer. “All these things combined create a decent tailwind for gold.”

Echoing Cohen’s comments, Beer says clients have rushed back into gold ETFs after having exited them in 2015. Since then, buying has pushed gold ETFs’ holdings back up to about 2,000 tonnes from 1,300 tonnes.

“Gold generally is inversely correlated with the US$ and interest rates. From 2003 to the end of 2011, the US$ was weak – and that pushed up bullion,” says Beer. “Today, the level of the US$ could see a ‘retest’ in the gold price. That’s if we see interest rates rise in the U.S. and the differential will favour the US$ against other currencies. But for a ‘gold bug,’ the current environment of negative rates and other macro themes probably outweigh the positive gold trend we saw in 2003-11, which was based only on the US$ phenomenon.”

Beer believes that the gold bullion price could rise to about US$1,400-US$1,500 an ounce within a year – not his yardstick.

“If we start using US$1,400 or US$1,500, then stocks are very inexpensive. But we’re not trying to pick stocks on the gold price per se,” he explains. “We’re trying to pick stocks on the basis of companies that can grow their production and their reserves irrespective of the gold price.”

About 50% of the RBC fund’s AUM is held in mid-sized companies, 33% is in small-caps and 15% is in large-caps.

A favourite mid-cap firm in the RBC fund, which has about 90 holdings, is OceanaGold Corp. This firm is advancing its so-called “Haile project,” which OceanaGold assumed when it acquired Romarco Minerals Inc. in 2015, toward commercial production.

“[OceanaGold] stock is trading at five times enterprise value to earnings before interest depreciation and amortization, vs eight to 10 times for its peers,” says Beer. “[The firm] has growth and one of the best balance sheets.”

OceanaGold’s annual production of 550,000 ounces could climb by another 150,000 ounces, based on revised estimates of an existing project, he says.

OceanaGold’s share price, which has doubled in the past year, is about $4.70 a share. There’s no stated target.

© 2016 Investment Executive. All rights reserved.