Real estate equities have generated double-digit returns in the past 12 months on the back of strong demand for income. And although fund portfolio managers are divided over valuations, generally, there is optimism about prospects.

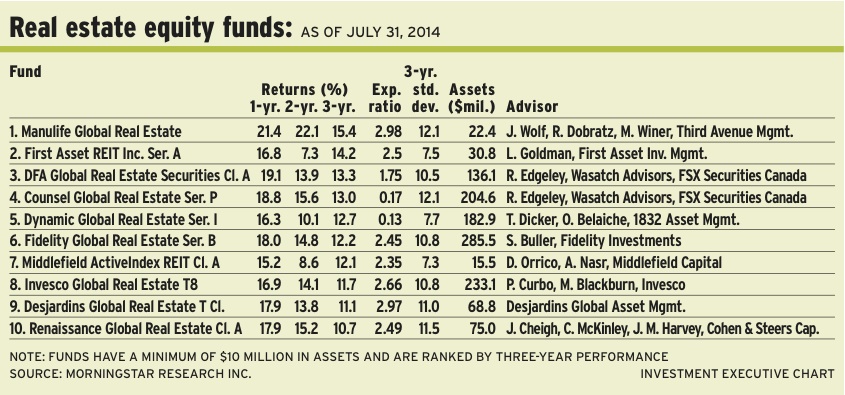

“Gateway cities of the world, such as New York, London or Hong Kong, are experiencing extreme demand for real estate investments,” says Jason Wolf, a portfolio manager with New York-based Third Avenue Management LLC, and portfolio co-manager of Manulife Global Real Estate Fund, “whether it’s from private individuals, or pension funds or sovereign-wealth funds. All have found real estate an attractive asset allocation over a longer time horizon.

“It may be because of inflation protection,” he continues, “or attractive relative yield, in the context of other fixed-income, and the protection that real estate affords you with something physical.”

Wolf works with Ryan Dobratz and Michael Winer, portfolio co-managers at Third Avenue Management.

Commercial real estate prices have recovered to levels before the financial crisis on a price/square foot basis, Wolf adds, and access to capital remains strong: “It’s as good as it has ever been. But lending has remained quite constrained, so we’re not back to the heady days of 2007.”

Moreover, construction activity, especially in the commercial sector, remains anemic. “This is largely due to the uncertainty in the economic recovery from the demand side,” Wolf says. “Occupancies have increased and rental rates are up modestly. But the risk appetite for speculative construction is not there. In most cases, supply and demand looks really good.”

Meanwhile, says Dobratz, real estate investments trusts (REITs) that hold high-quality real estate reflect a lot of these trends: “If you look at the U.S. market, REITs are trading at a premium to net asset value, in the 7%-8% range, and dividend yields are at record lows, near 3%. As value investors, we don’t get too excited about those valuations.”

Wolf adds that the attractive opportunities exist in three areas: commercial real estate firms with valuable development pipelines; companies that have strong ties to the U.S. residential market; and certain special situations, such as recapitalized European companies.

The Manulife fund’s portfolio managers have lowered the REIT weighting to 32% of assets under management (AUM). There also is about 48% in stocks and 20% in cash. On a geographical basis, about 36% of AUM is in the U.S., 16% is in the U.K. and 11% is in Hong Kong, with smaller weightings in countries such as the Netherlands.

Running a portfolio with about 40 names, the portfolio managers like Weyerhauser Co., a leading forest-products provider. Says Wolf: “One of the places that offer value in the U.S. is through the inputs in the home-building market. Weyerhauser is the very first step in the process.”

Acquired in late 2010, at less than US$17 a share, Weyerhauser stock is trading at about US$31.50 ($34.40) a share. Although there is no stated target, Wolf believes the stock trades at a 15%-20% discount to net asset value (NAV) of about US$39 a share.

Tom Dicker, a portfolio manager with Toronto-based 1832 Asset Management LP and co-manager of Dynamic Global Real Estate Fund, expresses concern that there are overheated conditions in some regions. Specifically, he points to Paris-based Unibail-Rodamco SE, Europe’s largest commercial real estate company, which launched a convertible bond with a 0% coupon.

“Whenever you get an artificially low discount rate,” Dicker says, “so-called ‘long-life’ cash flows like those from real estate could be overvalued. Right now, we are at risk of having too low a discount rate, because bond yields are so low.”

Dicker shares portfolio- management duties with Oscar Belaiche, senior vice president at 1832 AM.

On the positive side, Dicker notes, there is little new supply in most sectors of the U.S.: “When it comes to retail, for instance, there is very little new supply. There is some new industrial supply, but it’s below the rate that older properties are scrapped. But what’s important in the U.S. is growth in employment. That’s helping consumer spending and the takeup of office space. Vacancies are generally declining.”

The big uncertainty is the direction of interest rates, which caused real estate valuations to plummet in the summer of 2013.

Thus, Dicker is reluctant to make any predictions.

“We focus on companies that will do well in an environment, which is generally getting better,” says Dicker. “If rates do rise, and it’s caused by a better economy, you want to be in more pro-cyclical sectors, such as hotels, which are the most economically sensitive.”

Dicker adds that the Dynamic fund’s hotel and gaming exposure is the highest it has been, at about 8% of AUM.

From a strategic viewpoint, about 70% of the Dynamic fund’s AUM is in REITs, 26% is in stocks and 4% is in cash. On a geographical basis, about 41% is in the U.S. and 32% is in Canada, with smaller holdings in countries such as France.

One top holding in the 58-name Dynamic fund is Morguard Corp., a Canada-based firm with diversified real estate interests. Says Dicker: “[Morguard trades] at a substantial discount to the net asset value.”

Dicker estimates that Morguard’s NAV is $225 a share, although the shares trade at $144.50. The wide discount is attributable to the fact the shares pay a low dividend and are thinly traded.

Real estate’s fundamentals are improving gradually, agrees Steven Buller, vice president with Boston-based FMR LLC (a.k.a. Fidelity Investments) and portfolio manager of Fidelity Global Real Estate Fund. Buller, like his peers, notes that supply and demand generally are in balance, and financing new projects, while not as easy as before the global financial crisis, is obtainable.

“If you look at the U.S. or Hong Kong,” says Buller, “we are still in a period in which demand exceeds supply. Occupancies will pick up, although it’s less of an occupancy pickup game and more of a rental rate game, and rental rates will continue to move higher.”

Although U.S. economic growth is tepid, Buller believes this is a good environment to be in because it creates a more stable background for real estate. Moreover, access to capital is wide open to publicly listed companies.

“Money is cheap,” says Buller, adding that balance sheets generally are in better shape than before the financial crisis. At the same time, thanks to stronger cash flows, dividends are up and the yield on U.S. REITs is about 3.8%.

However, valuations are up, too, and global stocks are trading at a slight premium to NAV, says Buller, noting that NAVs also are rising due to growing cash flows.

“We argue that global stocks should trade at a slight premium,” says Buller. “One, they offer liquidity that is cheap. Two, you are getting professional management. And, three, there is a lot of transparency. Companies must always tell their story to access more capital.”

A bottom-up investor, Buller does not discriminate between stocks and REITs. About 66% of the Fidelity fund’s AUM is in the latter, with 32% in stocks and 2% in cash. On a geographical basis, 43% of AUM is in the U.S., 13% is in Japan and 8% is in the U.K., with smaller holdings in countries such as France.

Running a portfolio holding about 86 names, Buller likes firms such as Public Storage REIT, a U.S.-based REIT that is benefitting from generally consistent demand for storage.

“[Storage] is one sector in the U.S. that has seen low amounts of new supply,” says Buller, adding that Public Storage is the dominant industry player. “Public Storage and other operators have the ability to push fairly sizable rent rate increases, which translates into cash-flow growth.”

Public Storage, which yields about 3.3%, is trading at roughly US$171.40 ($187.25) a unit.

© 2014 Investment Executive. All rights reserved.