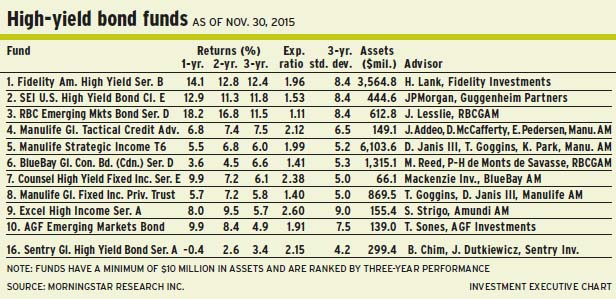

High-yield bond funds encountered significant challenges late in 2015 due to the impact of slumping oil prices on energy producers and gradually rising default rates. Yet, fund portfolio managers remain upbeat and note that there are pockets of value in this asset class.

“The overriding theme is that the market is recognizing – and we agree – that we are fairly late in the credit cycle, which has lasted seven years,” says Ben Chim, senior portfolio manager at Toronto-based Sentry Investments Inc. and portfolio co-manager of Sentry Global High Yield Bond Fund. He shares portfolio-management duties with James Dutkiewicz, chief investment strategist at Sentry.

Typically, Chim says, the cycle’s end is marked by rising default rates and declining so-called “recovery rates” (the amount bondholders can recover in a bankruptcy).

“There are growing concerns about those two issues,” says Chim. “And with energy company bonds trading at 65¢ on the dollar, on average, it’s apparent that those factors – rising default rates and falling recovery rates – will be present near the end of this cycle.”

Given the market’s deterioration, this phase “is not going to be as benign as some had originally expected, given a backdrop of accommodative central bank policies,” adds Chim.

Moreover, although the U.S. Federal Reserve Board finally raised interest rates in December, more hikes may or may not be on the way, he says: “The fear is less around whether or not the 25-basis-point (bps) hike in the Fed funds rate will damage asset prices or global growth. It’s more like: ‘What is the trajectory of [future] interest rate increases that the Fed will take?'”

What is certain, for now, is that U.S. high-yield bond spreads over treasuries have widened to about 650 bps, according to the benchmark Bank of America Merrill Lynch high-yield master II index, vs 450 bps last summer. Half of the increase is attributable to weakness in the resources sector.

“The average spread on energy companies is 1,000 bps,” says Chim. Meanwhile, he adds, default rates have risen in the past year to 2.8% from 2%, indicating troubling times. “There are some risks in the market. It is definitely going to be more volatile.”

But with the benchmark yielding about 7.5% (excluding resources firms), Chim argues that some attractive valuations have emerged. The telecommunications and health-care sectors, for example, offer “pockets of opportunity.”

Currently, about 70% of the Sentry fund’s assets under management (AUM) are in high-yield bonds, plus 22% in investment-grade bonds and 8% in cash. The average duration within the Sentry fund is 3.9 years, vs 4.4 years for the benchmark.

On a geographical basis, about 49% of the Sentry fund’s AUM is in U.S., and the balance is in Canada, Europe and emerging markets. The average credit rating is BB-plus.

Financials comprise the largest holdings, at 30% of AUM, followed by consumer discretionary (15.5%), industrials (12%) and energy (10%).

Chim, running a portfolio with about 60 names, likes issuers such as Olin Corp., a U.S.-based chemicals firm that supplies makers of fertilizers and plastics. Olin’s BB-plus rated bond, used to finance an acquisition, matures in 2023 and yields 8%. Says Chim: “There is some scope for spread tightening.”

The sell-off of energy- and commodities-related bonds has led to concerns that the sell-off will spread to the rest of the high-yield universe, says Harley Lank, vice president with Fidelity Investments Asset Management, a unit of Boston-based FMR LLC, and portfolio manager of Fidelity American High Yield Fund.

“Anytime you go into periods of ‘risk-off’ markets,” he says, “there is volatility and people become more concerned about the health of the global economy.”

Lank maintains that the Fed’s rate hike in December was a welcome development: “[A rate hike] usually is indicative of an improving economy. And that’s definitely a positive thing for high-yield bonds.”

Indeed, Lank notes, high-yield bonds generated positive returns in the five periods over the past 15 years when U.S. treasuries’ yields rose by 100 bps or more.

“[High yield] is a fixed-income instrument, but not one nearly as sensitive as government bonds. For these reasons, the Fed ‘lift-off’ will be a positive backdrop for high yield. There’s been a mismatch between valuations and positive fundamentals,” says Lank, noting that last year’s negative returns in U.S.-dollar (US$) terms (but positive returns in Canadian dollars) was an anomaly.

Although the default rate for high yield bonds has risen, Lank points out that this rate is a long way from the 5% long-term average.

“The default rate has gone up because of the commodity space – metals and mining, and oil and gas are hurting. But there’s been a record amount of new issuance over the past six years, and most of the proceeds have been used to refinance existing debt,” adds Lank. “As a result, most companies have really good balance sheets, and less than 5% of the debt outstanding is coming due over the next two years. On a mathematical basis, it’s going to be really hard to get to that long-term [default rate] average.”

From a strategic viewpoint, Lank has allocated about 85% of the Fidelity fund’s AUM to high-yield bonds, 8% to a mix of bank debt and floating-rate debt, and about 7% to cash. The average duration is four years.

Diversified financials comprise the largest sector, at 17%, followed by health care (12.5%), telecom (11.5%), and energy (11.2%). About 37% of the bonds are rated BB; 37% B; there are smaller exposures to CCC-rated and BBB bonds.

The highly diversified Fidelity fund contains about 650 securities from 325 issuers. There is a large weighting in Ally Financial Corp., the former financing arm of General Motors Corp., which was spun off in 2008.

“In our view, [Ally] has an A-rated balance sheet, but the bond is trading like a BB-rated security,” says Lank. “Ally continues to inch closer to investment-grade. When that happens, spreads will tighten and we’ll make good total return with good downside protection.” The Ally 2031-dated bond is yielding about 5.5%.

Another favourite is Hospital Corp. of America (HCA), the largest for-profit hospital organization in the U.S. “[HCA is] recession-resistant and has a lot of industry tailwinds with the Affordable Care Act being implemented in 2015,” says Lank. “[HCA] has generated a lot of free cash flow growth.” The Fidelity fund’s holdings in HCA – six bonds with maturities ranging between 2020 and 2025 – offer an average yield of 5.5%.

Emerging-market bonds are part of the high-yield asset class, yet investors have to be reminded of key differences vs U.S. high-yield bonds, says Sergei Strigo, head of emerging markets debt and currency at Amundi Asset Management in London, U.K., and portfolio manager of Excel High Income Fund.

“You might argue there is a similar oil and gas sector weighting within the asset class, but these emerging-market companies are very different from their [U.S.] counterparts,” says Strigo, noting that many emerging-markets firms are either state-owned or state-supported.

“With exports in U.S. dollars, and costs denominated in local currencies, which, in many cases, have depreciated, [there is] not a lot of stress on [emerging markets resources firms] to produce,” says Strigo. “That’s not the case with U.S. producers. That’s where the main divergence between U.S. high-yield and emerging-markets bonds is coming from.”

Strigo acknowledges that spreads between emerging- markets government bonds, as represented by the benchmark J.P. Morgan emerging market bond index, and U.S. treasuries have widened since last summer by about 50 bps to 400 bps.

“We are trading at the levels we were at in 2011 and 2012 on a spread basis,” Strigo says. “But we’re not at distress levels. In fact, there is value in the asset class.”

The fundamentals for emerging-market debt are considerably stronger than in the late 1990s, Strigo argues, as foreign-exchange reserves are much higher and the amount of foreign-currency debt outstanding is much lower.

“Many countries have shifted away from issuing bonds in hard currencies toward issuing in local currencies. That takes away default risk,” says Strigo, noting that a few countries, such as Venezuela, have a significant proportion of US$-denominated debt and are regarded as distressed issuers.

Strigo is positive on high-yield bonds: “There are some risks going forward, such as low commodities prices and a slowing Chinese economy. But there are so many regional or country bets that we can have and hold different assets that we can construct a portfolio that can benefit from market conditions at any point in time.”

The Excel fund’s portfolio is invested in 30 to 40 countries and about 61% of its AUM is in investment-grade bonds, 34% is in high-yield and 5% is in cash. The average duration is five years vs 5.5 years for the benchmark.

The bulk (85%) of the portfolio is held in a mix of sovereign debt and state-supported companies, with 15% in corporate debt. About 55% of AUM is denominated in US$ and 45% is in local currencies, such as the Mexican peso.

The Excel fund holds about 110 securities from 59 issuers, and Strigo likes bonds such as those issued by Provincia de Buenos Aires, Argentina’s largest province. The US$-denominated bond maturing in 2021 is yielding 8%.

“The new [federal] government will negotiate with holdouts of Argentine bonds and we expect that Argentina will be current with its debts in early 2016,” says Strigo, adding that last November’s presidential election outcome was better than expected.

Another favourite position is a Republic of Hungary bond, which matures in 2025, is denominated in US$ and euros, and yielding 3.75% to maturity.

“We expect Hungary to be upgraded to an investment-grade rating in 2016,” says Strigo, “because of its solid macroeconomic situation.”

© 2016 Investment Executive. All rights reserved.