Canadian equities markets slumped last year as growing concerns about the impact of low commodities prices spread to other key sectors such as financial services. For 2016, portfolio managers of Canadian dividend and income equity funds are split between caution and opportunism now that valuations are at more attractive levels.

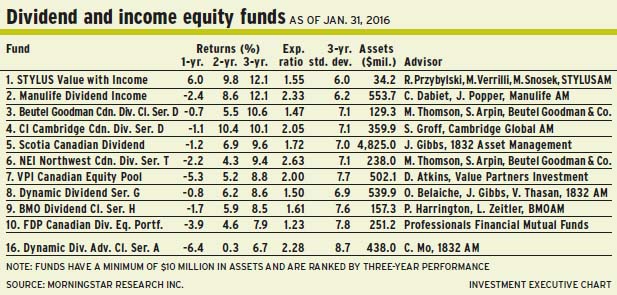

One portfolio manager in the cautious camp is Conrad Dabiet, senior managing director, Canadian value equity team, at Toronto-based Manulife Asset Management Ltd. (MAM) and portfolio co-manager of Manulife Dividend Income Fund. He shares portfolio-management duties with Jonathan Popper, senior managing director on the same investment team with MAM.

“The year began with quite a similar tone to last year. I haven’t seen any evidence to convince myself that anything has changed,” Dabiet says. “The big question is: ‘When will we see a wider effect from the decline in oil prices?’ Anecdotally, we hear that things have slowed down quite a bit out West. Looking at the fundamentals in the banking sector, we’ve yet to see considerable stress on the credit side. It is just a ‘wait and see’ situation, but you have to think that you will see the effects at some point.”

Taken together, energy, materials and financials comprise 75% of listings on the Toronto Stock Exchange; these stocks are cyclical.

“I don’t see any evidence that things have bottomed out or started a new ‘up’ cycle,” Dabiet says. “Luckily, we don’t invest in commodity companies because they can’t control the price of what they produce. That makes them difficult to value because we don’t know what kind of earnings they will generate into the future.”

Dabiet, a bottom-up investor who uses a blend of value and growth styles, focuses on companies that offer greater certainty about their earnings and cash flow, as well as have competitive advantages that provide the company with a relatively long so-called ‘runway’ for future earnings. Thus, although there is uncertainty about the strength of the broader market, Dabiet is confident about the stocks held in the Manulife fund: “We just look for certain businesses that we understand and can value.”

Although financials tend to be a mainstay in the income fund category, Dabiet has adopted a less favourable view of that sector. Moreover, sectoral weights are a byproduct of the stock- selection process, so financials account for 16% of the Manulife fund’s assets under management (AUM), followed by 15.6% in consumer staples, 14% in consumer discretionary, 9.3% in industrials and smaller weightings in sectors such as utilities.

From a geographical perspective, about 70% of the Manulife fund’s AUM is in Canadian stocks and 16% is in the U.S. The remaining 14% is in cash. The fund’s running yield is about 2.4%.

A favourite in the 60-name Manulife fund is Brookfield Property Partners LP, which was spun off from Brookfield Asset Management Inc.

“[Brookfield Property] looks for quality real estate that perhaps needs renovation or re-leasing to create more value in the portfolio,” Dabiet says.

Brookfield Property stock is trading at about $29.50 a share and pays a 4.5% dividend yield. Dabiet believes the stock has about 33% upside over three years.

Although economic conditions are challenging, prospects look better in the second half of 2016, argues Cecilia Mo, vice president with Toronto-based 1832 Asset Management LP and portfolio manager of Dynamic Dividend Advantage Series Fund.

“The first half [of 2016] won’t see a recovery in the oil market because Iran is coming back on the market; the oversupply situation will continue in the first half,” says Mo. “I expect that [oil prices] will get better in the second half, but that depends on how fast [the recovery occurs] and what price level will be sustainable, post-2016. That’s one of the tough questions.”

The other question mark hanging over 2016 is the precariousness of China’s stock market and economy. Yet, Mo argues, China’s stock market is a poor indicator because many investors are unsophisticated speculators and the authorities are having little success in dampening volatility.

“China’s growth is slowing down. But I do not see a hard landing – although, right now, the market is very concerned about that,” says Mo. “The retail numbers are strong, so the consumer story still is pretty good.”

Meanwhile, as worries about China have contributed to the bear market in Canada, Mo argues, some Canadian equities valuations have reached very attractive levels: “The banks look very interesting, and so do some of the consumer names. Valuations are more compelling compared with 12 months ago.”

Mo, a bottom-up value investor who focuses on firms that trade at low multiples yet have strong free cash flow, has allocated about 29% of the Dynamic fund’s AUM to industrials. “The market is worried,” she says, “because these names tend to be cyclical and it’s worried that we’re going into recession. But I don’t believe that’s imminent. These stocks are mispriced.”

About 17% of the Dynamic fund’s AUM is held in financials, 13% in consumer cyclical, 12% in health care, 10% in energy and smaller holdings in sectors such as technology. About 75% of AUM is in Canada and 20% in the U.S., with 3% in cash.

Mo, running a portfolio with 58 names, likes Bank of Nova Scotia. “Its valuation is almost back to March 2009 and a lot of bad news is priced into the stock,” she says, adding that the stock is trading at about 8.5 times earnings. “The exposure to the energy patch is manageable. Second, sentiment is poor because of [Scotiabank’s] exposure to Latin America. But markets such as Mexico and Chile are doing reasonably well.”

Scotiabank stock is trading at $54 a share and pays a 5% dividend yield. Based on earnings growth of 2%-3%, Mo expects a total return of 7%-8% over the next 12 to 18 months.

The pressures on the Canadian economy will continue to intensify this year, argues Stephen Groff, principal with Toronto-based Cambridge Global Asset Management (a unit of CI Financial Corp.) and portfolio manager of CI Cambridge Canadian Dividend Fund.

“The consumer will continue to deteriorate,” says Groff.” And the banks have a long way to go in terms of feeling the pressure on the economy, which is getting more difficult.”

There are downside risks in the economy, including high levels of consumer debt, excessive house prices in certain markets and rising unemployment in the oilpatch, he adds: “A lot of sectors have not fully felt the impact of lower commodities prices. But we don’t know how long that will take to show up. I don’t think we will see a V-shaped recovery in Canada.”

Going forward, the negatives outweigh the positives, says Groff: “The bulls will point to a weaker Canadian dollar stimulating meaningful amounts of exports. But I don’t see that being an offset to the global macroeconomic pressures on our economy. When it comes to the economy, you can say that I’m bearish. [I am] taking a very conservative approach.”

Groff does admit that valuations are more attractive now, but only in parts of the market. “[Sectors] that were expensive are getting better. But valuations are catching up with reality,” says Groff, noting that investors have flocked to stocks that are perceived to be safe, yet their valuations are stretched.

Groff, an investor who seeks high-quality companies at reasonable prices, is very selective. About 25% of the CI fund’s AUM is held in cash, with 20% in industrials, 20% in consumer cyclical, 12% in financials, 10% in consumer staples and smaller holdings in sectors such as real estate. About 50% of AUM is in Canada and 25% in the U.S. The running yield is about 2%.

One long-term holding in the 21-name portfolio is Brookfield Infrastructure Partners LP, a unit of Brookfield Asset Management Inc. “[Brookfield Infrastructure’s executives] are very intelligent capital allocators who are capable of taking advantage of distressed situations around the world,” says Groff, noting the firm has diverse interests in telecom, energy infrastructure and railways. “[The company has] compounded funds from operations north of 20% for several years.”

Brookfield stock is trading at $48 a share with a 5.9% dividend yield. There’s no stated target.

© 2016 Investment Executive. All rights reserved.