International equities markets have been struggling, weighed down by the uncertainty surrounding the U.K. referendum decision in favour of leaving the European Union, worries of an economic slowdown in China and generally high stock valuations. Thus, portfolio managers of international equity funds, including Jeff Feng, head of emerging markets equities for Invesco Hong Kong Ltd., argue that markets could take some time before they resume an upward climb.

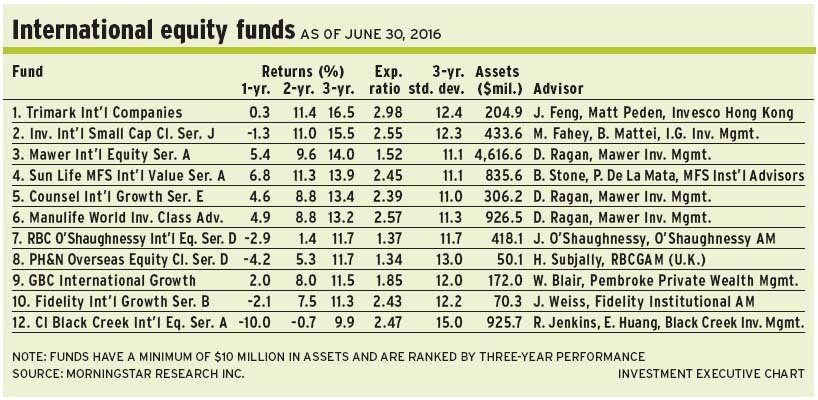

International equity funds invest in all markets except those in North America. Valuations in many markets are a key concern, especially in Japan, says Feng, lead portfolio manager of Trimark International Companies Fund. He shares portfolio-management duties with Matt Peden, vice president of Invesco.

“In 2015, valuations in Japan were no longer cheap compared with other markets,” notes Feng. “And the Japanese economy was struggling. Today, [Japan] has still not achieved what it wanted – healthy inflation. [Japan’s central bank] had to introduce, essentially, a negative interest rate policy. From an economic perspective, that is not a good sign.”

Meanwhile, investors in Europe are losing confidence in those markets as a result of the uncertain impact of the Brexit referendum and the ongoing crisis in absorbing refugees from the Middle East. As Feng notes: “All these things combine so that markets are treading water.”

Furthermore, Feng is concerned about the direction of interest rates: “How can interest rates go? We’re in negative territory in places like Japan. But the big issue is valuations. Other than emerging markets, I don’t think valuations are attractive. They range from fully valued or, to a certain degree, overvalued.”

Is there any hope that markets will turn positive eventually?

“If you look at history, eventually, things get better. But we don’t know if things will improve in the next 12 months or 36 months,” says Feng. “In our opinion, we will continue to muddle through.”

Feng is a bottom-up investor. About 52% of the Trimark fund’s assets under management (AUM) is in so-called Greater Europe, 39% is in Greater Asia, 5% is in Latin America and 4% is in cash. From a sectoral perspective, there’s about 31.4% in industrials, 22.4% in consumer defensive, 14.4% in information technology (IT), 8.8% in consumer discretionary and smaller holdings in sectors such as financials.

One prominent holding is South Korea-based Samsung Electronics Co. Ltd., which makes semiconductors, cellphones and digital displays. Referring to the first line of business, Feng says: “Growth in the future will mostly come from mobile servers and new applications such as in automobiles.”

Samsung is benefiting from consolidation in the chip industry, he notes. Samsung preferred stock is trading about KRW1.1 million ($1,126) a share. (KRW stands for Korean won.) Feng believes there is about 40% upside over two years.

The underlying problem is that markets need time to pause after several years of bull market performance, says David Ragan, director with Calgary-based Mawer Investment Management Ltd., and portfolio manager of Mawer International Equity Fund.

“Valuations got to a point that [markets] needed a break. The pace was unsustainable,” he says. “The performance was driven by a flood of free money and falling interest rates rather than fundamental economic improvement.”

Indeed, this situation is one of the big risks that markets will face in the next few years. “What are government long-term interest rates going to be like in one, two or five years? Long-term bond yields are very important to equities’ valuations. You’d have to go back to the tech bubble [in 2000-01] to get multiples [similar to] where they are now.”

For example, according to Bloomberg LP, the S&P 500 composite index is trading at about 19.5 times earnings, while the MSCI EAFE index is trading at about 22.3 times.

“Put this in context with near-zero interest rates and incredibly low discount rates for equities. If this low interest rate environment persists, then stocks are cheap. But if rates go back up to where they were 10 years ago, then equities will be overvalued,” says Ragan, noting that in 2006, long bond yields were generally around 4%-5%.

What are the odds of bond yields rising to 2006 levels? “They would go back up to where they were because of inflationary pressures or if economic growth takes hold,” says Ragan. “But it’s difficult to see that happening because there is a lot of excess capacity. Inflation is very low. And in some places, central banks are doing everything they can to fight deflation.”

The outcome of the Brexit referendum is weighing especially heavily on the U.K. pound sterling and that could be negative for many U.K. companies that move goods across borders. “However, it’s not catastrophic,” says Ragan. “There will be a long period of people asking, ‘How do we actually work this out? What sort of trade deals do we have to negotiate with Europe and, for that matter, the rest of the world?’ There is going to be a lot of uncertainty.”

Ragan is a bottom-up investor. About 63% of the Mawer fund’s AUM is in Europe, 26% is in Greater Asia, 2.6% is in Latin America, 1.3% is in Africa, and 2% is in cash. There’s also about 4% in North American-listed companies. On a sectoral basis, 22.6% is in consumer staples, 22.6% is in financials, 12.3% is in industrials, 11.5% is in health care and 8.2% is in materials with smaller weightings in sectors such as IT.

One top holding in the 53-name Mawer fund is London-based Aon PLC, one of the world’s largest insurance brokers.

“[Aon] has some structural growth drivers and should grow with [gross domestic product] in general. We really appreciate the quality of management and its ability to expand margins,” says Ragan. “Revenue may rise in the low-single digits, but earnings will grow at a higher rate.”

Aon, listed on the New York Stock Exchange (NYSE), is trading at about US$106.50 ($136.50) a share, (about 22 times earnings). The stock pays a 1.1% dividend.

Tightening of credit, already begun in the U.S., is a major factor in markets coming under pressure, argues Richard Jenkins, managing director and chairman of Toronto-based Black Creek Investment Management Inc., and lead portfolio manager of CI Black Creek International Equity Fund. He shares duties with Evelyn Huang, director, global equities, at Black Creek.

“I’ve been through three cycles in which you have a tightening of credit, and usually equities markets shake out,” he says. “Sectors and currencies move around. You don’t make a lot of headway, as far as returns are concerned. But earnings continue to improve because economies are improving.”

From a macroeconomic perspective, Jenkins maintains, North America is holding steady. “And Europe has turned upward. Not at a rapid pace, but most of Europe is now growing,” he says. “But other parts of the world that were reliant on high commodity prices have seen a major step backward – some are in recession.”

Demographic changes in China are leading to weakness in demand for commodities from emerging markets in Latin America and Africa, Jenkins adds: “The heavy lifting of building roads and railways in China is mostly behind them.”

Jenkins is a bottom-up investor, but argues that understanding the global environment is a must for picking the right companies: “Too many investors just assume, ‘The North American economy grows 2.5%, the world grows at 3.5%. It’s easy.’ Well, it’s not going to be easy. There are going to be significant differences [driving markets] and you need to understand that.”

Jenkins has allocated about 60% of the CI fund’s AUM to Greater Europe, 33% to Greater Asia, 4% to Latin America and 3% to cash. From a sectoral perspective, consumer services account for 20.9% of AUM; industrial goods, 18.9%; health care, 13.6%; and financial services, 12.6%; plus smaller weightings in sectors such as energy and IT.

One top holding in the 27-name fund is ICICI Bank Ltd., one of India’s leading commercial banks. Although legislation is forcing the bank to clean up the bad loans on its balance sheet, “[its] commercial loans and revenue are growing in the mid-teens,” says Jenkins. ICICI bank’s American depositary receipts, listed on the NYSE, trade at about US$7.15 ($9.30) a share.

© 2016 Investment Executive. All rights reserved.