An allocation to real estate offers a host of benefits for investors of all types: a stable income stream and strong returns, inflation protection, capital preservation and diversification through non-correlation to the broader markets.

But retail clients may not have the financial capacity to invest in commercial real estate directly. For these investors, real estate investment trusts (REITs) are an effective alternative – with some added advantages. Unlike direct investing, which has high barriers to entry, REITs are easily accessible by investors of all types. REITs also have a highly liquid and transparent structure. Plus, they offer a diversification advantage by providing access to a wider range of real estate exposures than direct investing.

But not all REITs are created equal. Passively managed vehicles tend to lose some of the advantages that lead investors to real estate in the first place. For example, these REITs have a tendency to move in lock-step with the broader equity market, and this high correlation diminishes their diversification benefits.

Active management is the solution

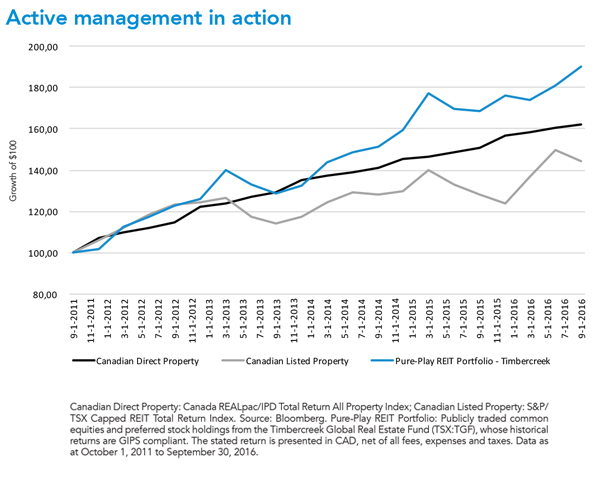

Through careful screening and selection, active management is able to create a portfolio of pure-play REITs that retain all the advantages of listed vehicles while at the same time capturing the benefits of direct real estate investments. The graph below compares the performance of Canadian direct real estate, the S&P/TSX Capped REIT Total Return Index and Timbercreek’s actively managed portfolio of publicly listed real estate.

Returns for the pure-play portfolio of publicly listed real estate exceed both direct real estate investment and the passive, indirect investment option. While volatility for direct real estate will always be lower than publicly listed investments (3.5%), the actively managed pure-play portfolio bests the passive option (9.2% versus 10.2%, respectively).1

Importantly, the active solution of publicly listed investments is more tightly correlated to direct investing than the passive option (96.9% versus 87.6%, respectively).2 This is clear evidence that active solutions are a more effective proxy for direct investing than passive REIT investment vehicles.

The power of process

A strong process is the key to achieving the advantages of active management described above. It should include two key phases:

1. Filtering out companies that undercut the benefits of real estate investing

2. Comprehensive company and market analysis of remaining candidates to identify stocks for inclusion in the portfolio

Filtering out detractors

Out of the approximately 500 companies that make up the universe of listed global real estate securities, about one-third tend to detract meaningfully from performance and should be screened out. “You can think of this initial screening step as a removal of impurities,” says Corrado Russo, Senior Managing Director, Investments & Global Head of Securities, Timbercreek Asset Management, a global asset manager specializing in real estate.

Common detractors include:

- real estate developers;

- brokers;

- construction companies;

- poorly located assets

- highly levered assets and

- emerging markets-based names, particularly developers and home builders.

“Developers typically don’t pay dividends. They usually redirect capital gains into the next project,” explains Russo. Builders and brokers often pay very low dividends. Emerging markets names also pay weak dividends and tend to have unstable businesses. “By stripping those away you see your income rise tremendously,” adds Russo. Poor-quality real estate, financially engineered cash-flow streams and highly levered assets are other hallmarks of the group of names that a strong active manager screens out immediately. “Those are the things that give you more volatility and diminish the positives of exposure to real estate,” explains Russo. He adds: “Removing them helps you get closer to the experience of direct real estate investing, but through a liquid vehicle.”

Active selection

At this point in the process, “it’s all about the underlying assets,” notes Russo. A wide range of variables are parsed and analysed, and while quantitative tools help crunch the numbers, final calls on which names make it into the fund should be shaped by the portfolio manager’s real estate experience and expertise.

One group of variables measures internal growth prospects. They include occupancy rates, lease rollover relative to comparable local-market units, operating margins, and contractual rent increases. The goal of the analysis is to develop forecasts for a number of key metrics, including net operating income, cash flows and dividend sustainability, as we would with direct real estate investments.

It’s also critical to examine companies’ track records and prospects for external growth. This involves assessing acquisition and sale activity. Is management making smart choices when they buy and sell properties? Have they shown good judgement in the way they’ve financed acquisitions? Another important variable is capital improvements. “Renovating an apartment building’s lobby or adding high-end amenities can generate higher rents over the long term,” Russo explains.

Strong, sustainable income is the goal, but only at an acceptable level of risk. An elaborate risk management regime will examine a host of variables, including:

- Real estate risk – Considers asset quality and location (in part through property tours), as well as lease structure

- Corporate risk – Assesses management quality (partly through in-person meetings) and company business model

- Balance sheet risk – Examines key metrics such as leverage, interest rate sensitivity and fixed charge ratio

- Stock price risk – Analyzes liquidity (30-day average volume) and volatility (one-year standard deviation)

The result: A high-active-share portfolio of quality global names that offers a liquid proxy for direct real estate investing. Such a portfolio will have exceptional prospects for income generation and growth because its constituents are purchased at a discount to intrinsic value.

A real alternative

With the right process and management expertise, an actively managed global REIT portfolio can deliver the key benefits of direct real estate investing. “Even though they’re liquid portfolios of stocks, they behave much more like a bricks-and-mortar real estate portfolio,” concludes Russo.

Timbercreek Asset Management is a global expert in private and publicly traded real estate investments, focused on delivering predictable, sustainable and growing returns to investors.

For more information on Timbercreek’s investment solutions, including the Timbercreek Global Real Estate Income Fund, visit Timbercreek.com/advisors

1 Source: Bloomberg. Data as at October 1, 2011 to September 30, 2016.

2 Source: Bloomberg. Data as at October 1, 2011 to September 30, 2016.

Partner Reports is a space made available for businesses who wish to publish content for financial professionals. Investment Executive journalists are not involved in writing these articles.