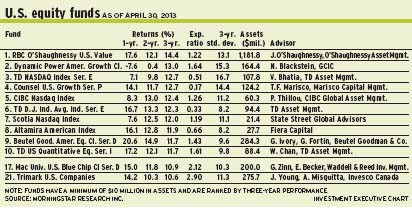

AS THE U.S. ECONOMY GAINS momentum, thanks to improving housing and manufacturing, markets are pricing in better times ahead. Fund portfolio managers are upbeat about investment opportunities, although selective in their choices.

“The key drivers for the U.S. recovery are focused around housing,” says Noah Blackstein, vice president with Toronto-based GCIC Ltd. and portfolio manager of Dynamic Power American Growth Fund. “The 2008 crisis was born and bred in housing; housing is leading us out of the crisis. It will have its fits and starts, but it is certainly on track.”

There now are 900,000 annual housing starts, Blackstein adds, compared with 550,000 in 2009 and 2.1 million in 2005. “And we are not even close,” he says, “to satiating the demand.”

Excess inventory, Blackstein says, has disappeared and builders are finding it hard to secure skilled labour and land lots. It’s difficult to get building permits in some municipalities because they laid off some of their staff during the 2007-08 slowdown. “You will have a significant supply/demand imbalance for years to come,” Blackstein says, “That’s a positive for the U.S. economy.”

Meanwhile, manufacturing has been bouncing back, led by the domestic boom in oil production. The U.S. has turned into a net exporter of refined petroleum products, Blackstein says, for the first time since the Truman administration.

“Technology, through horizontal drilling and hydraulic fracking, has unleashed a revolution in production,” Blackstein says. “Without it, you would never see an economy the size of the U.S. have the ability to achieve close to energy independence over the next decade.”

From a valuation standpoint, Blackstein notes, the equities market is up. But he is troubled that it is led by defensive stocks, such as consumer staples and utilities.

“They have rallied to near historical-high valuations,” Blackstein says. “For me, the danger rests not in secular or cyclical growth; it rests in this price momentum that some investors ascribe to consumer staples and utility stocks, which is dangerous and correlated to bond yields.”

Should yields rise, which is likely, he adds, “these stocks will be hurt badly.”

A bottom-up growth manager, Blackstein is running a concentrated portfolio of 25 names that fit within three sectors: 62% of the Dynamic fund’s assets under management (AUM) is in information technology; 22% is in consumer discretionary; and 14% is in health care. Blackstein seeks companies with revenue or earnings growth in the high teens or better, strong returns on equity and sustainable growth for three to five years into the future.

One top holding is Amazon.com Inc., the online retailer that has built a dominant position on the Internet, although its earnings are under pressure because of massive investment in distribution centres.

“That big capital expenditure program is coming to an end,” Blackstein says. “It has strong revenue growth. But it also has the ability to show operating leverage over the next few years. The underlying earnings power of the company is significantly below where the stock is trading.”

Amazon.com stock is trading at roughly US$268.30 ($272.50) a share. There is no stated target.

Gus Zinn, senior vice president with Kansas City-based Waddell & Reed Investment Management Co. and co-manager of Mackenzie Universal U.S. Blue Chip Class Fund, is equally bullish: “The recovery is slow, but it is sustainable. One of the main drivers is that the Federal Reserve Board will keep the pedal down until we get a sustainable recovery. So, we have this backstop of low interest rates, which is supporting the stock market. In turn, that helps the consumer-wealth effect and the housing market, which has a multiplier effect on the economy.”

Second, there has been an improving job market. “It’s in fits and starts but an improving trend,” says Zinn, who shares portfolio-management duties with another Waddell & Reed senior vice president, Erik Becker.

Third, Zinn points to the energy boom: “It’s a secular positive, whether it’s decreasing our dependence on foreign oil or the abundance of natural gas, which will help bring manufacturing growth back to the U.S.”

After years of shrinking, Zinn adds, the manufacturing sector is rebounding.

But there are challenges, such as reaching an agreement in Congress on a government budget that could mean higher taxes or spending cuts.

There also are concerns about Europe, which has not stabilized entirely. “At some point,” Zinn says, “it will get better, although the data points will remain low for a few quarters. On the other hand, this also keeps commodities prices low, and keeps the Federal Reserve in a very accommodative stance in the U.S.”

Zinn says stocks will continue to attract more attention from investors frustrated with the alternatives. “It could go on for a long time,” he says, adding that stocks are reasonably priced at about 13 times earnings. “We’ve had very strong earnings growth to go along with a rising market. Most of the market appreciation has been driven by earnings, not by multiple expansion.”

A growth-oriented portfolio manager, Zinn looks for stocks that have two to three years of earnings power that is higher than market expectations and improving competitive positions in their industries.

Using a blend of top-down and bottom-up styles, Zinn and Becker run a portfolio of about 40 to 50 holdings in the Mackenzie fund that fit three broad themes: manufacturing recovery, mobile communications and growing online consumer spending. Currently, about 17.8% of the Mackenzie fund’s AUM is in consumer cyclical stocks; 17.1% is in industrials; 15.3% is in financials; and there are smaller weightings in sectors such as energy.

One favourite holding is Harley-Davidson Motor Co., the fabled motorcycle manufacturer that is rebounding after hitting a hard patch in 2008-09, and which has rationalized production. Says Zinn: “The new CEO, Keith Wandell, brought in a lot of new people and went after the cost structure. Wandell has restructured the company.”

Harley-Davidson stock is trading at about US$52.85 ($53.90) a share, or about 18 times earnings. Zinn has a target of about US$75 ($76.50) within two years.

Another favourite is railway firm Kansas City Southern (KCS). “It’s a great play on the renaissance of North American manufacturing,” Zinn says. “Lots of companies, including some automakers, see Mexico as a very good place to locate their new plants. Kansas City Southern is unique because it has the best network down into Mexico.”

Although KCS stock is trading at about US$107 ($109), for a price/earnings ratio of 28, Zinn’s target is US$150 ($153) within three years.

Ashley Misquitta, a portfolio manager with Toronto-based Invesco Canada Ltd., who co-manages Trimark U.S. Companies Fund, believes the U.S. is in better shape than most people realize.

“When we look back 10 years from now,” says Misquitta, who shares portfolio-management duties with Invesco vice president Jim Young, “one of the things we will remark on is that the structural dynamics of the U.S. economy were stronger than people perceived them to be.

“No question,” Misquitta continues, “there are concerning elements: debt and deficits and the need for entitlement reform, which will cause some market volatility. However, there were some important tailwinds we tend to overlook.”

One of those tailwinds is that the U.S. is an important engine for innovation. Misquitta points out that many of the most important innovations in medicine, technology and energy in the past 20 years came from the U.S.

“That’s an important dynamic,” he says. “There’s also a strong culture of entrepreneurship that helps support the economy.”

Another positive factor is that the U.S. is in better demographic shape than other developed countries because of its higher birth rate and its policy of accepting immigrants, who will buy homes and cars and raise children.

Still, Misquitta says, economic decisions have to be made in the U.S. regarding benefits such as social security. But the current demographic trend, he says, “will make things a little less painful than they might otherwise be.”

Within Congress, Misquitta adds, there is greater awareness of the need to tackle these challenges than was the case a few years ago.

As for external challenges, Misquitta points to Europe’s recession: “It’s certainly a headwind for some U.S. businesses.” Similarly, China’s slowdown presents near-term headwinds. “It’s hard to be certain because, in a few months, we may see China’s economy pick up again.”

A bottom-up investor, Misquitta focuses on 40 to 45 names that have competitive advantages over their peers and benefit from high barriers to entry. From a sectoral standpoint, about 24% of the Invesco fund’s AUM is in infotech firms; 14.5% is in health care; 14.4% is in industrials; with smaller holdings in sectors such as financials and materials.

One top long-term holding is KLA-Tencor Corp., which makes capital equipment for semiconductor makers such as Samsung Corp. “As we get smaller and smaller processing nodes,” Misquitta says, “it gets more difficult to manufacture. These guys have become more important to the chip makers.”

As a result of strong margins, KLA-Tencor has had an annual average earnings growth of 11% for the past five years.

KLA-Tencor stock is trading at about roughly US$55.30 ($56.40) a share (13.4 times earnings) and pays a 3% dividend. There is no stated target.

Another favourite is United Parcel Service Inc. (UPS), a leading global package-delivery firm. “It’s very cash-generative,” Misquitta says, adding that the firm is benefiting from growing global trade and e-commerce.

UPS stock is trading at roughly US$83.65 ($84.90) a share and pays a 3% dividend.

© 2013 Investment Executive. All rights reserved.