The financial advisors surveyed for this year’s Report Card on Banks are deeply dissatisfied with their firm’s back office. Outdated technology, inefficient processes and high turnover among back-office staff are cause for much concern.

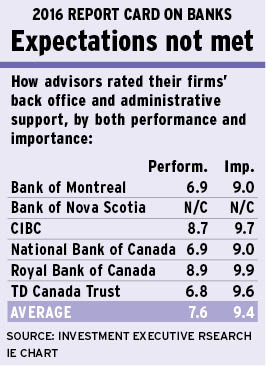

This dissatisfaction is evident when comparing the overall average performance rating (7.6) and the overall average importance rating (9.4) that advisors gave the “back office and administrative support” category. The difference between the two ratings – 1.8 points – is the second-largest “satisfaction gap” in the survey, which means that advisors’ expectations are far from being met.

This satisfaction gap is nothing new. Advisors in previous Report Cards complained loudly about their back office’s services.

Advisors’ dissatisfaction with their back office was most evident this year at Toronto-based TD Canada Trust, which received a survey-low performance rating of 6.8 in the category, down from 7.5 last year. According to TD advisors, high turnover and lack of accountability among back-office staff leads to errors and delays.

“Accountability is poor,” says a TD advisor in Ontario. “Sometimes, they don’t understand how quickly I need things done.”

Advisors with Montreal-based National Bank of Canada also gave their bank a low performance rating of 6.9. In addition to inefficiency among back-office staff, advisors are frustrated with the outdated back-office technology.

“[The back office] needs to keep up with technology and client-based support,” says a National Bank advisor in Ontario. “It’s a little bit behind on technological advancements. That leaves advisors in a lurch with clients.”

Advisors with Toronto-based Bank of Montreal (BMO), who also gave their bank a performance rating of 6.9 for the back office, expressed similar frustrations with outdated technology.

“It comes back to technology,” says a BMO advisor in Ontario. “The way they communicate is by fax.”

Given the long-standing concerns about the back office, firms are adopting strategies to ensure that the department is more accessible to advisors.

For example, Toronto-based Bank of Nova Scotia eliminated advisors’ access to the bank’s back office this year, implementing a call centre instead. As a result, Scotiabank has a “not calculable” rating for the back office because the bank’s advisors believed they could not rate something to which they no longer have direct access.

“[The bank] has phased out [the back office],” says a Scotiabank advisor in Ontario. “We have a call centre for that now.”

“[Advisors] are referring to the changes we made to our shared services organization,” explains Fulvia Cantarutti, Scotiabank’s district vice president for GTA North. “We found we had the same jobs in multiple locations right across the country, [so] we made the decision to centralize operation to reduce the duplication.”

However, some advisors were not at all happy with these changes. Says a Scotiabank advisor in Ontario: “We don’t have a back office anymore, and I hate it. I am very frustrated.”

Still, the bank is going through a transition period and advisors should give the new setup a chance, Cantarutti says: “The tools and technology we are equipping each of the advisors with in the long run will make their jobs a lot more pleasurable. I think it’s a bit of an adjustment period, but, in the end, we will all be better for it. And customers will appreciate the efficiency we are able to deliver to the experience.”

In contrast, other banks have taken a different approach, beefing up either the technology or the staffing in the back office, much to their advisors’ satisfaction. Case in point: advisors with Toronto-based Royal Bank of Canada (RBC) gave the bank the highest performance rating in the back-office category, at 8.9, up from 8.4 in 2015, because of the way RBC has leveraged its approach to make the back office more efficient.

“It’s all automated,” says an RBC advisor in Ontario. “Everything is there. You send in a request, and they follow up quickly.”

In fact, Michael Walker, vice president and head of branch investments with RBC, explains that several steps have been taken to ensure the bank’s back office is as efficient as possible.

“We’ve been trying to look for opportunities to streamline things and make [the interaction] smoother for the advisor,” he says. “When we’re trying to transfer a portfolio, we found an opportunity to take down the average time. We had four ways to submit a transfer, and what we evolved to was one very efficient way to do it.”

Another way that RBC has increased its back office’s efficiency is by adopting electronic signatures, Walker adds: “What we used to find was when our [advisors] would complete a transaction manually, there was a tremendous amount of rework or errors that would occur. By using e-signatures, that rework has gone to zero. You can’t do e-signatures without them being done straight through and correctly. [This strategy] has liberated a tremendous amount of time on the back office and, frankly, it’s a great client experience.”

Similarly, advisors with Toronto-based Canadian Imperial Bank of Commerce (CIBC ) also were pleased with the way their bank improved its back office’s efficiency, rating it at 8.7.

“The [back office] gets things done in a timely manner,” says a CIBC advisor in Ontario. “They don’t leave you hanging out to dry.”

A big reason for CIBC advisors’ satisfaction is the COMPASS platform, a new front- and back-end order-entry system that the bank introduced over the past couple of years, according to Scott Wambolt, CIBC’s senior vice president, national sales and service.

“COMPASS allows our advisors to spend more time meeting a client’s needs and less on administrative data-entry tasks,” he says. “We’ve really streamlined the process.”

© 2016 Investment Executive. All rights reserved.